by Dr. Daniel Thornton, D.L. Thornton Economics

The Fed engaged in a massive bond-buying spree following the Lehman Brothers bankruptcy announcement on September 15, 2008. The bond-buying program, commonly referred to as quantitative easing (QE), ended October 2014. However, the Fed pledged to maintain its balance sheet at the $4.5 trillion level indefinitely.

QE was intended to reduce yields on long-dated Treasuries, mortgage-backed securities, and agency debt. The effect on these yields would spread to other long-term yields through arbitrage, or what chairman Bernanke called the portfolio balance effect.

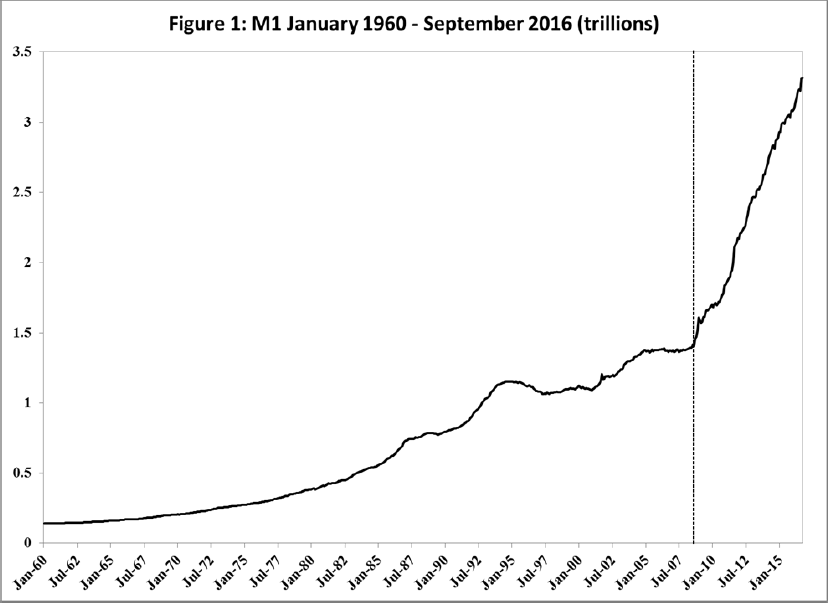

There is considerable debate whether or to what extent QE reduced long-term yields. But there is another effect of QE that is unassailable, although it has received almost no attention. Specifically, QE produced a massive increase in the M1 money measure. M1 increased by $1.9 trillion from August 2008 to October 2016—more than it increased during its previous 48-year history. This is shown in Figure 1 (the vertical line denotes September 2008).

On October 3, 2008, Congress passed The Emergency Economic Stabilization Act of 2008 which permitted the Fed to pay interest on excess reserves (IOER). It was thought that IOER would enable the FOMC to control the federal funds rate, while at the same incentivize banks to hold the reserves created by QE as excess reserves in order to avoid a massive expansion of the money supply.

This didn’t happen. Here’s why:

FIRST

Banks had so many reserves that they no longer financed lending by issuing large negotiable certificates of deposits (CDs) and by borrowing continuously in the overnight federal funds market. Prior to QE, only a small fraction of loans were financed by reserves. Now, reserves finance nearly all bank lending.

SECOND

Banks have an incentive to make any loan with a risk-adjusted interest rate higher than IOER. This is not a difficult task. Many loans are at least partially collateralized and are made at rates significantly higher than the IOER. Hence, banks are making all high-quality loans as well as some risker loans than they would were they not holding massive amounts of excess reserves.

The Wall Street Journal (WSJ, July 23-24, 2016) reported that some banks were lowering the credit score requirements and making even riskier loans. Other banks were bolstering their reserves in anticipation of higher loan losses on the loans they had already made.

THIRD

The Fed has a fractional reserve system. This means every dollar of reserves can finance multiple dollars of loans and the corresponding amount of checkable deposits — the core component of M1. Total checkable deposits increased by $1.3 trillion since August 2008, more than twice the increase during the past 48 years.

The Fed’s highest reserve requirement, 10 percent, means every dollar of reserves could support $10 of checkable deposits. But the Fed’s system of reserve requirements is complex so the ratio is not 10. The ratio of checkable deposits to required reserves has been higher than 10 since 1991. It has trended down somewhat since August 2008 because all loans have been financed with reserves, but averaged 11.5 during the past year.

All of this means...

... that as long as banks continue to make loans, the money supply will continue to expand. The potential expansion is finite, but incredibly large! Banks still hold nearly $2 trillion in excess reserves. This means that banks would have to make additional loans of $23 trillion in order to convert all of their excess reserves into required reserves, an impossible task — the national debt is $19.3 trillion.

Many economists believe that banks are holding excess reserves because of the IOER. This is ridiculous. The FOMC increased the IOER to 75 basis points last week. But that won’t halt the rapid growth of M1. The IOER would have to be much higher than 75 basis points. Moreover, as George Selgin has pointed out (WSJ, Sept. 27, 2016) there appears to be a legal barrier to having the IOER high enough to achieve this objective.

The Fed could prevent further growth of M1 by imposing 100% reserve requirements; banks would only be able to increase loans and the money supply by $2 trillion. But increasing reserve requirements above 12% requires amending the Federal Reserve Act. This would take time and it is unlikely Congress would do it.

Alternatively, the FOMC could shrink its balance sheet. It has done this to a limited extent by continuously rolling over about $400 billion in reverse repurchase agreements. But to be completely effective, the balance sheet needs to be reduced to a level where banks finance nearly all of their lending as before.

As long as banks have more excess reserves than they would like to hold and they can make loans with a risk adjusted rate of return higher than the IOER, they will continue to finance lending with excess reserves, and the money supply will continue to increase.

Some may argue that the size of M1 is not a problem because inflation is below the FOMC’s 2% target. Others might suggest that M1 is not a problem because spending is more closely tied to broader monetary aggregates, like M2. While the growth of M2 is not as dramatic, it has increased 70% over the past 8 years.

In any event, the recent growth in M1 is unprecedented, so we have no idea what might happen. I don’t believe its effect will continue to be reflected only in equity and real estate prices. It seems likely that it will eventually inflate a broad range of consumer prices as well. Should this happen, the FOMC will find it nearly impossible to shrink its balance sheet fast enough to avoid further large increases in M1.

Moreover, the FOMC will find it extremely difficult to reduce M1; draining excess reserves is one thing, draining required reserves is another. Indeed, all new lending would cease because banks would have to issue large amounts of CDs just to finance their existing loans; the multiplier works in reverse, too.

Consequently, the FOMC may be unable to avoid an inflation disaster.

EDITOR'S NOTE

This is a Hedgeye Guest Contributor research note written by Dr. Daniel Thornton. During his 33-year career at the St. Louis Fed, Thornton served as vice president and economic advisor. He currently runs D.L. Thornton Economics, an economic research consultancy. This piece does not necessarily reflect the opinion of Hedgeye.