“I entered the work force cleaning breast pumps at the pharmacy! It was a part-time gig while I was at school… no interview required.”

-Chris Hemsworth

Humor aside, and as the Demographer on the Hedgeye research bench, it’s my job to make sense of the larger trends we’re seeing across the country. Taking the Early Look pen for Keith this morning, I see an important rhythm-of-history subtext playing out related to the “gig” economy.

Yes, the gig economy is alive and well – but could America be reaching peak gig? I think it's likely. The generation most attracted to gig work (Gen X) is now reaching maturity. The generation now rising in the workplace (Millennials) accepts informal and impermanent work arrangements less by preference than out of necessity: If offered the choice, what most Millennials prefer in their workplace is community, security, institutional attachment, and long time horizons – i.e., something very ungiglike.

Meanwhile, with both parties vying to offer workers greater protection against job loss, pay cuts, and uncompensated overtime, the political wind is definitely blowing in the Millennial direction. It is only a matter of time, and perhaps not much time, before policy makers accompany this "formalization" of employment with measures to prevent employers from making end runs around the rules via "gig" workers. Uber's insistence that its drivers are contractors and McDonalds' claim that its franchisees are independent employers are just the opening salvos of this emerging generational weather front.

Back to the Global Macro Grind…

The Gig Economy is alive and growing. What’s happening? The Commerce Department recently proposed a four-part definition for what it calls “digital matching firms.” (Think of your Ubers, your Airbnbs, and your TaskRabbits.) According to the definition, these firms use technology to facilitate P2P transactions, rely on user reviews for quality control, offer worker hour flexibility, and rely on workers to use their own assets to perform their job duties.

Why is this important? Because it’s the first significant step anyone’s taken in some time to try to define—and ultimately measure—the so-called “gig economy.”

It seems silly, really. Everyone from Hillary Clinton to Barack Obama has been urging regulators to protect gig economy workers—yet nobody seems quite sure of who works in the gig economy, whether or not it comprises a growing share of the workforce, or even what it is. The last official study of this sector took place over a decade ago by way of the BLS 2005 Contingent Work Supplement (CWS).

One thing is for sure: Though the number of digital matching firms is expanding rapidly, these companies represent only the tiniest sliver of a growing gig economy.

How big is the whole gig economy, exactly? Again, your bureaucracy is working on it—and it’s left to analysts like me to draw their own inclusions.

What is the Gig Economy? Experts often define the “gig economy” by equating it with so-called contingent employment. At its narrowest, the BLS classifies contingent work as a strictly impermanent position, typically expected to last no longer than one year. Using this definition, the BLS reported that in 2005, between 1.8% and 4.1% of the workforce was contingent—a share that had declined slightly since 1995.

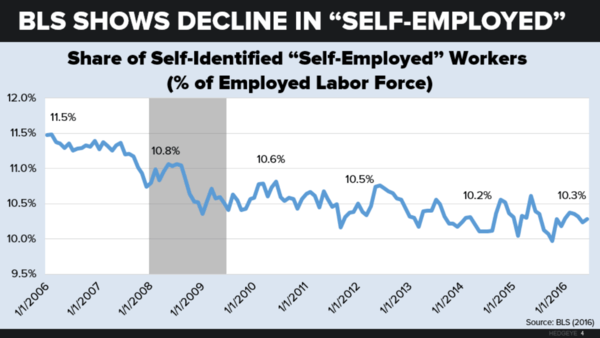

The BLS also releases monthly data on another, slightly broader component of the gig economy: self-identified “self-employed” workers. Here too we see a decade-long period of gradual decline: Since 2006, the self-employed share of the population has slid from 11.5% to 10.3%.

But here’s the thing: These BLS figures leave out a vast share of the true gig economy. Think about it. An agency temp, an on-call staffer, and even a standard part-time employee can and perhaps must be considered “contingent.” But these workers are left out by either of the above measures because they are not strictly “impermanent” or “self-employed.”

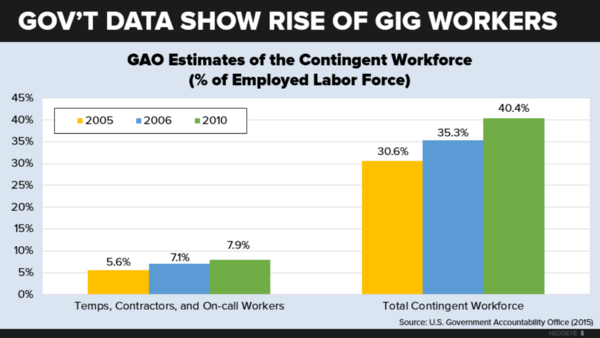

This is where an important 2015 GAO report on the gig economy comes in. The GAO broadens the notion of contingent workers to include “all individuals who maintain work arrangements without traditional employers or regular, full-time schedules.”

Using this more comprehensive measure, we see that the gig economy is much larger than the previous BLS estimates. By looking at historical CWS data, the GAO found that a whopping 30.6% of laborers were contingent in 2005.

Not only that, but the gig economy is also growing steadily. By analyzing more recent General Social Survey data, the GAO determined that the contingent share of the workforce grew to 40.4% by 2010. (Some of this growth may be due to differences in the sample populations surveyed.)

Within this GAO-defined gig economy, there are several categories of work that we know are growing rapidly.

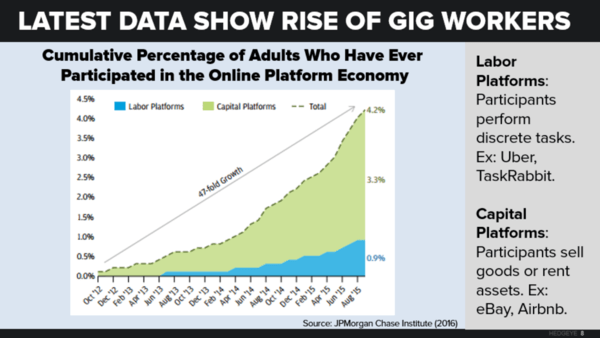

One is part-time workers, who have grown as a share of the workforce by about 2 percentage points since the Great Recession. Another is independent digital contractors, who—while still few in number—are surging. JPMorgan Chase finds that, as of August 2015, 1 percent of adults make money in the “online platform economy” each month (as Uber drivers, Airbnb renters, etc.)—a tenfold increase from October 2012. During the same time period, the share of Americans who report ever having worked in the online platform economy exploded 47-fold to 4.2%.

All told, economist Gerald Friedman estimates that as much as 85% of the jobs added since 2005 have been temp, on-call, or contracting positions. Sara Horowitz, executive director of the Freelancers Union, asserts that, "The sector of workers who don't have traditional full-time jobs—whether by choice or not—is a sizable and growing portion of the workforce."

If anything, even the broad GAO definition may underestimate the gig economy. Virtually no full-time workers would self-identify as contingent workers, but at least some alternatively employed individuals—such as contractors—consider themselves regular full-time workers.

Why The Gig Economy is Growing: Drivers

“Artisanal” makes a comeback. Before 2000, CPG companies and big-box retail chains were marginalizing mom-and-pop stores virtually to extinction. However, in the last decade-plus, we’ve seen the pendulum start to swing back toward freelancers. In agriculture and retail, much of the growth has been at the bottom of the market, from the small-scale organic farmers surging in popularity to the do-it-yourself Etsy crowd selling handmade products with great success.

Service sector grows, production stagnates. The growth of the gig economy is also rooted in the broader expansion of the service sector. (It’s hard to think of a contingent worker who isn’t providing services, whether it’s an Uber driver, a TaskRabbit “Tasker,” or a part-time musician.) Since 2006, service-sector employment has climbed by 10%, with the sector adding roughly 12 million new jobs. By contrast, goods-producing industry employment has not even come close to its pre-recession levels, falling by nearly 13% since 2006 (amounting to 3 million lost jobs).

The service sector’s growth is also evident when we dig deeper into the newest GDP numbers. Buried in the overall negative report is this tidbit: The personal consumption of services, which grew by 1.3% during Q2 2016, contributed more than 100% of all Q2 GDP growth (which registered just 1.2%).

Generational change. Since the 1980s, generational forces have been tilting the economy toward more gig-like work arrangements. Boomer young adults were the first to separate from the conventional 9-to-5 jobs of their parents, preferring to “get by” rather than sell out.

Sure, many of these Boomers are now retiring. But they’re being replaced in the workforce by a generation that is even more gung-ho about gig work: Xers. This generation practically invented the phrase "free agency" and “be your own boss”—and now, the rise of the sharing economy has given them the chance to work as little or as much as they want depending on their personal obligations and financial needs.

Millennials have similarly flocked to piecemeal, part-time gigs—though many had no choice in the matter. Despite their reputation as job-hoppers and tech entrepreneurs, a much larger share of Millennials would prefer the security of a conventional full-time position. This generation joins their elders in this contingent labor force, but more as underemployed “perma-temps” stuck there unwillingly rather than as contingent workers by choice.

Broader Implication. Go long on businesses and services that create and manage a gig economy framework. Platforms that help gig economy companies manage their operations are a solid bet. For example, an IT-managed service provider could be the perfect solution for a business trying to migrate to a contractor-based workforce but unsure of the HR implications.

Privately held San Francisco-based startup Payable, which created a software-as-a-service product to make it easier for contractors to get paid, has seen heavy business-side demand from companies looking to manage their own independent contractor fleets. Services like QuickBooks Self-Employed, offered by Intuit (INTU), are valuable tools for freelancers trying to navigate the complex world of reporting earnings from a multitude of sources.

Brace for the continuing legal battle between the government and gig economy firms. Both political parties are increasingly concerned with kick-starting the economic fortunes of the lower and lower-middle class, whether by raising the minimum wage or ensuring overtime rights. The important stage two of this fight (which is already coming into view) is protecting all of the people who fall through the cracks because they have nontraditional jobs. The various lawsuits brought against gig economy giants like Uber are the government’s way of trying to bring contingent workers into the net of formal employment.

Millennial gig economy workers would be thrilled to get the same benefits and rights as traditional full-time employees. But the real battle of this socialized work movement will be between government regulators and Xer freelancers who don’t want assistance—i.e. rules that hamper their freedom and their earning opportunities.

To learn more about my sector and receive my demography work please contact .

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.46-1.60%

SPX 2156-2193

VIX 11.01-14.76

EUR/USD 1.09-1.12

Gold 1

Best of luck out there today,

Neil Howe

Managing Director