Here's an unabridged review Richards sent me last night after going through the numbers in Nike's 10k that we think matters as it relates to the central themes (mainly share shift in distribution and pressure on legacy retailers) in the Nike ecosystem.

The punchline is that I'd give anything to NOT be an executive running FL, FINL, HIBB, or any other retailer that disproportionately relies on Nike as we head into calendar year-end.

1) DTC at NKE added an incremental $1.2bn in Fiscal 2016, that was paced by 51% e-commerce growth. The composition of that growth adds important context, we think, to the relationship with the company’s traditional wholesale partners primarily in the US. One of the key points of pushback we received when we laid out our $11bn in e-comm by 2020 thesis for Nike was that the lion’s share of direct growth was going to come in Global markets. That’s not been the case to date, and this dynamic will continue to pressure the likes of FL and FINL. For the year – NA accounted for ~50% of NKE’s DTC growth. Tack on China and that comprises ¾ of the growth for the year.

2) If we breakdown that Nike NA growth into channel specific segments over a longer time series it becomes strikingly evident where the next leg of growth is coming from. All in we saw an incremental $1bn in sales for the year taking Nike on this continent to $15bn with DTC accounting for 58% of the incremental dollars. Yea, the fact that NKE DTC accelerated to 17% growth in the year is notable, but what we think is far more important to the dynamic between NKE and its traditional wholesale accounts is that the incremental wholesale dollars recognized on the P&L was about half as much as the worst year we’ve seen over the past 5 at just $431. $431 (north of $700mm at end retail) translates to 4%, again half the trough year we’d seen from 2012-2015. That’s a much smaller pie for the content distributors to fight over, and we expect it goes to something starting with a 2 in the next Fiscal year.

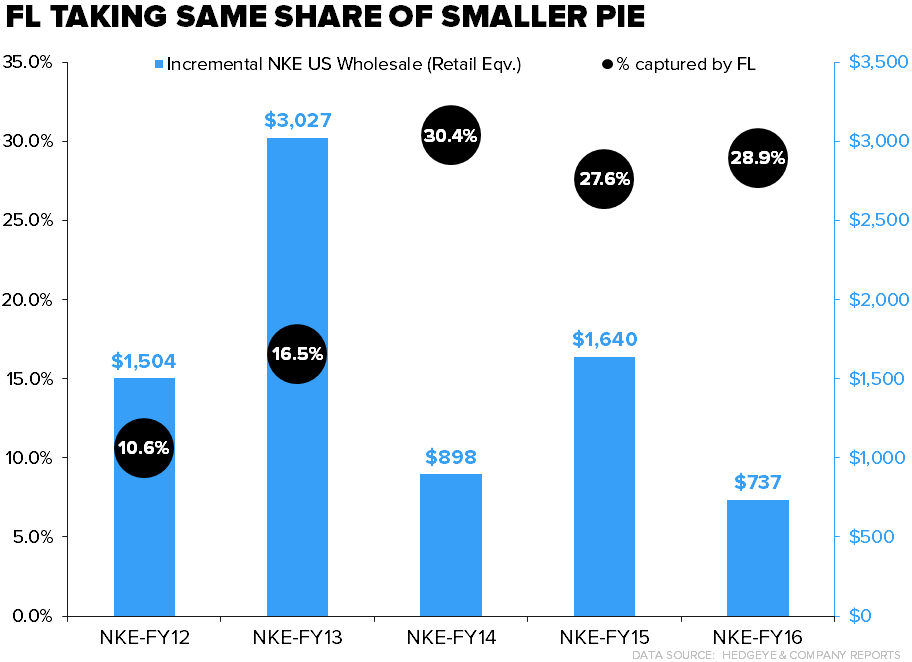

3) At retail – NKE’s NA wholesale business was up $737mm dollars. Of that $700+mm, FL captured 29%. That’s up from previous years when NKE was growing like a weed, but in line with prior two years. All in that’s an incremental $215mm to FL, good for 4% growth in its US business. That’s about half the average growth rate (8%) NKE wholesale handed to FL on a silver platter over the past 4 years. Going forward, assuming FL still gets the same allocations from Nike (despite the fact that FL was as bearish as it’s ever been on the brand in its most recent call) we think the NKE benefit gets cut in half again in 2017. ***Methodology note: we adjusted FL’s Fiscal year to more closely match NKE’s calendar.

4) Below is a year by year breakdown of the NKE/FL relationship. We think it’s incredibly important to understand the historical context in order to understand how the relationship evolves in the coming years. The punchline on all this is that we know the emphasis NKE is placing internally to grow it’s DTC business (mainly e-comm), and we can do the math to see what the risk is to FL. But, what are the options for the retailer? It can either a) take a larger share of NKE’s incremental wholesale business, or b) spend to grow the less relevant footwear brands like UA and AdiBok. The first ain’t going to happen as FL has hit it’s limit with Nike and the 2nd requires both additional investment and something we haven’t seen in a long time which is NKE losing market share.

Based on our math for FY17 (that’s 2Q-1Q for FL), using the Street’s estimates, FL needs to add an incremental $330+mm to its US business to hit numbers. We think about $130mm comes from NKE, meaning we need to see an incremental $200mm from other brands. Hint – it’s not a slam dunk. See below for a brief description of our key assumptions.

- We assume that NKE adds $1bn in NA sales in FY 17, good for a 7% growth rate.

- NKE DTC carries the weight accelerating to 20% bringing it to almost $5bn. The remainder goes to wholesale which sums up to a retail equivalent = $10.9bn up $440mm vs. $737mm in FY16.

- We assume FL captures 30% of those dollars, which = $132mm vs. $213mm in FY16.

- NKE share inside FL goes from 76% down to 74% in the US.

- That means FL needs an incremental $200mm from the likes of UA and AdiBok to hit current Consensus Estimates.

5) So what does that mean for the likes of UA and AdiBok? This scenario analysis walks through the possible options FL has to get to its 2017 numbers without the NKE benefit. Essentially anything in green (one purple) works for FL. Some brief background info: current UA NA FW sales = ~$1bn, current AdiBok NA FW sales = $2bn

One example: We’ll take the $201 number highlighted in purple. This says that: UA would need to grow FW 60% and AdiBok 20% with 50% of that growth coming from wholesale with the over arching assumption in all the calculations that FL captures 40% of the incremental share from each of the brands.

6) The only problem with those type of growth and channel assumptions is that Nike isn’t the only brand navigating around its wholesale partners. AdiBok is the worst offender with 70% of its incremental growth over the past 4 years coming from the direct channel. UA is at 32%, and we think FW growth for UA is more heavily weighted to the DTC channel. That means from here, the likes of AdiBok and Under Armour would need to take share from NKE, allocate over 40% of its wholesale growth to FL, and (not or) redirect a portion of its more profitable retail growth to the wholesale channel. A lot has to go right for that to happen.