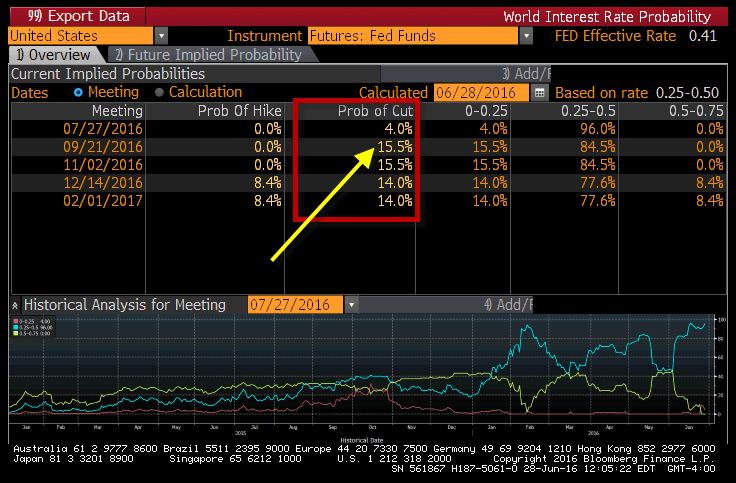

The market is now signaling a 15% chance of a rate cut this September.

(That's no typo - rate CUT ... not hike)

Take a look at this shocking about-face in the chart below. In fairly short order, the hatchet was taken to rate hike probabilities. The market now sees a 0% chance for each of the July, September and November Fed meetings. That's down from an over 50% chance of a July hike just a few weeks ago.

So the pendulum has swung to cuts.

How did This happen?

Basically, markets are pricing in our Macro team's warnings about global #GrowthSlowing. Sure, the U.K.'s vote to leave the European Union was the catalyst but, then again, it was effectively a voter referendum on lackluster growth. Post-Brexit voter analysis shows that a preponderance of the "Leave" contingent came from lower income areas and regions that derived most of their trade from the European Union.

Essentially, the promise of growth from European bureaucrats didn't live up to reality for a majority of U.K. voters.

Go figure.

GrowthSlowing Evidence?

Look no further than the 10yr/2yr Treasury yield spread. At 84bps wide this afternoon, the 10s/2s yield spread hasn't been this compressed since the Great Recession.

But What about today's upwardly revised 1Q GDP report?

It's a government manufactured mirage...

As Hedgeye CEO Keith McCullough points out, the US government effectively overstated GDP (again) today by cutting its inflation measure. Here's how that works:

To calculate real GDP, the government subtracts the "GDP deflator" (a measure of inflation) from the nominal GDP number. The GDP deflator used this go-round was 0.4%, an artificially low number by our estimation. "It should be more like 1.6%," McCullough writes. "In other words, into an Election, they understated inflation (the deflator) by 75%!"

Bottom Line?

We'll say it again, U.S. #GrowthSlowing.