The industry has been down, but its prospects are brightening.

Editor's Note: In this complimentary edition of About Everything, Hedgeye Demography Sector Head Neil Howe discusses why life insurance company shares have been beaten down since the Great Recession, but makes the case for their comeback. "Looking forward, there are a lot of positive trends at play. Gen Xers are waking up late to save for retirement, while risk-averse Millennials are trying to prepare early, promising to drive demand steadily upward for decades to come," Howe writes.

WHAT’S HAPPENING?

The life insurance industry has problems.

Or at least, what’s left of it has problems. In 1988, there were 2,343 U.S. life insurers, but by 2014 that number had plunged to a mere 830.

Sure, giants like MetLife, Prudential, Manulife, and AIG still have hundreds of billions in total assets. But investors have soured on these companies since the Great Recession. Manulife’s stock prices have dropped by two-thirds since the end of 2007. Industry heavyweight MetLife still sits well below its pre-recession peak. Lincoln Financial has lost a quarter of its value in the past year alone. As for the remains of AIG, they are in danger of being dismembered and devoured.

Earnings season sure didn’t help these companies’ stock prices. Prudential saw its total revenue slide more than 4 percent year over year. AIG badly missed Wall Street’s estimates, tallying just $0.65 in operating income per share (compared to a consensus $1.00). MetLife’s YOY earnings, meanwhile, plunged a full 9 percent.

THE BAD NEWS: MOSTLY IN THE PAST

So yes, this industry has its issues, but they’re well-known—and are already priced into the market.

“Minimum return guarantees.” Today’s life insurers are hamstrung by yesteryear’s optimism. Moody’s estimates that guaranteed products—whether life insurance policies or annuities—make up as much as 80 percent of insurers’ balance sheets. Most of these products carry a minimum payout of 3 percent or more.

What’s wrong with that? Nothing, if it’s the 1980s and the rate on 10-year treasuries is bobbing around near double digits. But today, with long-term rates sinking toward zero, these guaranteed payouts are a bleeding wound.

The “interest-rate risk” triggered by imbedded guarantees is greatest for fixed annuities, which are often locked into a single rate of return over the life of the product—as well as for “universal life” policies that accrue cash value at a fixed rate.

Demutualization. In the old days, the big mutually owned (or privately held) life insurance companies could keep their eye fixed on long-term returns. These firms could match long-term obligations with long-term assets without listening to what bean-counters might say about the changing net worth of their companies quarter to quarter.

But all that changed during the bubbly exuberance in the late ‘90s, when insurers from MetLife to Prudential thought they would be worth a lot more if they went public. And now these companies are saddled with the result: investors who constantly want to know what their stock is worth now, now, now.

In search of a higher immediate return that they could advertise to their shareholders, these newly public insurers have turned to riskier asset classes. In 2004, corporate and government bonds made up 74 percent of life insurance portfolios—a share that slid to 58 percent by 2014. Now more than ever, their assets rise and fall with each market swing—and there’s clearly been much more falling than rising going on lately.

“Too-big-to-fail” regulations. In 2014, under Dodd-Frank rules, three of the biggest life insurers by assets (MetLife, AIG, and Prudential) were classified as “systemically important financial institutions” (SIFIs)—meaning they had to meet liquidity requirements and hold more capital on hand than your average life insurer. MetLife has since wiggled out from under its SIFI categorization, perhaps opening up the door for the others to follow suit.

Competition from other savings vehicles. According to consultancy LIMRA, sales of life insurance policies have declined 45 percent since the mid-‘80s. Today, roughly 30 percent of American households today have no life insurance at all (not even a term policy)—up from 19 percent three decades ago. Most of this decline has been in “whole life” policies with a strong savings component.

Why? Competition. A century ago, life insurance was the only way a typical American family could save anything for the future. Then we added Social Security. Later we added defined-benefit pensions. And still later we added a whole array of voluntary options, from 401(k)s to IRAs. These retirement savings vehicles aren’t just plentiful: They’re efficient, easy to use, low-cost, and (often) tax sheltered.

THE GOOD NEWS: IN THE FUTURE

Sure, in the near future, life insurance will continue to suffer from its legacy problems—guarantees that are “in the money” plus competition from other forms of tax-free savings. But firms that can manage these challenges have a lot to look forward to.

The retirement savings crisis. By any measure, working-age Americans are saving far too little to retire when they plan to or with as much as they need—and they’re just beginning to wake up to that fact.

The National Retirement Risk Index shows that more than half of Americans aren’t putting away enough to retire without a steep drop in living standards.

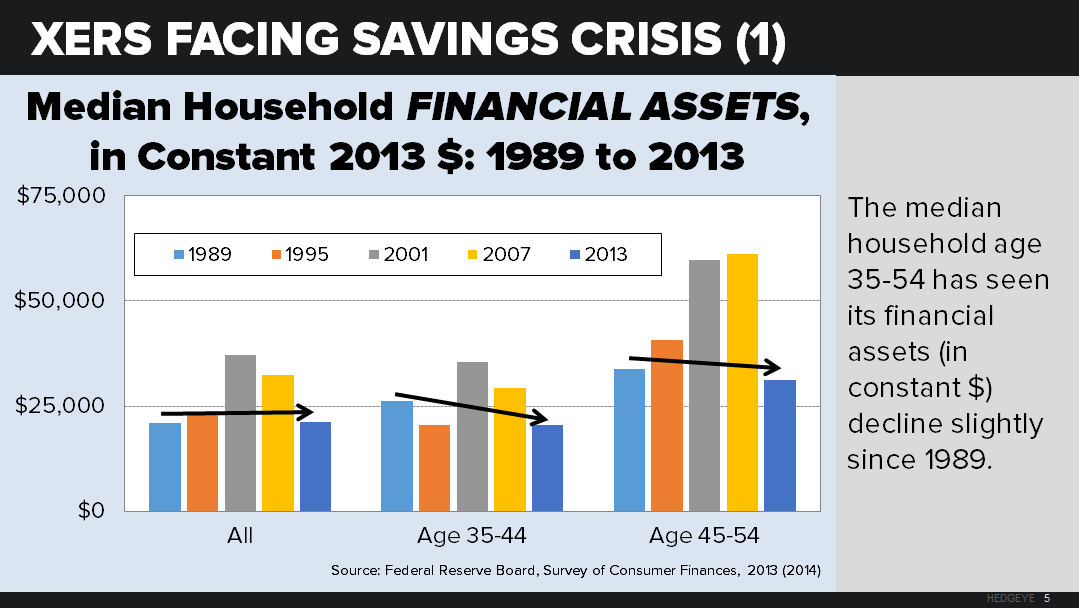

Of these non-savers, a huge share belong to Generation X. The 35- to 54-year-old demographic now populated by Xers has seen its median household financial assets slide since 1989.

And what’s worse is what’s left after all the new debt they’ve accumulated. Median household net worth has downright plummeted. Back in 1989, the typical 35- to 44-year-old household had a net worth about $100,000 (in today’s dollars). Now it’s below $50,000. Net worth among 45- to 54-year-olds have dropped by nearly half as well.

How is this generation ever going to retire? Keep in mind that public retirement benefits are going to become stingier, not more generous, in the years to come—as today’s breaking age wave puts ever more pressure on Social Security, Medicare, Medicaid, and related programs.

My conclusion: Gen-Xers will have no choice but to ramp up their savings steeply in the years ahead. And much of these new savings will flow into products offered by the life insurance industry. Indeed, over the last three years the personal savings rate has already been rising. This rise will continue—putting some deflationary drag on the economy as a whole, perhaps, but enabling millions of 40- and 50-something households to repair their balance sheets.

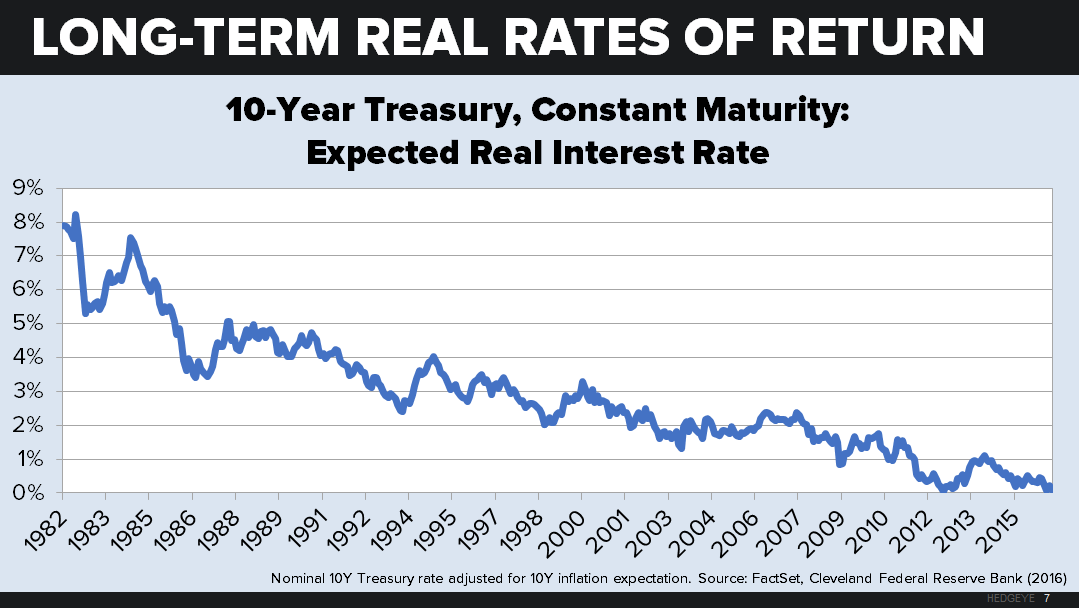

Low rates of return. Life insurance execs complain a lot about low long-term rates—not just because of the hit they take in guaranteed payouts, but also because they think it makes their products look unattractive. These worries are unfounded. Quite simply, everything looks unattractive nowadays.

In fact, low rates could easily cause people to save more. In the short run, sure, low interest rates suppress savings. But in the long run—once everyone expects low rates to continue indefinitely—the correlation reverses. (The world’s ZIRP- and NIRP-fixated central bankers have yet to figure this out.) Households and pension funds eventually realize they must put away more money each year to hit their retirement targets. Plus, workers in a low-interest-rate environment can’t count on their own income to grow as fast in the future—which further boosts the need for extra savings.

Favorable demographics. From the ‘90s onward, Boomers moving into midlife have helped push much of the life insurance industry away from its traditional whole-life product line and toward various kinds of annuities. Now, as Boomers move past age 65, that strong demand for annuities is fading.

Meanwhile, the demographic tide is about to turn. Census population projections show that, over the next fifteen years, Millennials will swell the ranks of 30- to 39-year-olds and then the ranks of 40- to 49-year-olds. This will provide a much-needed boost in demand for traditional life insurance.

Generational change. More than just their sheer number, Millennials’ cautious worldview will fuel even greater demand for life insurance.

For starters, they’re already saving as much as possible to avoid falling into the quicksand of retirement catch-up that they’ve seen happen to so many of their parents. In this effort, life insurance is one more way to save.

But life insurance isn’t just another savings vehicle for Millennials. This generation also wants to be protected from risk—which is the name of the game for life insurers. For Millennials, there’s no such thing as “playing it too safe.” Many are already buying whole-life insurance well before the age at which they’re likely to use it. In the workplace, they’re fueling new demand for voluntary life insurance policies that will keep their loved ones solvent no matter what happens. Among workplace benefits, according to a 2015 survey by the Employee Benefit Research Institute, Millennials are the only generation that regards life insurance as important as retirement savings.

It’s not just married Millennials, either. Some single twentysomethings are taking out policies as well, just in case—presumably to reimburse Mom and Dad for all those years of rent-free living.

In fact, insurers could even leverage this need for protection into a service that walks Millennials through everything they need to know about finance—in which life insurance is just one piece of the puzzle. Look no further than Massachusetts Mutual’s “Society of Grownups,” a program chalk-full of whole-life advice for prudent young consumers. (The tagline: “Helping you find your inner adult.”)

TAKEAWAYS

- Up until recently, life insurers have been plagued by difficult challenges. Their guaranteed products have left them vulnerable to “in the money” payouts. They’ve also been pressured to prove profitability to their shareholders amid a long-term slide in the demand for their flagship products.

- But looking forward, there are a lot of positive trends at play. Gen Xers are waking up late to save for retirement, while risk-averse Millennials are trying to prepare early, promising to drive demand steadily upward for decades to come.