“We have what it takes to take what you have.”

-Suggested Federal Reserve Motto

Recently promoted to Senior Hedgeye Partner, Kevin Kaiser (MLP analyst who called the Linn Energy bankruptcy which was filed last night), and I spoke at one of the world’s largest investment bank’s High Net Worth division’s dinner last night in NYC…

So I’m running a little late this morning. But I do want to thank everyone who has supported us since starting the firm in 2008. Our audiences continue to grow. And, instead of getting complacent, we need to work harder than we ever have to earn your respect.

While I do not like to make a habit of being late, fortuitously that is working in the favor of our #ConsumerSlowing call this morning as one of our favorite non-MLP-ponzi shorts, Kohl’s (KSS), is imploding. There’s always a bear market somewhere.

Back to the Global Macro Grind…

While it should surprise no one who has been on the right side of the US economic, profit, and credit cycle call that the #LateCycle Sectors of the US Economy (Financials, Consumer Discretionary, Tech, Healthcare) are the biggest dogs for the YTD, the pace of the decline in the US Retail (XRT) sub-sector of consumer has caught many off-side this week.

Taking a step back, don’t forget where US Consumers (70% of GDP) were at this time last year:

- US Employment Growth (NFP) was putting in a cycle peak

- US Consumer Confidence was putting in a cycle peak

- US Consumption Growth was putting in a cycle peak

Peak. Peak. #Peak!

And what happens when you start to lap the cycle peak? Well, instead of crappy Baby Boom capacity putting up mediocre (barely positive) same store sales at the peak, they look even crappier on the back side of the cycle.

Not to pick on Kohl’s (KSS), but now that LINE is a bagel, I have to pick on something with market cap. KSS missed the top-line (same store sales were DOWN -4% year-over-year) and EPS came in at $0.31 vs. an Old Wall “expectation” of $0.37/share.

Ah, but “it’s cheap.” Yep. Getting cheaper. And no they can’t turn themselves into a “REIT.”

What happened?

- Was it fantastic East Coast weather that kept people from buying Spring inventory?

- Was it the competition “taking share” when Macy’s (M) and Gap (GPS) comped down -6-7%?

- Or was it that “Ex-Energy”, rising gas prices didn’t stimulate the consumer?

I know Ed, it’s getting real tough to follow the narrative drift that “falling gas prices” were going to be a US consumption panacea in the 2H of 2015… and now rising gas prices are going to keep the stock market up.

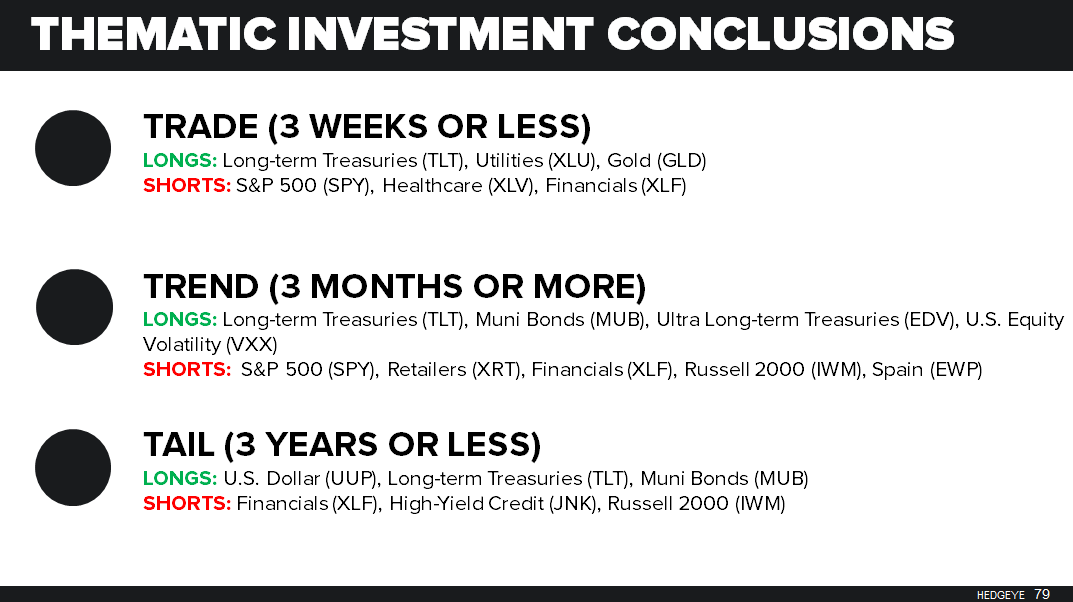

Not that we like to #timestamp and hold ourselves to account on our big macro themes calls or anything, but in our Macro Themes Deck (see Chart of The Day) we make our best ideas, across durations, very clear. Here are our Best TREND Shorts:

- Financials (XLF)

- Retail (XRT)

- Russell 2000 (IWM)

- SP500 (SPY)

- Spain (EWP)

You won’t hear this from many guys/gals who were trying to push these US Retailers as “value” and/or “real-estate plays”, but reality is that US Retail (XRT) is on the precipice of #crash mode at -18.4% since we went bearish on Consumer and SPY in July of 2015.

Nope. Instead, I’ll hear a lot of whining. But why? Why is it so hard for everyone at SALT and SOHN to just belly up to the bar and short “cheap”? Mr. Market is telling you these stocks aren’t “cheap”, if you have the analysts who can price the stocks on the right #ConsumerSlowing Cycle numbers.

I spent a whole day in NYC yesterday hearing about why Utilities (XLU) are “too expensive.” That’s code for “I missed it and I’m not long it.” But why? Why is it so hard for so many smart people to understand that expensive Low Beta Slow Growth exposures get even more “expensive” during the #GrowthSlowing surprise part of the cycle?

Does consensus realize how #GrowthSlowing => Down Dollar => Up Oil => Down Consumer flows to our Street low US GDP forecast?

It puts downward dog bias to our forecast as there’s currently an upward bias to what is called the GDP Deflator. In Q1, the US government got away with using 0.7% as the Deflator (you subtract that from nominal GDP to get Real GDP).

The Fed’s own preferred calculation of inflation = +1.6%. If the BEA used that in the official calculation, Q1 GDP wouldn’t have been as negative as Kohl’s or Costco’s traffic, but it would have been negative. And #Recession would be knocking on The Big O’s door.

Like any other tax, devaluing the purchasing power of The People (US Dollars) is an obvious tax on consumption. The un-elected Fed and their Old Wall cheerleaders have whatever it takes to take away whatever savings consumers have left.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.70-1.79%

SPX 2040-2088

RUT 1096-1141

USD 92.52-94.99

YEN 105.39-109.33

Oil (WTI) 42.59-46.93

Gold 1

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer