Believe It When You See It: Productivity Growth is Slipping.

Editor's Note: In this complimentary edition of About Everything, Hedgeye Demography Sector Head Neil Howe explains why the much-debated productivity shortfall – amounting to $3 trillion – is "simply far too vast to pin on mismeasurement." Howe suggests, "It’s time to take the productivity slowdown seriously" and explains the broader implications for investors.

WHAT’S HAPPENING?

For years now, Silicon Valley techno-optimists have been telling us that our dismal productivity numbers are wrong. They’ve said that technological gains are enriching our lives in ways that are simply impossible to measure.

On the surface, they appear to have a point. After all, how could innovations like robotics, AI, and the sharing economy not boost productivity? Plus, as tech heavyweight Erik Brynjolfsson likes to point out, Americans have access to ever-more free web services that aren’t counted by GDP. I’ll be the first to admit it: I’m blown away by Wikipedia.

Well, the latest in a series of Brookings Institution reports (see especially the paper by economist David Byrne et al.) blows these arguments out of the water. It turns out that the vast shortfall in recent real GDP growth due to falling productivity—amounting to $3 trillion—is simply far too vast to pin on mismeasurement.

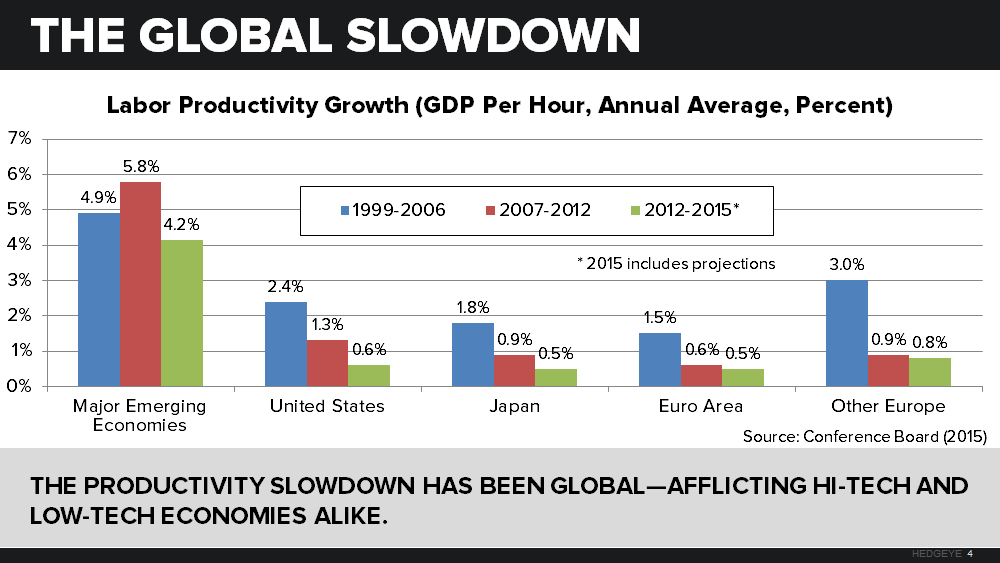

So yes, those dolorous productivity numbers you see in the media should be taken seriously. With the single exception of the dot-com revival (1995-2004), real worker output per hour has been decelerating ever since the end of the post-WWII American High.

The past few years have been particularly dour. After peaking at over 3% per year in the early ‘00s, productivity growth over the last decade has been closer to 1%, with plenty of quarters of negative productivity growth mixed in.

Brookings thoroughly debunks Silicon Valley’s mismeasurement hypothesis. First, the productivity decline has taken place across all industries, not just IT. Additionally, IT employs too small a share of our workforce for mismeasurement to have a large positive impact on real GDP. Further, if the mismeasurement of high-tech creativity were the main story, we wouldn’t be seeing a global productivity slowdown spanning countries at vastly different stages of technological advancement.

The techno-optimists believe that we’ve been wildly overestimating inflation, and that—correctly measured—the “real” living standard of the typical American has actually been rising swiftly in recent years. Really? Try selling that celebratory news to Bernie and Trump supporters. (Personally, I’ve never met a techno-optimist whose income is anywhere near that of the median American adult who never completed college. And these comprise roughly three-quarters of all adults.)

WHY IT’S HAPPENING: DRIVERS

It’s time to take the productivity slowdown seriously. Here are some possible explanations.

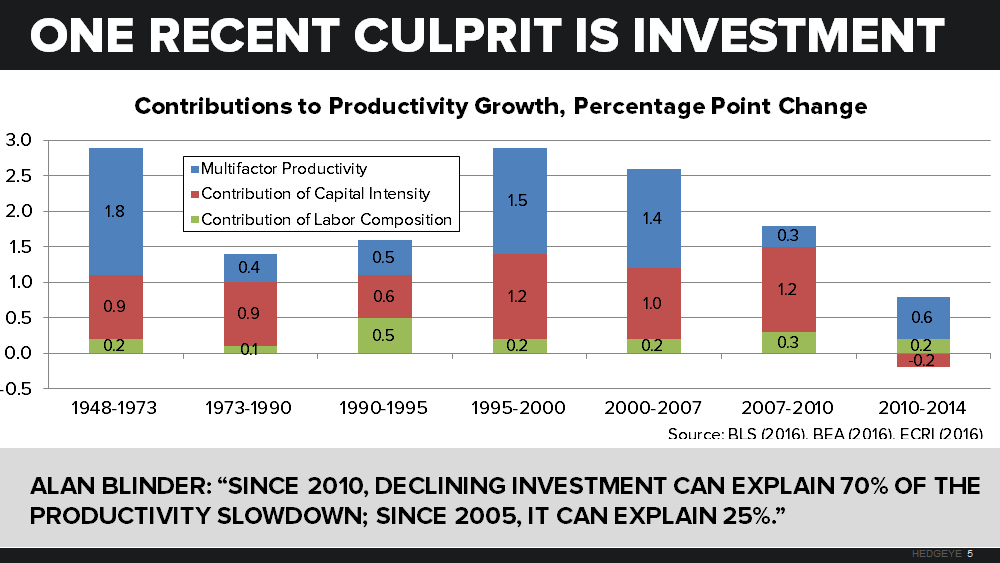

Declining investment. Companies aren’t spending on capex like they used to—and it shows. A quick look at BLS aggregate hours and BEA capital stock data shows that, since 2010, capital intensity (the ratio of capital to hours worked) has actually declined.

Former Fed Vice Chairman Alan Blinder attributes a whopping 70 percent of the productivity slowdown since 2010 to weak investment.

Baumol’s cost disease. Industries with slow productivity growth are making up an ever-greater share of employment. Health care, education, and retail have together ballooned to roughly a third of total U.S. worker hours—roughly five times greater than the manufacturing share, which continues to shrink.

A lack of true innovation. Prominent analysts like Tyler Cowan and Robert Gordon (check out the latter’s new best-seller, The Rise and Fall of American Growth) say that the technological innovations we’re seeing today are much less impactful than the foundational discoveries of the late-19th and early-20th centuries. After all, what’s Facebook, Twitter, or Tinder compared to electricity, automobiles, hydraulics, or refrigeration?

If you think your kids pout when you take away their mobile phone, try taking away any processed foods, any hot water, any illumination after dark, and any motorized help getting to school. They may yet come around to Robert Gordon’s point of view.

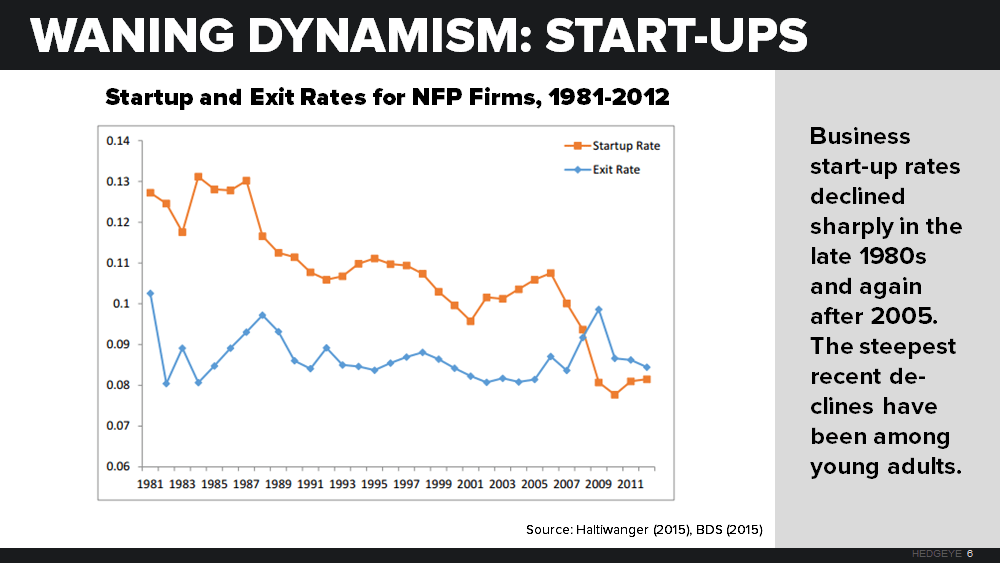

Waning business dynamism. Many economists suspect that the American economy is also suffering from declining “dynamism,” as measured by a variety of risk-taking and mobility indices.

For example, startup activity is down. The U.S. firm entry rate is barely half of what it was in 1978, and over the last decade, for the first time ever recorded, more firms disappeared than were created.

We’re also seeing a stagnant job market. The job reallocation rate (job creation plus job destruction) has fallen steadily since 1990.

Workers of all ages are also moving between jobs a lot less than they used to.

Some economists suggest that declining dynamism may be symptomatic of a deeper problem—declining competitiveness. Indices of market concentration by industry have risen substantially over the past 15 years.

Exhibit A: The total number of listed companies has dropped by half over the past 20 years, while the Fortune 500 (or the Fortune 100) account for an ever-growing share of total U.S. corporate revenues.

Demographic aging. An aging society is inherently less dynamic, since older adults work less—and aren’t as entrepreneurial—compared to their younger counterparts. What’s more, the youth generation that should be starting its own businesses, Millennials, simply aren’t. For better or worse, Millennials are risk-averse. Most would rather take a secure, benefit-laden “position” at a large firm than go it alone and risk abject failure.

BROADER IMPLICATIONS

Silicon Valley is waiting for productivity gains to “kick in”—but that’s no sure thing. Techno-optimists cite a “lag” between the time when a new technology arrives and the moment it starts boosting productivity. It took 40 years for electricity to result in productivity gains, after all.

So is it just a matter of time? Not if you believe the markets. The real yield-to-maturity on a 30-year Treasury bond sits under 1 percent today, meaning that the outlook of long-term investors on productivity is every bit as bearish as the economists.

Work culture is growing ever-more inclusive. American corporations don’t hire outsiders like they used to, instead preferring to send their own to corporate universities and promote from within. The business world’s new emphasis on “cultural fit” may help explain why worker churn is lagging.

Declining dynamism may reflect declining competitiveness—and explain a central paradox of today’s ZIRP/NIRP era. When you consider that businesses and workers are stuck in place, it suddenly makes some sense why we’re seeing the unprecedented combination of near-zero interest rates, soaring valuations, high ROR on book-value assets, and tepid investment. It doesn’t pay to fight your way into a market where only a few privileged incumbents dominate—no matter how little it costs to borrow.

TAKEAWAYS

- Recent research vindicates the nerdy economists over the “next big thing” techno-optimists in the productivity debate. The slowdown is happening. It’s a serious threat to our economic future.

-

Long-term market expectations: The real yield on 30-year bonds (nominal minus expected inflation) may be a rational long-term assessment—not just a spasmodic and temporary reaction to global QE. Feeling lucky, kid? Go ahead, short those bonds.

- Investors should assess how weak productivity growth may depress the long-term return on their portfolios—and elevate the popularity of radical political programs among voters who have lost patience with stagnant living standards.