Editor's Note: Below is a research note on the oil industry and ongoing OPEC developments from Potomac Research Group Senior Energy analyst Joseph McMonigle.

While we certainly expect that speculators will be swayed by the Doha discussions, we are highly skeptical that any meaningful agreement will be reached or that it changes the outlook for oil markets.

We view the freeze as OPEC's version of vaporware for two main reasons:

- A freeze is not a cut; and

- A freeze without Iran is not a freeze.

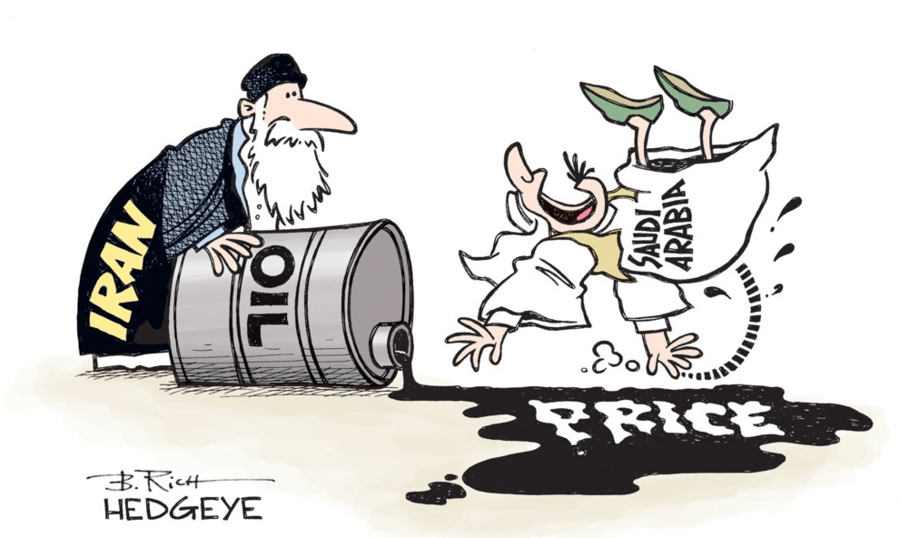

With Russia and many OPEC countries at or near maximum production amounts, a freeze will only continue the supply glut and add to record crude inventories.The freeze would only be meaningful with Iran's participation which is the only producer capable of ramping up production. But Iran has made it clear that it won't participate and even freeze proponents now concede that any agreement will exclude Iran.

There are increasing signs that Iran is achieving its production goal. An official at the state-owned National Iranian Oil Company said on March 2 that February's crude exports had reached 500,000 bpd, and it expects an additional increase in March of 250,000 to 350,000 bpd. Shipping sources have also supported increased Iranian exports but we will standby for more independent confirmations.

Bottom Line

On June 2, OPEC will meet for its regularly scheduled meeting. We continue to see no chance of a production cut at this time and maintain our thesis that Saudi Arabia believes its market share policy is winning.

CLICK THE IMAGE BELOW TO WATCH MCMONIGLE ON BloombergTV