Editor's Note: Below is a brief update and recap on our Foot Locker call. For additional analysis or other related research from our Retail team led by Brian McGough please ping sales@hedgeye.com.

Following Wednesday’s updated Best Short Idea presentation by Hedgeye Retail analyst Brian McGough, Foot Locker (FL) posted decent to good numbers.

However, most metrics look sequentially worse including FL’s margin of EPS upside relative to expectations. The flow through in profitability is less than half of where it trended 3 and 4 quarters ago. And from here, compares get increasingly tougher.

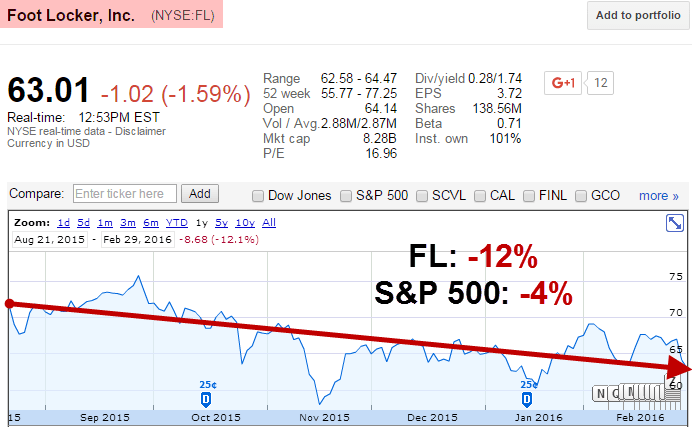

Since McGough added FL as a Best Ideas Short, the company is down -12% versus -4% for the S&P 500:

Comp trends were disappointing in February, at a low-single digit rate month-to-date even though:

- There was a sequential uptick in Nike/Jordan launches this month versus last, and;

- Feb 2015 was disappointing – so it faced an easy comp. i.e. there’s an increasing bifurcation between Nike’s solid release schedule and FL results.

That’s bad.

The steady sequential decline in e-commerce is unsettling to say the least. Given base levels of industry growth in the US in conjunction with our estimate of how Nike channel distribution will change, we think that Nike’s US Wholesale revenue base will shrink by $1 billion (retail equivalent) by 2020.

The only way FL wins in that context is to become a wholly-owned subsidiary of Nike. That obviously won’t happen. FL is likely to miss six out of eight quarters from here without a significant downward guide, not to mention the re-valuation that will come with it – we expect this to be a slow but steady bleed.

Bottom line: We think FL will struggle to generate $4 in EPS over the next 2-3 years, suggesting 25%+ downside risk from here.

Click here to watch a brief video summarizing FL's earnings:

To read more analysis on Foot Locker or other research from our Retail team ping sales@hedgeye.com.