The late-cycle domestic macro data continued its slow, deceleration-ary march this morning with the Durables Goods and Income/Spending data for November.

As we continue to stress, “late-cycle” is a process not some discrete point on a macro sine curve and as the cycle traverses its twilight the rate-of-change peaks across a growing number of metrics continue to roll-in.

To summarily review the majors:

- Employment: Employment growth peaked in February 2015 and has been slowing since. Employment growth is hostage to the law of large numbers and will invariably slow alongside tighter labor supply and a growing employment base as an expansion matures. A negative inflection in employment growth doesn’t herald an imminent recession but, empirically, it’s a one way street as the cycles progresses past peak and onto eventual recession. The labor trend matters insomuch as it’s the principal driver of all things consumption and investment …..

- Income Growth: Income Growth peaked in 4Q14/1Q15 alongside peak acceleration in employment growth and modest gains in earnings. Absent a material acceleration in credit growth, income growth drives the capacity for and trajectory of consumption growth. Indeed, income growth and the change in the savings rate carrying >0.95 correlation to household consumption growth across decades of data . Aggregate wage and salary income remains a particularly pronounced driver of consumption in the present cycle with credit growth remaining modest and the long-term capacity for consumer re-levering to drive incremental consumption growth remaining constrained. Aggregate income growth will remain positive over the nearer-term but will continue to slow against steepening comps

- Consumption: Consumption growth peaked in 1Q15 alongside the peak in employment and income growth. Again, absent remarkable changes in the savings rate and/or consumer credit growth, consumption growth will follow the slope of aggregate income growth. Household spending growth will remain “okay” on an absolute basis over the nearer term but will continue to slow alongside slowing income trends and tougher base effects. (recall – Macro cares about the slope of the line and the 2nd derivative trend will remain negative)

- Corporate Profitability: Both Corporate Profitability as a % of GDP and S&P500 operating margins peaked in late 2014 and have retreated since. Past peak profitability, persistent strongdollar deflationary pressures, negative growth/inflation revision trends and a broad expectation for higher labor input costs is not the stuff multiple expansion or lazy long allocations are made of.

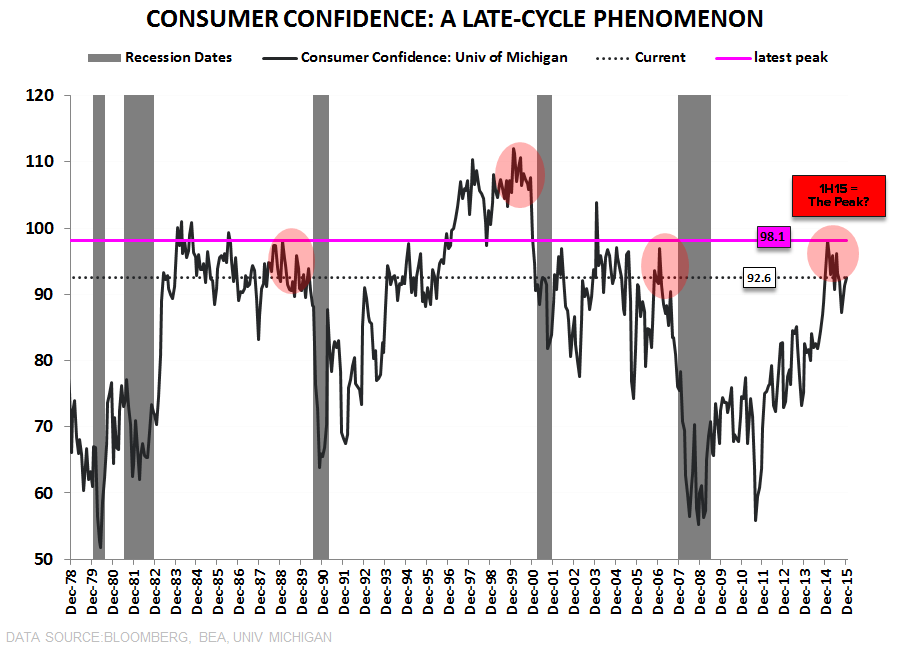

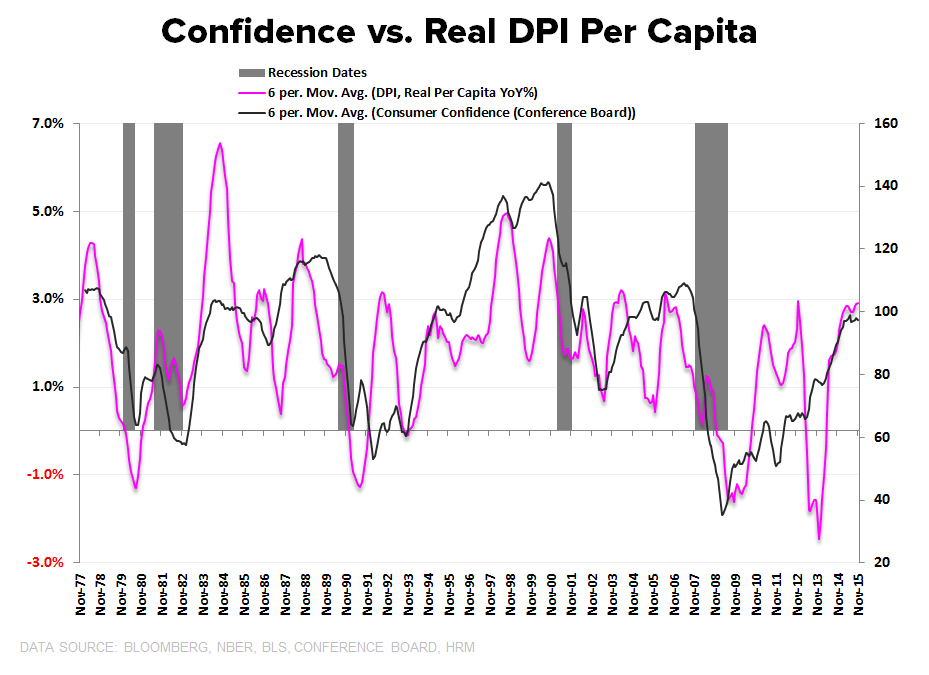

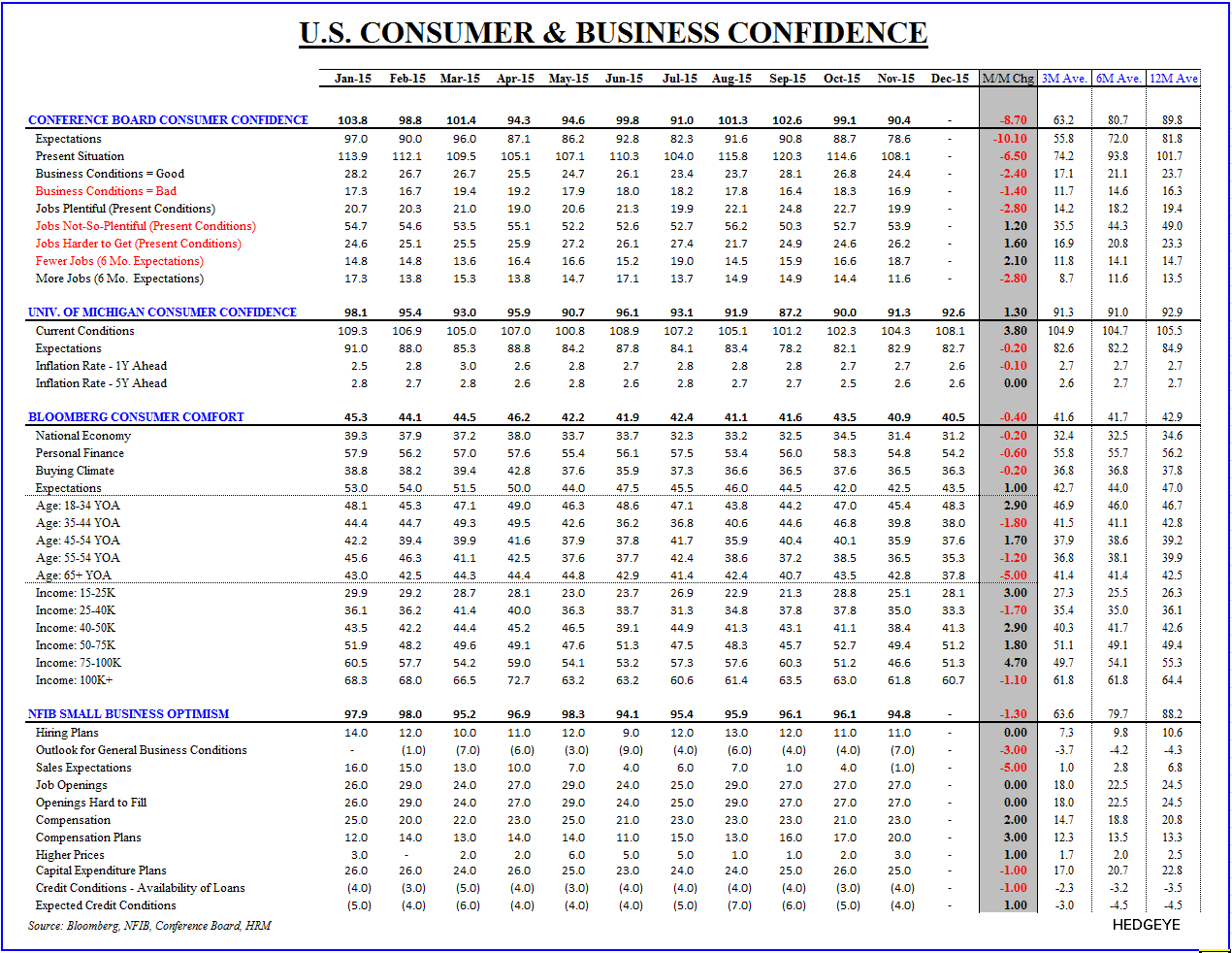

- Confidence: Consumer Confidence across all the primary series (Conf. Board, Univ. Mich, Bloomberg) peaked in 1H15 and have since backslid. Confidence peaks late-cycle and, unsurprisingly, peaks alongside the peak in real per capita disposable income growth (i.e. when the most people are realizing their greatest income flow) and Per Capita DPI appears to have peaked in 2Q/3Q15.

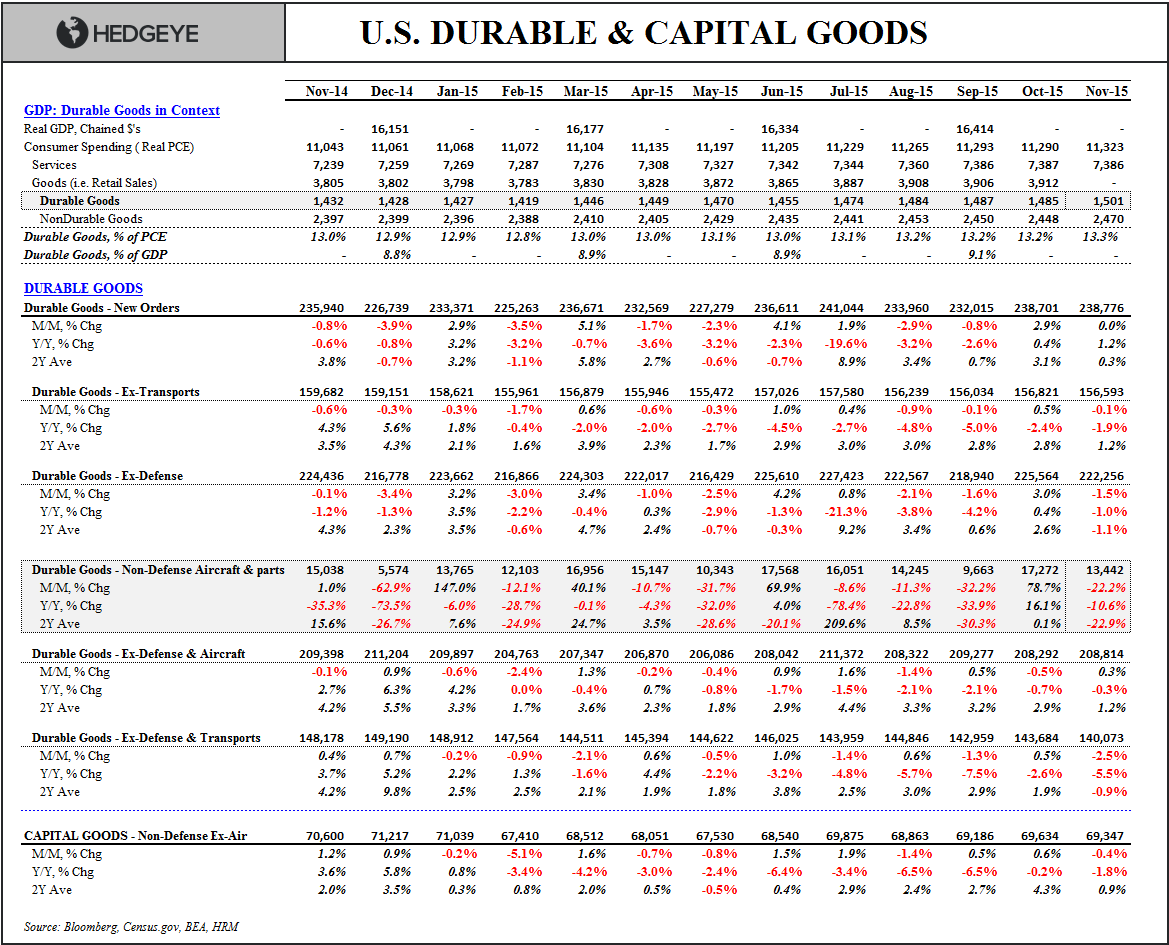

- MFG/Industrial: With the ISM printing in contractionary territory and Durable Goods and Capex Orders growth negative for most of the last year, the domestic manufacturing data has been conspicuously recessionary. The collapse over the TTM, of course, is now the 2016 comp but given further OUS slowing, another step function lower in oil/energy/commodity prices and another wave of investment and labor realignment across the energy and mining spaces, the trend there is likely to get worse before it gets better.

The November Detail:

Consumption: Household spending grew +0.3% MoM in November (after declining in October for the first time in 21-months) but decelerated on both a 1Y/2Y basis for a 2nd consecutive month as the savings rate held at a multi-year high (5.5%) and income growth decelerated further.

Income: Both DPI and aggregate Salary and Wage Income decelerated on a 1Y and 2Y basis as the dynamics highlighted above continued to define the 2nd derivative trend. Income growth should continue to decelerate from here against peak comps into year end.

Durable Goods: Headline Durable Goods Order growth decelerated to +0.0% sequentially but managed a second month of modest year-over-year acceleration. The improvement was largely a comp effect – and one that should remain a support to reported growth as we comp negative growth in 8 of the next 9 months.

Under the hood, Core Capex Orders continued to slump - recording negative growth for the 10th consecutive month and decelerating on all of MoM/1Y/2Y basis in November. Much like inflation's 4-year run of below-target "transience", the great capex renaissance remains 'just around the corner' and very much a phantasm.

Also concerning is the prevailing trend in Durable Goods Ex-Defense and Aircraft - which represents the stuff the average household actually buys – which saw a 7th straight month of negative YoY growth.

Darkness: In other, random positive inflection news, with the winter solstice now rearview, we're past peak on shortened daylight. Global luminary forces in the northern hemisphere will again marshal Mother Nature and her celestial minions to progressively overtake the oppresive fetters of the darkside ... so there's that, at least.

A visual tour of this morning’s data along with the historical cycle context below

Christian B. Drake

@HedgeyeUSA