“The essential ingredient of politics is timing.”

-Pierre Trudeau

For those of you not familiar with Canadian political history, the "Trudeau salute" was a middle-fingered gesture former Canadian Prime Minister Pierre Trudeau gave to protestors in Western Canada in the early 1980s. To Western Canadians at the time, it was symbolic of years of policy that undermined their commodity laden economies.

Yesterday, Canadians elected Justin Trudeau, the 43-year old former son of Prime Minister Pierre Trudeau, as their next Prime Minister. This was as much an election that rejected Prime Minister Stephen Harper as one that voted in the relative neophyte, Trudeau.

Trudeau’s victory marks the biggest political rebound in Canadian history. The Liberals become the first third-place party to win an election, and the party’s seat gain from the prior election of around 150 is the largest ever. In fact, the Liberals, who had governed for about two-thirds of the 100 years before Harper came to power, won just 34 districts in the 2011 election, the worst result in their history.

After almost 10 years of Conservative rule, the Canadians wanted change. And change they have elected, in an epic way. Some would even argue with an emphatic middle finger to the departing Prime Minister.

Prime Minister-elect Trudeau has basically indicated that his economic policies will be built around two key points: raising taxes on those making over $200,000 and increasing government spending on infrastructure. (Incidentally, he also intends to legalize marijuana quickly, which is clearly a priority for a nation in recession.) By and large, Trudeau will be taking a page right out of the Keynesian playbooks of many European countries.

Back to the Global Macro Grind...

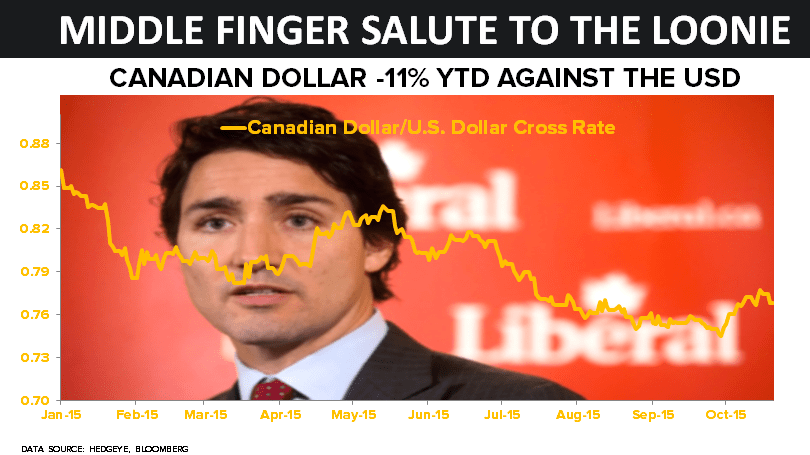

From our purview, it is difficult to see in the short run how Trudeau will have a positive impact on the Canadian dollar or economy. In part, of course, the Canadian dollar has front run this and is down about 11% over the last year, but with a deficit that is likely to expand, the floor has probably not been established for the Loonie.

There is a more significant issue facing Canada than a collapsing currency, which is the state of the Canadian banking system. Our financials team introduced their call to short the Canadian Banks this summer and in an update note in late September wrote the following:

“You would think that with the Canadian economy in recession, energy prices tumbling, Oil & Gas loan impairments skyrocketing, and the whole Canadian housing market sitting atop an historic bubble, the Canadian banks would be at Defcon 4: building reserves, speaking cautiously, slowing loan growth. Instead, however, management(s) couldn't be more unconcerned, disinterested, and generally indignant at the mere suggestion that risk is rising.

Over the last two weeks the big six Canadian banks (BMO, RY, NA, CM, TD, BNS) and CWB reported their fiscal 3Q15 earnings. Generally speaking the results were not terrible. There were four beats, two misses and one in-line print.

Part of the reason the results weren't terrible is that the banks continue to avoid taking reserves against future losses. There's no better example than in the Oil & Gas patch. A major focus of Canadian bank earnings conference calls over the past two weeks was the effect (or supposed lack thereof) of low oil prices on the Canadian economy and on bank earnings. The consensus from management teams is that it’s no big deal, and their lack of concern concerns us. We can't help but be reminded of Aesop's The Ant and the Grasshopper fable. In a word, the Canadian banks are Grasshoppers, all.”

In light of yesterday’s election results, we’d recommend you email to review our work on the Canadian banking system and set up a call with our financials research team. The short thesis is timely this morning.

Canada isn’t the only sovereign we have concerns about in the current environment of political change. In fact, tomorrow we will be doing a call on Spain, which has been a perpetual weak economic link in the Eurozone. Similar to Canada, Spain has an important election scheduled on December 20th. On the call, Hedgeye contributor Daniel Lacalle, a former buy-side PM at PIMCO and Citadel, will talk through his scenario analysis on Spain.

In contrast to Canada, Spain has been under Conservative rule for the last four years. In that time period, the Conservative Party (PP) unwound years of deficit spending from the previous administration. In fact, the PSOE had left a deficit of 9% of GDP after promising a maximum of 7%.

As Lacalle has written, when the socialist government left office, Spain had more than 40 billion euro in unpaid invoices from the public administrations to the private sector, the public savings banks presented a capital requirement of 100 billion euro and the regions and municipalities faced a bailout of 125 billion euro. To many, this was seemingly an insurmountable situation.

However, after a large austerity plan that was split 50% in tax increases and 50% in spending cuts, and a very substantial set of reforms, including the financial sector, labor market, entrepreneurship programs and early payment schemes, Spain recovered.

Between 2014 and 2015 Spain started to grow well above the EU average. It led job creation in the Eurozone, with more than one million jobs, and brought unemployment rates back to September 2010 levels. It went from a massive trade deficit to a balance by 2015.

In summary, Spain undertook the largest adjustment seen in an OECD economy, 15 points of GDP, and managed to do so growing and creating jobs. But as austerity is prone to do, it does make some folks unhappy. As a result, much like in Canada, the December 20th election in Spain will be referendum on the Conservatives. And with political change, comes investment opportunity. After all, the great thing about being stock market operators is that we can go both ways.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.98-2.08%

SPX 1

VIX 14.94-20.69

Oil (WTI) 45.08-47.99

Gold 1144-1195

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research