Editor's Note: Below is an abridged breakdown of this morning's labor data from Josh Steiner and our Financials team. If you would like to setup a call with Josh and his partner Jonathan Casteleyn, or trial their research, please contact sales@hedgeye.com

* * * * *

Consider a turkey that is fed every day. Every feeding will firm up the bird's belief that it is the general rule of life to be fed every day by friendly members of the human race 'looking out for its best interests,' as a politician would say. Then, shortly before Thanksgiving, something unexpected will happen to the turkey. It will incur a revision of belief.

- Nassim Taleb, The Black Swan

Just like Taleb's Turkey, initial jobless claims "appear" on solid footing below 300,000. However, the stark reality is that we're drawing inevitably closer to Thanksgiving Day ... and the market is, of course, the Turkey.

The Transition

The current labor market trend shows a subtle shift from great to good.

Initial claims, put in their low watermark ~6 wks ago and are now in a 1.5 steps back, 1 step forward re-convergence higher, moving back toward 300k. While anything sub-300k isn't "bad" per se - remember, it's what happens on the margin that counts. This is especially true when the market is stretched on longer-term valuation metrics and is entering the upper echelons of historical bull market duration.

Outside of claims, yesterday's ADP print came in light vs expectations at 190k (consensus was looking for 210k) and this happened last month as well when consensus was also looking for 210k and ADP delivered 185k. On the NFP front, the last two months (June/July) have been in-line with expectations, but that actually follows the same great to good pattern, as the May NFP print was a 280k blow-out (consensus was 220k).

The Data

Prior to revision, initial jobless claims rose 11k to 282k from 271k WoW, as the prior week's number was revised down by -1k to 270k.

The headline (unrevised) number shows claims were higher by 12k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims rose 3.25k WoW to 275.5k.

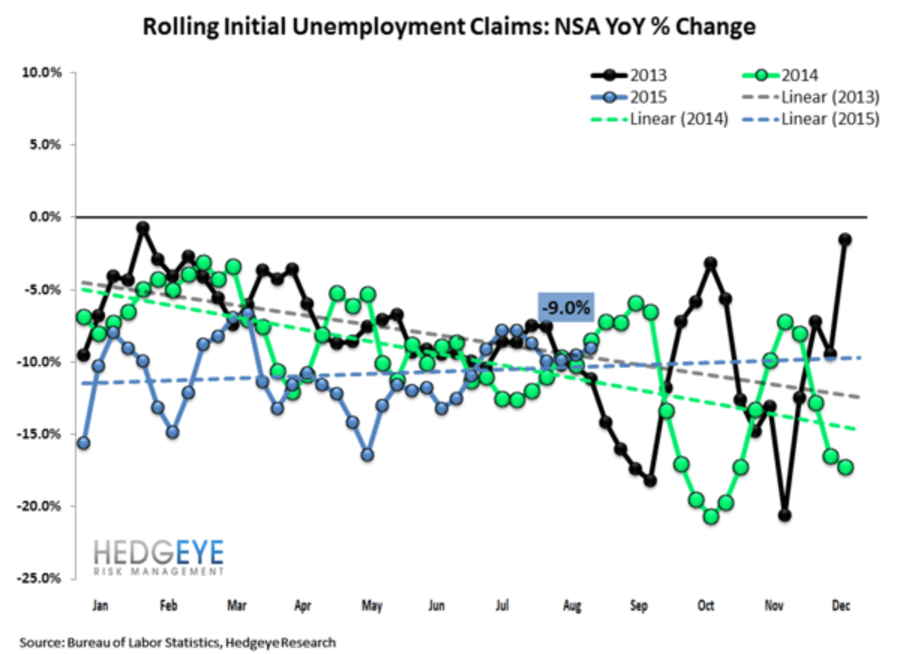

The 4-week rolling average of NSA claims, another way of evaluating the data, was -9.0% lower YoY, which is a sequential deterioration versus the previous week's YoY change of -9.5%.

The Cycle

It's not easy to tease out exact causation here, but a few possibilities come to mind. One possibility is the inevitability of late cycle reality --> great becomes good (early late cycle --> mid late cycle) and then good becomes less good (mid late cycle --> late late cycle) and, eventually, less good becomes bad (late late cycle --> recession). Another possibility is that the confluence of fears from real energy sector headwinds, August market weakness and rising Global Macro uncertainty are conspiring to facilitate that first shift downward from great to good. It's also possible (likely, even) that the latter is simply this cycle's causal factor for the former.

The Bottom Line

Like an old broken record, we're here to remind you again that it's late cycle and it's time to start preparing for the inevitable cyclical downturn.