“The magician and the politician have much in common: they both have to draw our attention away from what they are really doing.”

-Ben Okri

But what could the Eurocrats really be doing beyond perpetuating a political ‘crisis’ in the Eurozone?

Interestingly, according to a new Opinium poll, only 14% of Brits, 17% of Dutch and 24% of French believe that the EU countries “should continue to progress towards ever closer union” and transfer more powers to Brussels.

What does this poll suggest?

It’s another confirming signal that the Eurozone project has failed. Like it or not, the union of uneven countries (today composed of 19 member states) guided under one monetary policy is deeply flawed; and the economic, political, and cultural divides across countries is not abating. The United States of America, therefore is not an apt analogy for the Eurozone.

Back to the Global Macro Grind…

But would any Eurocrat come out and say this? Not if they want to keep their job.

A great expose on Greece’s ex finance minister, Janis Varoufakis, in The New Yorker titled in jest “The Greek Warrior” reveals from the man himself the great political chicanery between the Greek government and those of the Eurozone member states around the most recent (3rd) bailout.

Varoufakis says the 19 governments could be divided into 3 groups:

- “There is a very small minority that believes in austerity, and in this program. Germany leads this minority.

- A second group – Ireland, Spain, Portugal, the Baltic states — has pursued austerity programs, and now fears that Syriza, if successful, would leave those countries exposed to radical domestic opposition.

- Then there’s another group, of substantial countries like Italy and France—especially France—who don’t believe in austerity. But they fear that if they side with us they will be punished. Their punishment would be austerity.”

Sound conflicted? While we won’t take Varoufakis’s word as the final one, the point we’re trying to make is getting 19 states to agree on anything is a fool’s errand. There exists so many different agenda points – the problem is Eurozone countries are often more divided than united.

You don’t have to look further than the money trail to understand who is incentivized to play in this conflicted system. One great winner is Germany. Two recent data points clearly demonstrate this reality:

- A new report by the Halle Institute of Economic Research shows during the debt ‘crisis’ Germany (more than any other country) benefitted by the reduction in interest rates, namely in German bund rates declining by about 300 bps, yielding interest savings of more than €100 billion (or more than 3% of GDP) during 2010-15. A significant proportion of this debt ‘crisis’ relief is attributable specifically to the Greek ‘crisis’. In short, Germany benefitted not only greatly from the flight to safety trade during the ‘crisis’ but also the debt savings helped it maintain its “fiscally conservative” budget balance.

- Germany is expected to achieve a record trade surplus of 8.1% this year (vs 7.6% in 2014), according to recent report from the German Finance Ministry. A weaker EUR and strong USD (perpetuated by the Greek ‘crisis’) has supported lower energy prices and propelled Germany’s export growth (47% of Germany’s GDP is comprised of exports!)

Stay Short the EUR/USD!

On Tuesday we recommended another short signal in the EUR/USD via the etf FXE in our Real Time Alerts.

We think there are a few guiding principles to maintain this #EuroWeakness position:

- The political crisis in the Eurozone isn’t going away. Extend & Pretend policy from the Eurocrats isn’t a viable solution to fix deep sovereign ails and the flawed structure of the single monetary union. ‘Real’ solutions and compromise to Greece’s debt ‘crisis’ cannot be reached in mere days with band-aid bailout packages. Greek bailout #3 isn’t going to work, just like #2 didn’t work.

- Draghi and Merkel remain poised and incentivized by a weak Euro. So follow the money! Draghi’s agenda is to will growth and inflation across the region. Germany is his best horse. A weak Euro is in Merkel’s best interest to support her country’s export powerhouse.

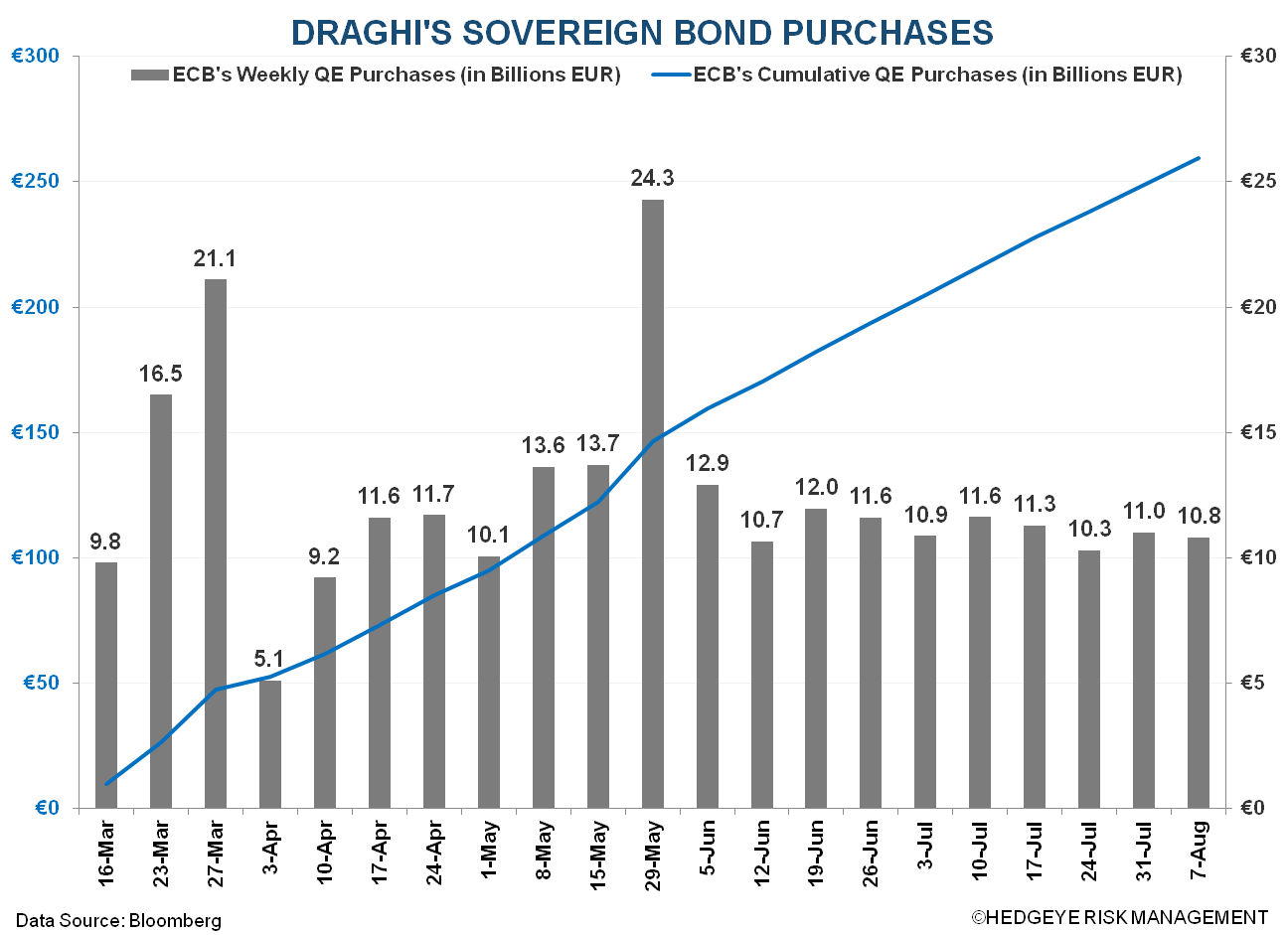

- Draghi’s “whatever it takes” continues to spell a willingness to increase his QE purchasing program (currently structured at ~ €60 billion/month – see Chart of the Day below). Look to Jackson Hole at the end of the month (Aug. 27-29) as an opportunity for Draghi to talk down the Euro. An increase in his QE target would send the Euro falling.

- Janet Yellen’s Fed is increasing looking de-facto hawkish on policy. In the last week the BOE talked down inflation (and the Pound Sterling); the BOJ remains mired in economic maladies pressuring the Yen lower; China devalued the Yuan to support its exports; and Draghi’s QE bazooka for the Eurozone remains fully loaded, with no prospect for a rate hike before the Fed. His goal of achieving a 2% inflation rate is a far out pipe dream, increasing the likelihood of more QE.

While we see growth and inflation globally continuing to slow into year end, on a relative basis the currency wars will promote winners and losers. As we originally outlined as one of our Top 3 Global Macro Themes for Q3 2015, #EuropeSlowing, we continue to like the EUR/USD as a relative loser.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.10% - 2.28%

SPX 2073 - 2115

USD 96.20 - 98.47

EUR/USD 1.08 - 1.13

Oil (WTI) 42.10 - 47.18

Gold 1075 - 1128

Keep your head down and eye on the ball,

Matthew Hedrick