SBUX reports Q3 2015 earnings after the close on Thursday, July 23, followed by a conference call at 5pm ET. The consensus is looking for revenues of $4.86 billion, up 17% and EPS of $0.41, up 21%. We see little upside to current consensus estimates.

We are adding SBUX to the SHORT bench of our Hedgeye Restaurants Best Ideas list.

SBUX obviously has significant growth potential, and has had industry leading innovation as of late. But we are growing increasingly concerned by the valuation of the stock, which trades at nearly 2 standard deviations above the five year average EV/NTM EBITDA of 12.9x. The current valuation more than adequately reflects the company’s long-term growth potential. That being said, we do have some reservations about the current growth strategy.

Some of the issues on our radar screen are:

- We are closely watching the amount of items they are adding to their menu, as they may be overcomplicating it, which if history proves right again, would decrease performance of the stores.

- Is the latest round of mobile order and pay improving throughput?

- CAP region sales and margin trends.

PRICE PERFORMANCE

SBUX shares are up 35.75% year-to-date versus up 3.29% for the S&P 500. One turn on the EV/NTM EBITDA multiple suggest 5.9% upside/downside in the name.

FINANCIALS

SAME-STORE SALES

Looking out to 3Q15, SBUX should achieve its 22nd consecutive quarter of same-store sales growth of 5% or greater, which is an impressive feat given their large store base. Imbedded in the 3Q15 performance we are looking for management commentary about the Mobile Order & Pay as well as performance of food items across all day-parts. Same-stores sales will slow sequentially in 3Q15, but traffic trends are estimated to accelerate globally.

AVERAGE CHECK

SBUX’s margins have benefited from a significantly higher average check. The check has been rising at a steady 3%-5% for the past five quarters; consensus is expecting these increases to tail off to the 2.5%-3.5% range over the next four quarters.

TRAFFIC

Traffic growth has been historically low over the last five quarters coinciding with the historically high price increases. Management is banking on innovation and Mobile Order & Pay to get traffic back up. The acceleration in traffic is critical at this valuation, especially in the Americas. Watch out below if traffic decelerates sequentially in 3Q15.

MARGIN TRENDS

RESTAURANT LEVEL MARGINS

Globally, SBUX is expected to see Restaurant Level Margins accelerating, but at a slower rate than in 3Q14. Margins expected to increase 84 basis points YoY to 28.41%, compared to a 205 basis point increase in 3Q14.

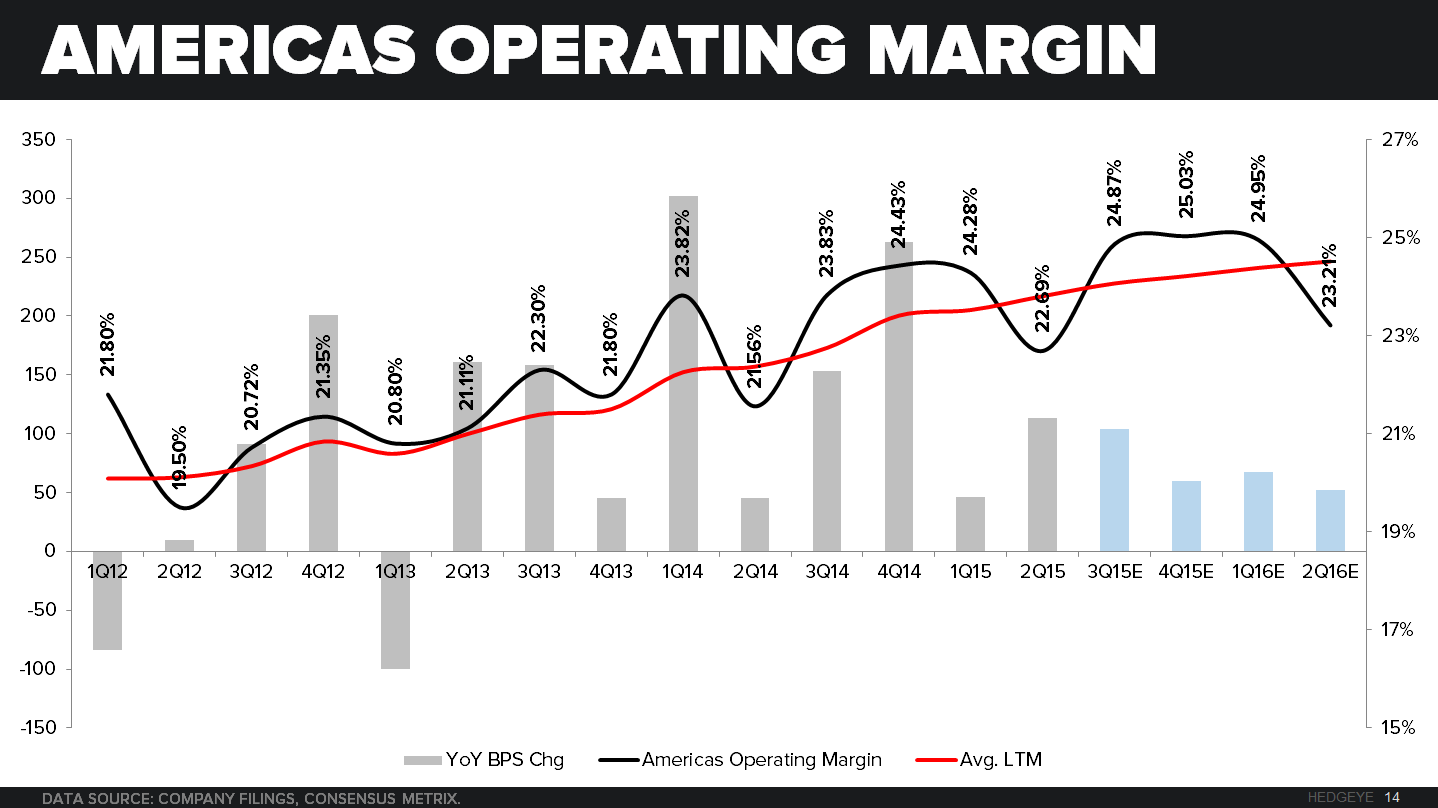

OPERATING MARGIN

Globally, SBUX should see operating margin expansion in every region except CAP. On a consolidated basis, operating margins are expected to be 19.18% in 2Q15, up 68 bps year-over year. The company should benefit from favorable coffee prices, and supply chain initiatives taking costs out of the system.

SENTIMENT AND VALUATION

EV / NTM EBITDA

Trading at 16.9x EV/NTM EBITDA the stock is not cheap, and is due for a correction. Long-term we are bullish on SBUX, but we are growing skeptical of the current valuation and product line extensions. For example, if the stock were to drop down to 15x EV/NTM EBITDA, 1 standard deviation above the five year average, it would imply a ~12% decrease to todays price. This is a scenario we believe to be likely, but with the upcoming quarter and current excitement around Mobile Order & Pay we wouldn’t want to get in ahead of the print.

POTENTIAL DOWNSIDE

Realistically we see about ~20% downside in this name if our thought process plays out. Before being fully convicted on this idea we need to hear management’s commentary during the Q3 call. Post the call we will give you our higher conviction take on the outlook for the company.

SHORT INTEREST

SBUX’s short interest is low, hovering right around 1% of the float. There is not a big bet against this company.

SELL-SIDE SENTIMENT

With 79% of the analysts having a buy rating on the stock and zero sell ratings, there is a very strong positive bias to the name. Given the financial performance of the company for the past two years, the bullish bias appears to be justified. But the future looks murky, as the over complication of the menu has the potential to spell serious trouble.

HEDGEYE RESTAURANTS IDEA LIST