While we are not quite ready to make a short call, we wanted to outline 2 headwinds to the potash industry in the coming years to keep front and center:

1. Entry from a large miner like BHP, should its Saskatchewan project get pushed through, will immediately pressure potash prices in our opinion. Uralkali and Belaruskali, who have moved to a volume over price strategy after the disbanding of Belarusian Potash Company, have mine expansions planned. These projects have been sidelined for now, but both companies plan to move forward, so even if timing is not yet specific, the likelihood that future supply will accelerate is high.

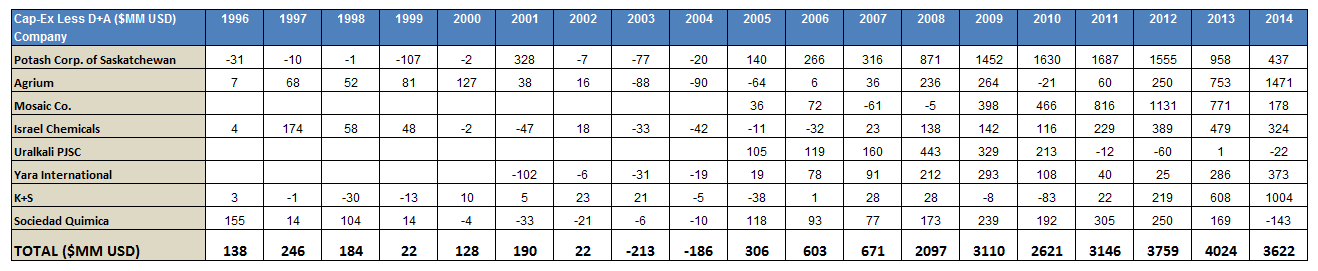

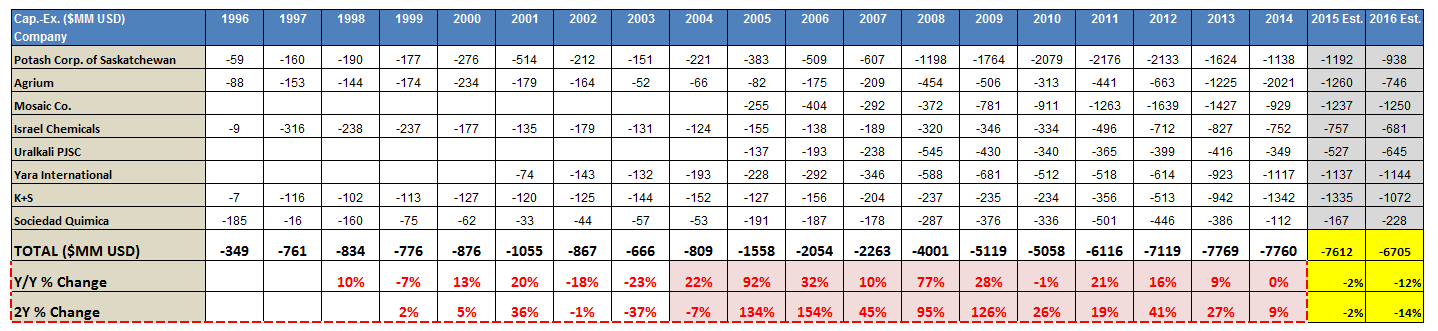

2. While capital intensive at onset, participating in the potash industry remains a high margin business even as prices have retreated, so what will Mosaic and Potash Corp. do with their cash moving forward as margins continue to compress now that they’re producing under 2/3rds capacity? More buy-backs and dividends? If they are like other commodity producers, continuing to invest in future projects is also a reasonable scenario. Whether investing in potash, nitrogen, or phosphate capacity, the fertilizer industry faces challenges moving forward. The outlook for potash just happens to look most dire.

------

- Fortunately for the largest potash producers, their business is concentrated in the hands of few players, three of which seem to operate under a nominalcartel (for now).

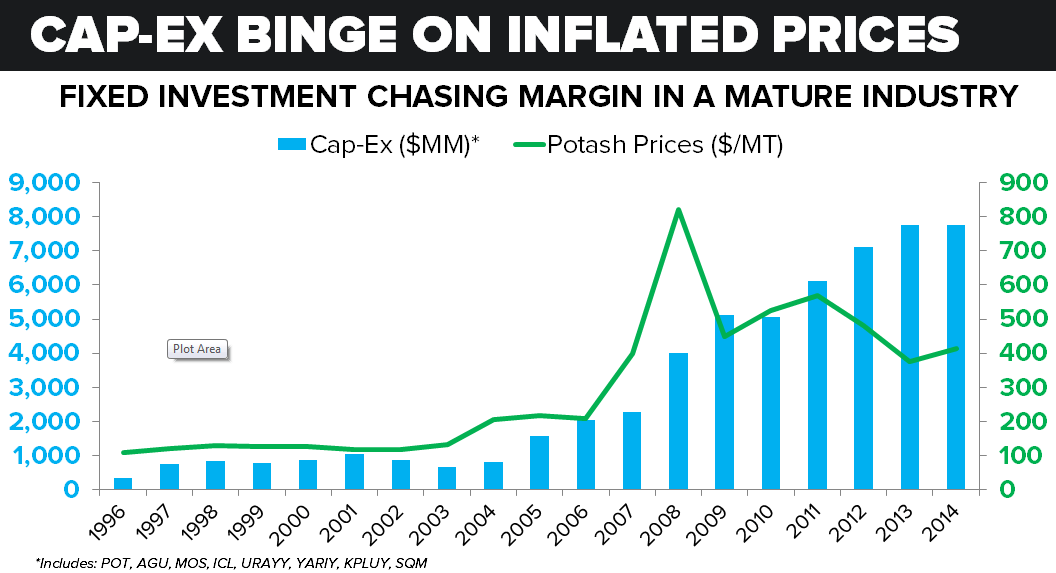

- High margins over the last several years have given the large producers cash to invest, expand, and become more efficient.

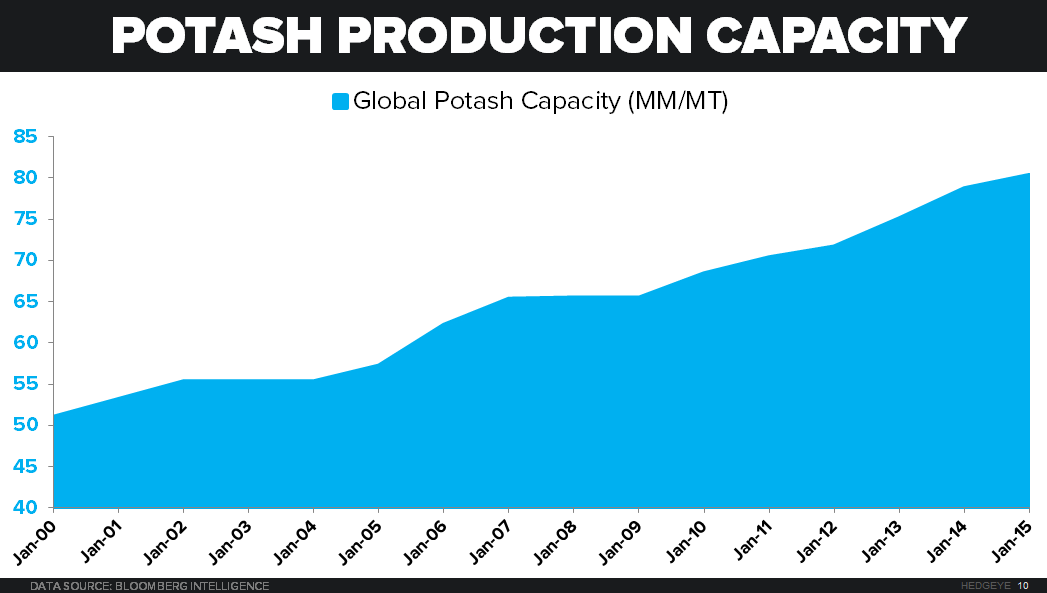

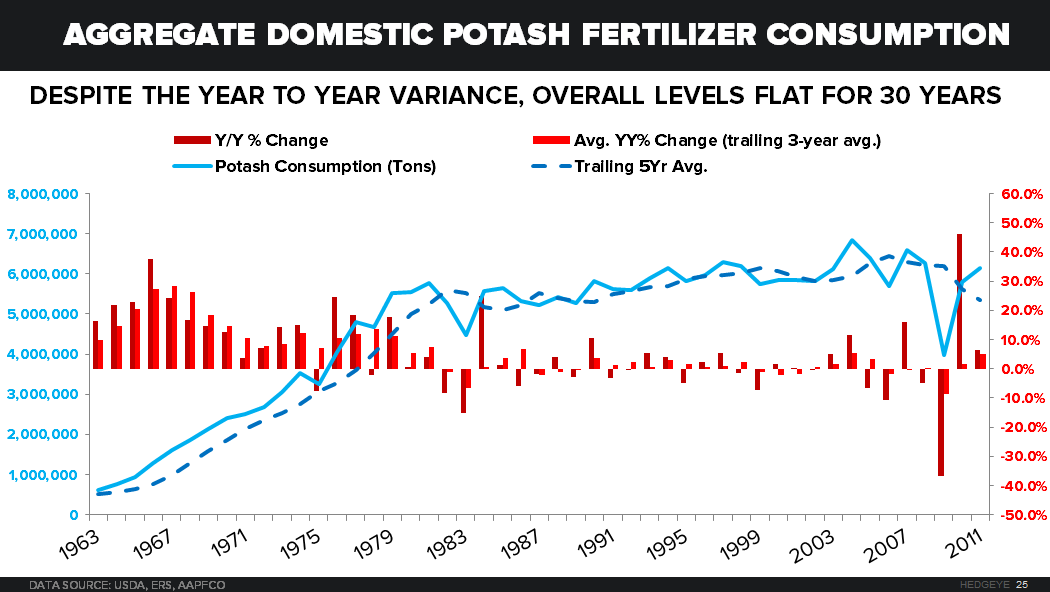

However, as outlined in the charts below, capacity additions across the globe have been excessive in the last 6-8 years relative to a long history of very meager demand growth. In fact, over thirty years aggregate demand for Potash has remained flat.

------

Unique History of the Potash Industry:

The potash side of the fertilizer industry is much less exciting than phosphate or, in particular, nitrogen , which has been a major beneficiary of localized and cheaper natural gas.

The potash industry is dominated by a select few companies. (5 companies make-up a majority of potash production). For a long-time these 5 companies belonged to 2 cartels, or “marketers and distributors” as they call it, to make up a duopoly in the global potash market.

Considering Canpotex members (POT, AGU, MOS) paid over $100 million to settle a U.S. antitrust lawsuit accusing them of concerted action to raise prices as recent as 2013, we have nothing against calling it a cartel.

Belaruskali (Belarus) and Uralkali (Russian) belonged to the Belarusian Potash Company (BPC). The three North American producers, Mosaic (MOS), Potash Corp. of Saskatchewan (POT), and Agrium (AGU) still belong to Canpotex, which is an “offshore marketing and logistics company.”

Together, these five companies control more than 2/3rds of global potash exports. BPC failed as a joint venture in 2013 and has since put pressure on the Canpotex stance as a supply-controlling organization.

Canpotex produced at around 65-70% of production capacity in 2014. AND, more capacity is in the works from both Canpotex and most importantly BHP Billiton.

From here, we can expect to see either more investment or a continued transition from fixed investment to return of capital agendas. Any incremental investment into potash expansion projects will add to the likelihood of a price crash:

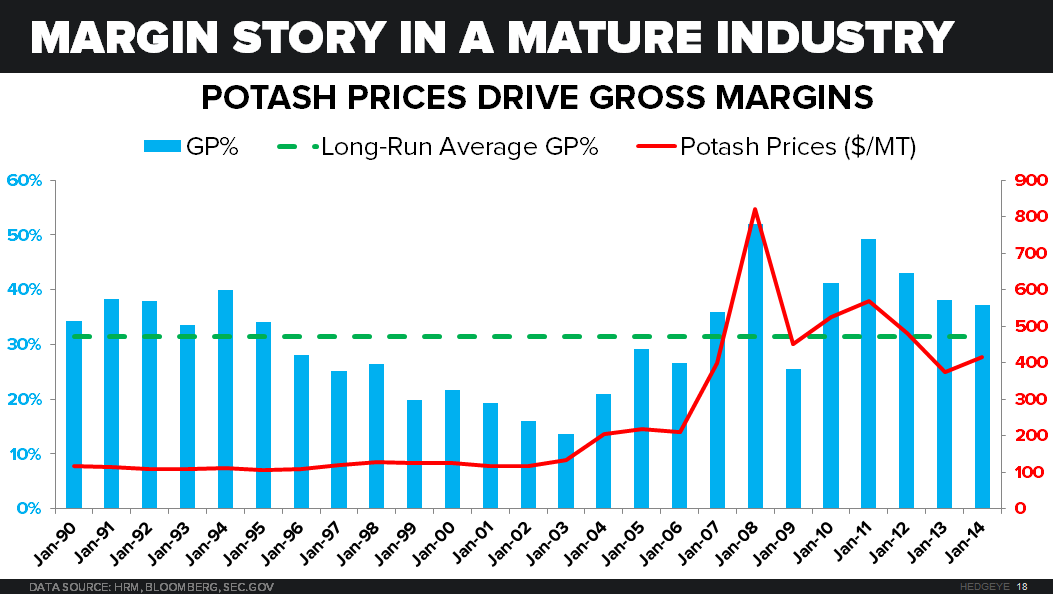

- Potash prices hovered around $100/Ton for decades until the de-regulation and low rate policy circa ~2004.

------

If BHP can follow-through with its greenfield mine project in Saskatchewan, the Canpotex position on the international market will be threatened immediately. It’s already facing pressure in the aftermath of the disbandment of BPC.

- BHP’s project is expected to bring on 7 MM/MT of production capacity which is close to 12% of current global consumption levels.

- Fortunately for Canpotex, should BHP continue with the project, initial production will be much less and not expected until 2018-2020.

BHP has consistently said that 1) they want potash to be part of their 5 pillars (already labeled “petroleum and potash”); and 2) they will not be a part of the Canpotex marketing and distribution company.

BHP failingly attempted a takeover of Potash Corp. in 2010. The bid was rejected and ultimately blocked by the Canadian government.

“The world needs new greenfield potash capacity to meet demand beyond 2020”

- BHP Investor Presentation

BHP Potash Demand Outlook

“Our large resource base can underpin the staged development of a low-cost potash business that will generate attractive investment returns.”

- BHP Investor Presentation

------

So the question becomes, if the Canpotex players continue to bring on even more capacity (like they’ve already done), yet they don’t utilize and flush it through Canpotex, won’t they shoot themselves in the foot? Then if Canpotex does disband or they are undercut in a big way, prices collapse. It seems difficult to be a swing producer when we’re this oversupplied and the threat of big entrants looms.

Is Canpotex trying to strong-arm potential entrants, much like BHP, Rio Tinto, and Vale with iron ore which unraveled in 2014? Many smaller companies have halted project plans. After-all, the cap-ex cycle is very long (6-8 years) and initial investment in a potash mine shakes out at $1,000-$2,500 MT range which is at least a 3 or 4 year payback at current prices for the best brownfield projects.

We don’t expect an answer, but a new entrant looking to become a big player in the space is probably the biggest threat to the Canpotex position.

The two former BPC members, Belaruskali and Uralkali are already shaking things up:

Uralkali signed a contract with Indian Potash Limited to deliver 800K tons of potash between May 2015 and 2016. At the end of March, Belaruskali was the first big producer to sign a contract with China. Both China and India still acquire potash via annual contracts.

The shift in the nature of the global potash trade is evidenced by the fact that independent producers are the first to sign contracts rather than an organization acting in the interests of all members.

Global trade also appears to be shaking-up the domestic potash market. Belaruskali has just started importing potash into U.S. again this year. Uralkali already jumped in front of the other players to sign the most recent China contract.

Luckily for Canpotex, the expansion projects from Belaruskali and Uralkali are on hold for now and Uralkali was forced to close a mine of significant size due to an unfortunate flood:

- The Uralkali mine that was flooded this past year will not come back online in the near future (this takes 2.3MM/MT, or ~4% of what was produced last year, off-line which is a sizable amount of global production). This mishap is a blessing for Canpotex considering the two big Eastern European producers have a volume over price strategy based on the two contracts they’ve signed with China, and now India (announced two weeks ago).

Despite the flood, Canpotex is filling the gap net of closing some smaller mines:

- Potash Corp.’s New Brunswick Mine, which only had 0.2MM/MT of capacity in 2014 is expected to ramp up (1.8MM/MT of capacity when fully completed)

- Agrium’s 1MM M/T Saskatchewan expansion is well on its way to being completed

- Mosaic has 0.6MM/MT of capacity coming online in 2015 with another 0.9MM M/T expected to be online by 2017.

It’s not as if any of the existing potash producers will disappear, but the likelihood of increased margin compression is accelerating.

Potash Corp. and Mosaic brought on more production capacity with the excess cash on their balance sheets in the heady days of the commodity bubble highs. Both used it as an opportunity to re-invest, expand, and become more efficient. We don’t question this corporate strategy. It’s logical, but the bottom line is that a supply glut has the potential to devastate prices in the future, despite efficiency gains.

With deflationary forces looming as a real risk over the intermediate to longer-term and crop prices that have retreated much further than fertilizer prices, one important question mark is the following:

Can prices collapse before planned projects are pushed-through?

Mosaic cash costs were $86/MT with brine management expenses of $17/MT for 2014. This is still 4x average potash prices globally but right around a normalized price level for many years prior to 2004.

While crop prices have retreated, fertilizer prices haven’t had nearly the fall:

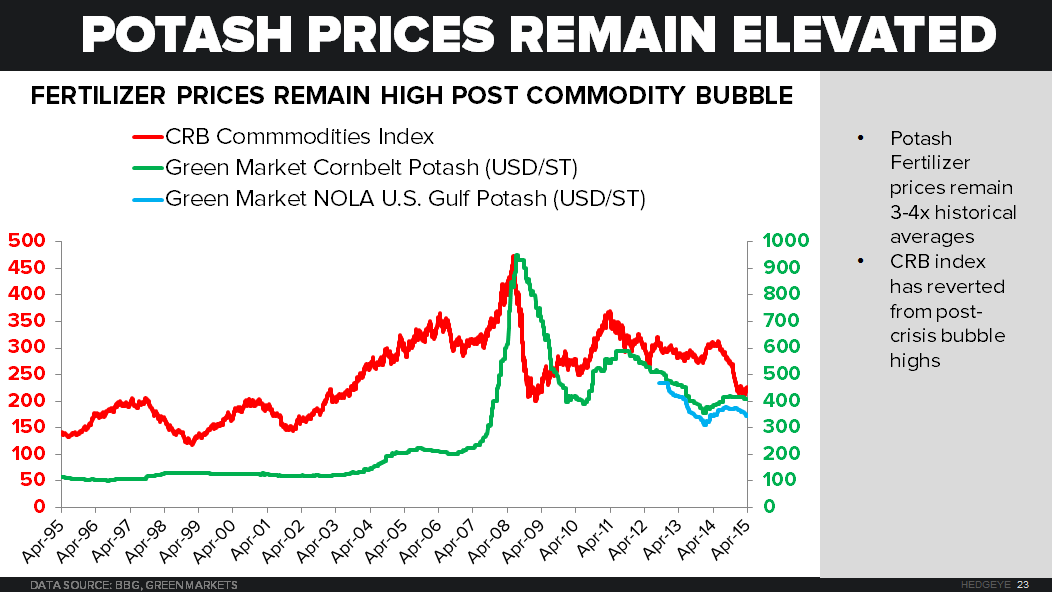

- As evidenced in the chart below, Potash prices remained at around $1/MT for many years even before 1995.

- While prices have retreated from the bubble highs, they remain 3-4x this long-term historical average.

- The CRB Commodities Index is now below its 2004 levels; Corn and wheat are less than 2x

------

We expect potash consumption to continue with its slow, steady growth trajectory.

A growth trajectory moving forward of 2-3% YY is a best case scenario. Even the large producers are expecting demand to be worse YY in 2015.

- “North America is a very competitive market. Like the second half, we may find some of the additional Agrium tonnes are not required” – Mosaic Q4 2014 earnings call

- “India needs P&K imports. Stars and Moons are aligned.” –Mosaic Q4 2014 earnings call

The emerging market demand story is old news, and begging for emerging market demand doesn’t help either. The EM argument has been at the forefront of commodity-related agriculture investment for years, and global potash demand has been underwhelming.

On the other side of the “EM Demand Story” is the fact that increase in crop pricing and crop acreage (corn is nearly 50% of the North American market for fertilizer) is largely over. Starting in 2004 ethanol expansion drove the demand for corn for a 10-year period. Ethanol expansion is now flat-lining.

------

The most important development to follow over the next few years is the ability of a large independent producer to develop more capacity. The sooner this becomes a reality, the sooner that Potash industry margins return closer to their cash cost of production.

Ben Ryan

Analyst