“No matter how much it cries or begs, NEVER feed it after midnight”

-Gremlins, 1984

According to 1980’s legend, feeding a mogwai after midnight catalyzes the transformation from cutesy, wellmeant Gizmo to mischievous, malevolent Gremlin. Hijinks, hilarity, and the creation of the first PG-13 rating ensue.

The spat of soft early March housing demand data had many wondering whether we’d already reached midnight on the current housing inflection and if the fund flows and improving sentiment feeding the multi-month run of outperformance were set to spawn a reversal in the related equity complex.

We think the hour is nearer twilight than midnight… and Gizmo has more to give as it relates to housing.

Back to the Global Macro Grind….

We reviewed our bullish thesis on Housing in a late-February Early Look – see: Dr. House-ing. The subsequent ping-pong match in housing data over the last month has, at the least, been interesting.

In a recent note to institutional clients we compared and contextualized the competing realities promulgated by the March to-date data.

Consider the following juxtaposition:

(False) Reality:

- 3/13: Mortgage Purchase Applications | Purchase demand declined -1.5% sequentially with year-over-year growth sliding back towards the zero line at +0.7%.

- 3/16: NAHB HMI | Builder Confidence declined -2pts month-over-month in March, marking the 3rd consecutive month of decline and the lowest reading since July of last year.

- 3/17: Housing Starts | New Home Starts in February dropped -17% sequentially, posting their biggest month-over-month decline since January 2007

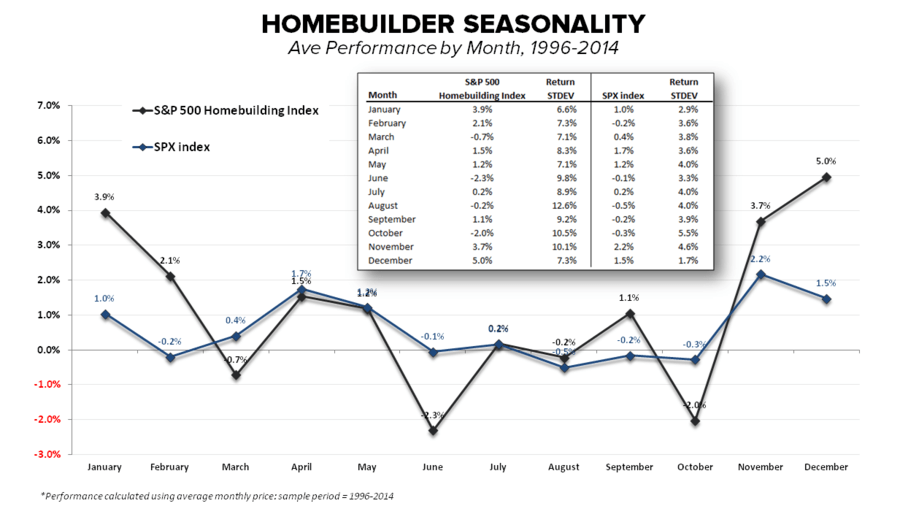

- March: Seasonality | Performance in Housing related equities shows marked seasonality. In short, the housing complex outperforms from Nov-Feb ahead of the Spring selling season and subsequently underperforms modestly in March as (presumably) some of that cumulated optimism comes off and again in mid-year as the heart of the selling season concludes (see 1st and 2nd charts below). We show the seasonal pattern that has typified the last 20 years in the Chart of the Day below.

So, certainly not the numbers accelerating recoveries and sustainable outperformance are made of.

We think the underlying reality is more sanguine with the preponderance of the weakness in the reported February data largely attributable to weather.

As it relates to builder confidence, the Current Traffic component of the index led the weakness in the composite reading, which is consistent with a severe weather related drop in the flow of active buyers. The NAHB also cited supply chain concerns, particularly in terms of labor supply. Residential construction employment saw its largest monthly increase in employment in nearly 10 years in January and employment at the industry level continues to run in the high-single digits.

There is clearly strong demand for labor in the sector, however, wage growth has yet to really accelerate according to BLS data so it remains equivocal whether rising labor demand is, in fact, driving accelerating builder cost pressure and/or labor supply shortages at the aggregate level. Further, while labor supply constraints may serve as a drag to builder confidence, presumably it is rising demand trends that are driving tighter conditions in the resi employment market. All else equal, we’d view improving demand as a net positive.

On the New Construction side, while the sharp drop in Housing Starts captured most of the headlines, we believe the real story was in the 3% gain in permits. The 57% collapse in starts in the Northeast drove the bulk of the headline decline, again consistent with unusually cold/severe weather weighing on activity.

Sure, seasonality and weather are not new phenomenon but resolving the volatility and vagaries inherent in month-to-month changes in activity in seasonal industries remains challenging despite the best efforts of evolving seasonal adjustment methodologies.

Further, staring at industry numbers from the aseptic environment of a spreadsheet has the sneaking ability to, at times, drive a wedge between expectations conceived in an analytical echo chamber and the practical realities of the underlying business. Having been in the construction industry, digging a foundation or auguring down to below the frost line to pour piers in frozen terrain is a largely quixotic pursuit.

Anyhow, we expect to see a big rebound in the next two months in housing starts as the data plays catch-up to the thaw.

Reported Reality:

- 3/19-20: Builder Earnings | Reported results for 1Q15 out of the Builders LEN and KBH had both companies beating sales and earnings estimates while reporting strong pricing and accelerating orders growth. Further, they talked down the weakness in reported Starts in February and guided to incremental margin improvement over the balance of the year with the expectations for continued, ongoing improvement in the demand environment. We’re not inclined to take management’s word for it but in this particular case, we’d agree on the intermediate term outlook.

- 3/23: Existing Home Sales | Sales of Existing Homes accelerated to +4.7% YoY, marking the fastest rate of growth in 17-months.

- 3/24: New Home Sales | New Home sales in February hit their highest level since February 2008 rising +7.8% MoM to 539K vs an upwardly revised January estimate. More notably, sales were up a remarkable +25% year-over-year and should continue to look strong from a second derivative perspective as we traverse a 5-month period of easy comparisons.

- 3/25: Purchase Applications | Purchase application saw some positive mojo in the latest week, rising +4.9% sequentially and accelerating +200bps to +2.7% on a year-over-year basis.

What’s our suggested interpretation of this Tale of Two Housing Realities?

We’d argue that much of the weakness in the reported February data was weather related and, in effect, created a mini-ball underwater dynamic. Over the next 6-8 weeks, we expect a modest backlog of deferred housing consumption in conjunction with healthy organic demand trends to manifest in accelerating improvement in reported activity.

Indeed, behind the data volatility in March, the crux of our underlying thesis remains largely unchanged. Labor market strength + credit box expansion + (very) easy compares should continue to support improving rates of change in housing demand over the intermediate term.

We’ll be hosting our 2Q Housing Themes call next Thursday, April 2nd at 11am to update our outlook for the industry and the related equity complex. Please contact if you are interested in attending.

No matter how much it [your position] cries or begs, NEVER capitulate at a manic, short-term bottom.

Our immediate-term Global Macro Risk Ranges are now

UST 10yr Yield 1.81-1.98%

SPX 2046-2084

DAX 113

VIX 14.03-16.97

EUR/USD 1.04-1.11

Oil (WTI) 42.37-52.28

To hair bands, Hungry Hippos and Volker-style policy sobriety,

Christian B. Drake

U.S. Macro Analyst