What’s the biggest risk to the market right now?

Most people would probably answer this question with one of the following: Oil, China, Russia/Ukraine, Terror/Middle East. To be sure, these are all big risks. The biggest risk I see, however, is valuation and that’s not a very Hedgeye thing to say.

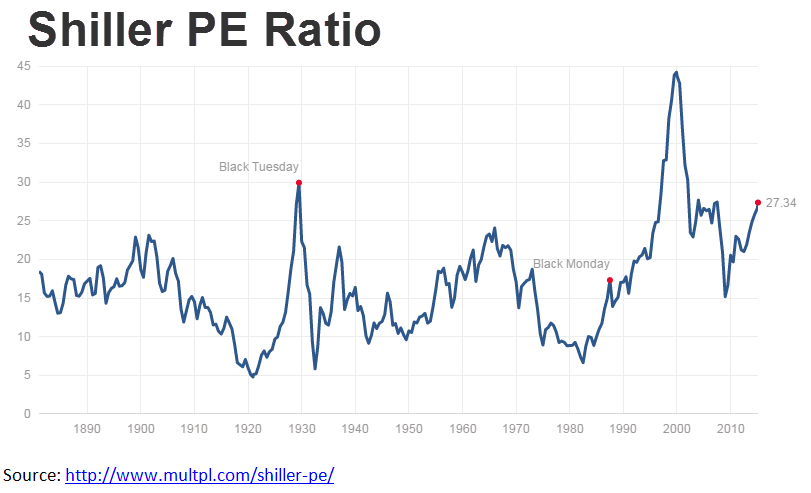

One of the more interesting weather vanes for valuation is the Shiller PE, also known as the CAPE ratio. It looks at the market’s price relative to the trailing 10 years of earnings to smooth out the normal cyclical variability of corporate earnings. Hedge Fund billionaire Cliff Asness, co-founder of AQR, and frequent author (https://www.aqr.com/cliffs-perspective) published a terrific analysis of the Shiller PE several years ago.

To summarize, he looked at the monthly Shiller PE multiple from 1926-2012 (n=1,032) and then looked at the subsequent market returns over the following decade. What he found was really interesting. He took all those observations (each monthly value over 86 years) and broke them into deciles and then looked at the subsequent 10-year return by decile of starting Shiller PE. He found that S&P 500 returns matched perfectly against those starting Shiller PE multiples.

In statistical speak, the returns are monotonic to the starting multiple’s decile. In other words, you make the most money buying the market when the Shiller PE multiple is in the bottom decile (i.e. the market is the cheapest) and vice versa. The highest valuation decile begins at a multiple of 25.1x and goes up to the highest multiple ever observed, 46.1x. Following that period, the real return for equities in the ensuing decade was just 0.5%/year. The current Shiller PE is 27.3x. The table below shows these returns by decile, while the chart below that shows the current (and historical) Shiller PE.

While 10 years is a long time, and the markets could always rally higher in the short term, the reality is that unless almost a century’s worth of market history is suddenly irrelevant (the mother of all “It’s Different This Time” arguments), the outlook for buy-and-hold returns over the next decade is terrible, which is why we at Hedgeye constantly emphasize the need to be keep moving out there.