The second half of 2009’s back to school season appears to be picking up with industry sales positive and incrementally better than the previous week. As a reminder, we don’t look at the absolute growth in these SportscanINFO numbers given our view that the sample is somewhat flawed. But the fact is that it is a consistently flawed sample, and as such the directional changes have proven to be quite relevant. The bottom line here is that the industry’s total dollars are picking up steam. Is it coming at the expense of price point? Yes, somewhat. But the ASP trends are nowhere close to what I’d consider panic levels.

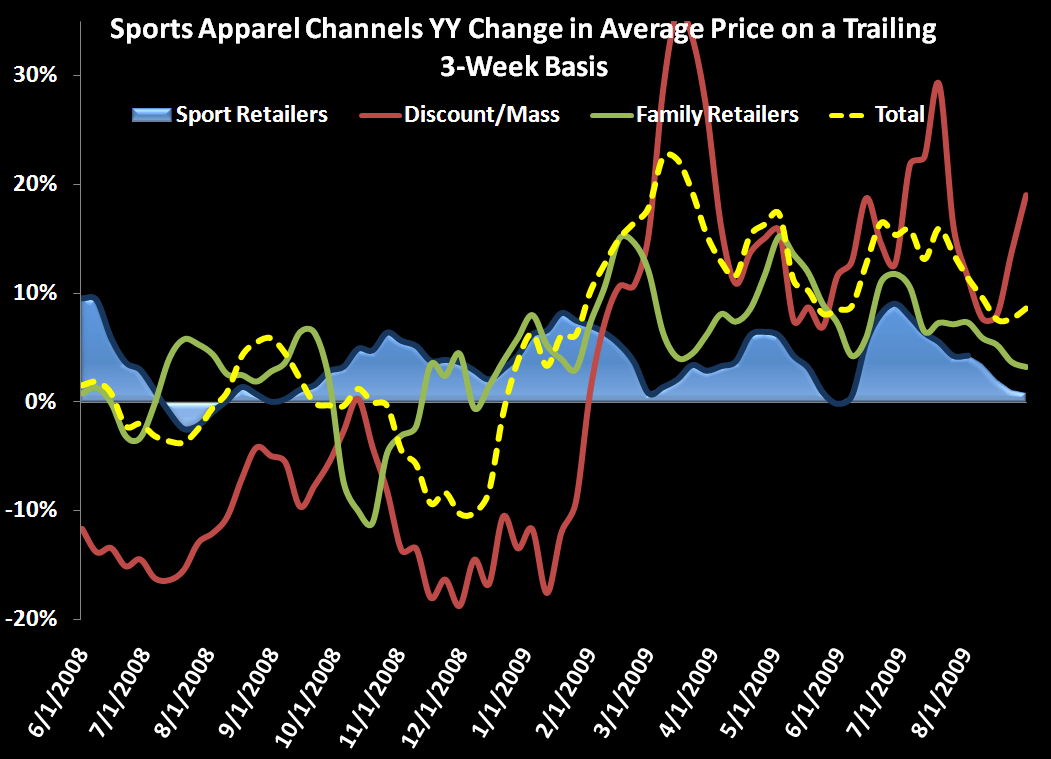

Total industry sales grew by 3% driven by growth in Sport Retailers and Family Retailers while the Discount/Mass Retailers channel continued to underperform. All channels sequentially improved on sales while ASP growth remained positive across the board. Major deltas between this week and last week are the sales jumps of 5% by Sport Retailers and Family Retailers and the 15% jump in ASPs by Discount/Mass Retailers.

Full Line Sporting Goods, Mid-Tier Department Stores, and Family Footwear stores were positive for the week with Athletic/Urban Specialty stores sequentially improving but remaining negative. All geographic regions of the US were positive with the exception of New England, the Middle Atlantic, and the East North Central who were all down less than 5% which was an improvement.