FIVE-FECTA: REVOLVING CREDIT GROWTH ACCELERATES FURTHER IN JULY AS THE BREAKOUT IN CONSUMER CREDIT HITS 5-MONTHS

Consumer Revolving Credit rose at a 7.3% annualized rate in july, the 2nd largest increase in 6.5 years behind the 13.2% rise reported for April.

Inclusive of July, this marks the 5th consecutive month of positive MoM loan growth – the longest such streak since April of 2008.

The monthly revolving consumer credit data continues to accord with the broader cross-category trends in the weekly Fed H.8 release where the slope of growth across total loans, C&I, CRE, and residential real estate all remain positive.

SO, WHERE’S THE SPENDING?

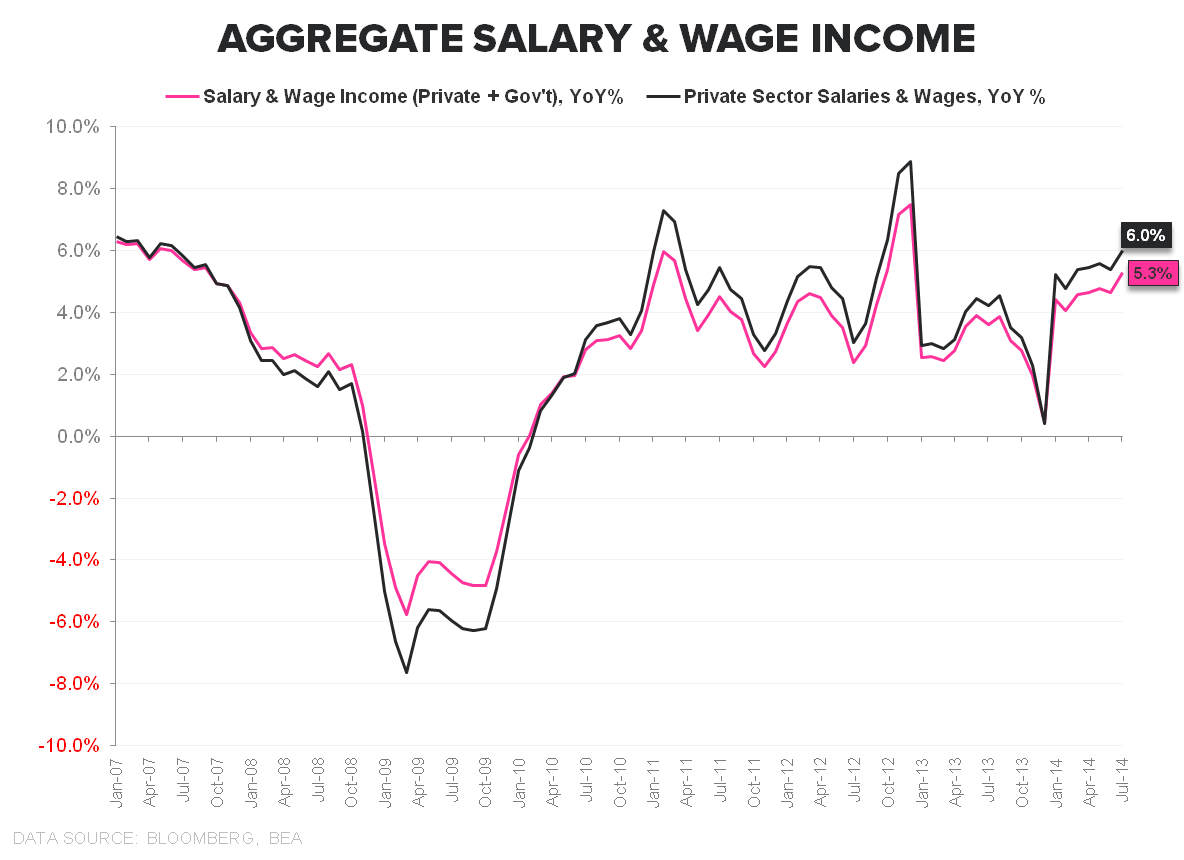

Aggregate personal and disposable income growth is currently accelerating alongside an emergent breakout in salary and wage income growth.

Indeed, aggregate private sector salary and wages grew +6% in July, the fastest rate of growth in over 3 years excluding the peri-fiscal cliff period (although wage income growth will likely slow in august given flat growth in hourly earnings and a modest deceleration in growth in the employment base).

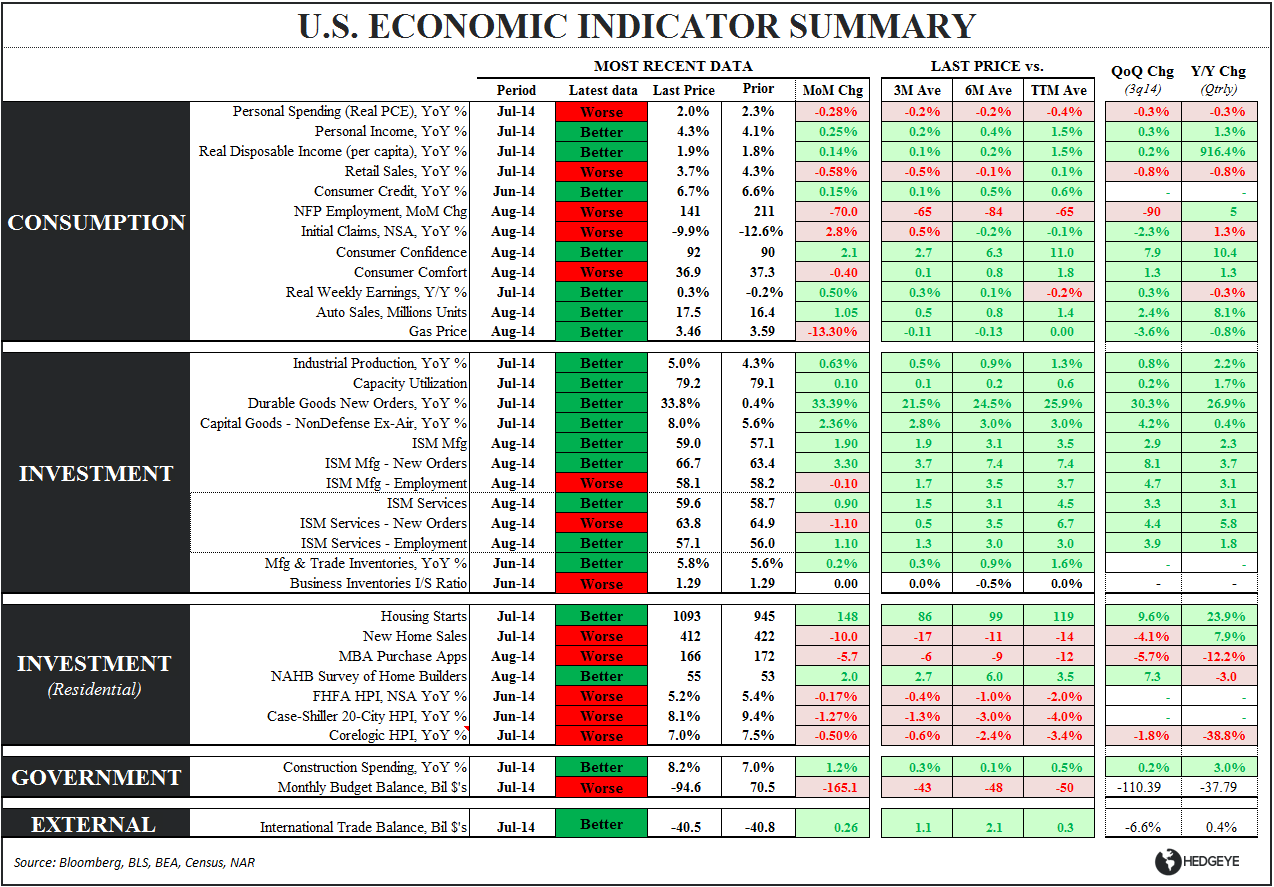

However, while capacity for consumption is rising, actual consumption is not. Real consumer spending declined -0.2% MoM in July and decelerated on both a 1Y and 2Y basis as the savings rate hit an 18-month high at 5.7%.

The collective motivation underpinning the concomitant acceleration in both savings and revolving credit isn’t completely clear – it may be some combination of liquidity preference and income distributional effects, but we don’t have a clean explanation (yet).

Irrespective of the somewhat incongruous income-credit-saving dynamics, the reality of a modern, consumption economy, is that it's total spending that matters and accelerating credit growth + accelerating income growth is certainly supportive of consumption growth.

Whether the conflation of positive labor and credit market trends, the fledgling breakout in the dollar and the fledgling breakdown in commodity inflation can drive a sustainable, late-cycle acceleration in domestic consumerism in the face of negative real wage growth, a slowdown in housing, a discrete EU/Japan/ROW growth deceleration, and a nascent proclivity for saving remains to be seen, however.

We continue to like defensive yield and late-cycle exposure vs. consumer/housing/early-cycle leverage.

Christian B. Drake

@HedgeyeUSA