How did MAR’s long range projections from 2010 and 2012 fare?

CALL TO ACTION:

Taking a step back to evaluate MAR’s 2010 "Plans for Ambitious Growth" covering 2011, 2012 and 2013, we found that actual results generally disappointed vs. Marriott’s goals. In addition, on June 19, 2012, MAR senior management hosted an investor meeting in Beijing, China during which management rolled forward their growth plan through 2014. Similar to the 2010 plan, the 2012 growth plan is trending toward the low end of the company’s forecast range. Certainly, with yesterday's investor meeting, MAR was once again ambitious in its communicated plan. While we are positive on the hotel sector over this period, we would err to the low end of MAR’s forward guidance range given the track record. Further, with MAR’s recent stock outperformance and relatively and historically high valuation, we prefer the stocks of the other branded hotel companies with HOT being our favorite near term idea.

BACKGROUND:

On October 27, 2010, Marriott gathered investors and analysts for an investor conference titled "Marriott Outlines Plans for Ambitious Growth". Yesterday, simultaneous to MAR stock reaching a new 52-week high, MAR senior management hosted a full-day analyst meeting in Washington DC, titled "Marriott International Charts Future Success". Similar to 2010, MAR once again laid out some aggressive financial targets, the high end of which may be difficult to achieve. We note, Marriott’s historical forecasts were predicated on forward three year looks; however, yesterday's forecast and outlook included 2014 as well as 2015, 2016 and 2017. This change in interval timing is important because 2014 includes the Protea acquisition as well as line item trends that are stronger or higher in 2014 than 2015, 2016 and 2017.

The table below compares the 2010 forecasted metrics versus actual and then yesterday's new projections. Here are some observations:

- Actual 2011-2013 compounded RevPAR was 6.25%, only modestly above the low end 5% assumption, but below the midpoint of 7%

- Year-end 2013 EPS was $1.99 versus the implied $2.10-2.15 guidance based on actual RevPAR growth of 6.25%

- Conversely as well as surprisingly, MAR forecasted total fees of $1.57 billion (low-end based on 5% RevPAR growth) yet 2013 total fees were $1.511 billion – less than the low end forecast even with higher than 5% RevPAR growth.

- Base management fees in 2013 of $621 million were significantly below MAR’s midpoint projection of $765 million.

- Franchise fees were definitely the bright spot with actual of $634 million, slightly above the high-end 2010 projected range of $560-$625 million.

- Incentive management fees of $256 million during 2013 were below MAR’s low end guidance of $285 million.

- Total gross room openings from 2011-2013 were 83,643 versus a projection of 80,000 to 90,000 rooms

- Total capital returned to shareholders from 2011 to 2013 via share repurchases and dividends were also below the midpoint totaling $3.925 billion versus MAR’s forecast of $3.3B - $5.3B.

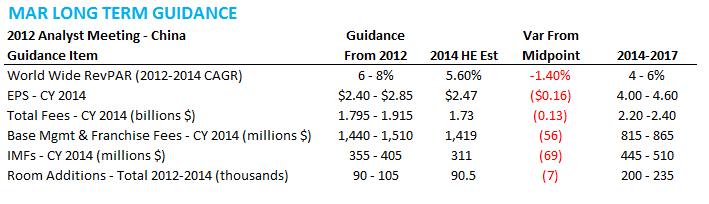

On June 19, 2012, MAR called investors to Beijing, China for an informative update on the Company’s Asia Pacific growth strategy as well as providing an update and roll forward on key metrics and growth strategy. The 2012 plan focused on the calendar years 2012, 2013 and 2014. Similar to the 2010 Growth Outlook, results are trending below the mid-point of Marriott’s forward look.

The table below compares the 2012 forecasted metrics versus Hedgeye’s forecast for cumulative and year-end 2014 results. Here are some observations:

- 2012-2014 compounded RevPAR growth is developing toward 5.6%, below the low end 6% assumption and 140 bps below the midpoint of 7%

- Year-end 2014 Hedgeye EPS is $2.47 versus current company guidance of $2.40 - $2.51 and the implied $2.30-2.35 guidance based on estimated RevPAR growth of 5.6%

- MAR forecasted total fees of $1.795 billion (low-end based on 6% RevPAR growth) and 2014 total fees are estimated to be $1.73 billion – less than the low end forecast.

- Base management and franchise fees of $1.44 billion in 2014 (based on 6% RevPAR) are above the Hedgeye estimate of approximately $1.42 billion and significantly below MAR’s midpoint projection of $1.47 billion.

- Incentive management fees of $355-405 million during 20134 were forecasted but Hedgeye currently forecasts $311 million of IMFs in 2014, $44 million below MAR’s low end guidance of $355 million.

- Total gross room openings from 2012-2014 were estimated at 90,000 to 105,000 and Hedgeye forecasts 90,500 gross additions.

CONCLUSION:

While we believe the sell-side will "reaffirm" their optimistic ratings on MAR following today's meeting, we are less impressed based on historical results. Don't get us wrong, we are favorably inclined on the lodging sector and its strong underlying fundamentals as well as the likelihood for positive near-term revisions. However, we prefer some of the less expensive branded hotel stocks with more near-term catalysts such as HOT, H, and HLT.