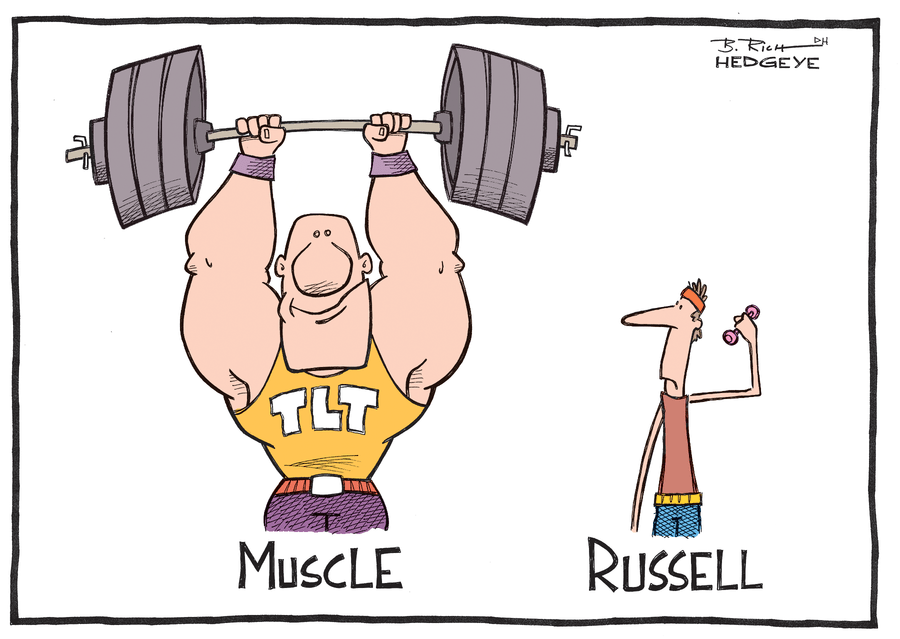

Takeaway: The 2014 Macro Score: Long Bond $TLT +14% vs Russell 2000 -2%

LAST CALL: OUR BEST DEAL EXPIRES SOON!

SAVE UP TO 66% OFF

MACRO & STOCK-PICKING ESSENTIALS

Takeaway: The 2014 Macro Score: Long Bond $TLT +14% vs Russell 2000 -2%

By joining our email marketing list you agree to receive marketing emails from Hedgeye. You may unsubscribe at any time by clicking the unsubscribe link in one of the emails.