We applaud the lower than consensus Q3 guidance but maintaining full year guidance risks a Q4 guide down.

CALL TO ACTION

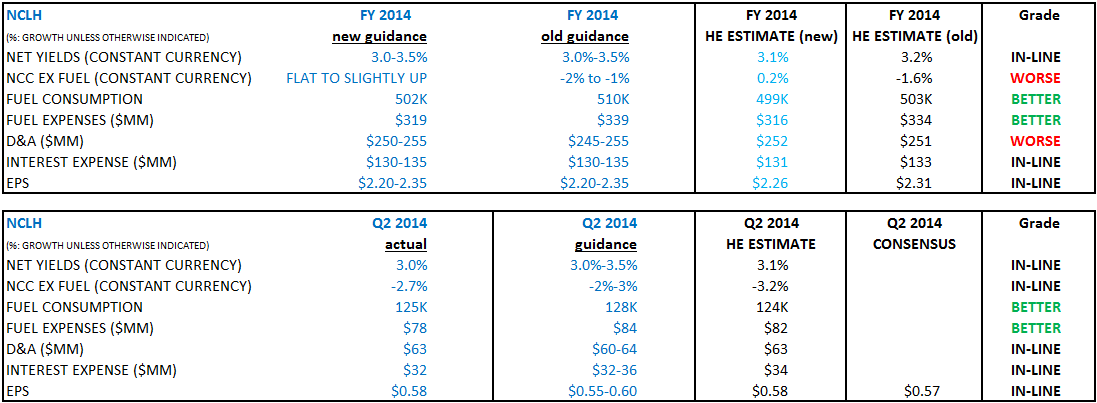

NCLH reported 2Q numbers that met our estimate and company guidance despite lower revenues. The NCL brand began discounting in the Caribbean in late January, rankling investors’ nerves but not the sell side. Approximately 80% of sell-side analysts have maintained buy/outperform ratings (pending Genting stock sale?) even as the stock has fallen 10% this year. Revenues were indeed disappointing and NCLH did provide lower than expected Q3 guidance. With unchanged full year guidance, we’ve got to ask: where are they going to pull earnings from to make the higher implied Q4 guidance?

The stock looks to open down but we may see some more pin action today as a somber management team fields questions on the Caribbean and upcoming cost initiatives. At the end of the day, investors may be tired of waiting for the inflection point. We find it hard to disagree.

QUESTIONS WE HAVE FOR MANAGEMENT

- What drove Q2 fuel price per metric ton down by $38 vs management guidance? Lower fuel costs offset the revenue miss.

- Implied Q4 yield guidance looks aggressive. What is driving that outlook – better pricing or load?

- Commissions/transportation costs as a % of ticket revenue has fallen in four out of the last five quarters and offset lower gross ticket yield. Is this an indication of being less reliant on the agent community, renegotiation of tour/shore pricing, or something else? How sustainable is it?

- Why is cost guidance ex fuel going higher when there are a number of cost cutting initiatives are underway? NEXT program?

EARNINGS RELEASE

We were surprised by the lower than expected 3Q yield guidance and very skeptical of the 4Q implied guidance of ~4% yield growth. The Hedgeye proprietary cruise pricing survey suggests more difficult pricing conditions in Q4. While Caribbean comps are easier in 4Q than 2Q and 3Q, more competition (e.g. Quantum) is on the way and NCL will have to deal with that in the New York market - quickly. In our opinion, NCL has a better shot of exceeding yield expectations in Q3 than in Q4 or early 2015.

We are not seeing any signs of a less promotional Caribbean pricing environment. Could the low pricing in the Caribbean becoming a secular trend? Perhaps. Oversupply concerns have been understated and the initial hot booking demand cooled somewhat in the Caribbean this year.

Q2

Net yields met the low end of the company’s guidance at 3.0% as more cost reductions offset lower gross revenues.

- Net ticket yields rose 2.7% as lower commission/transportation/other costs offset the 1stdecline in gross ticket yield since 3Q 2012.

- Commission/transportation/other costs only accounted for 15% of ticket revenues, the lowest since IPO inception (an interesting trend…)

- Gross ticket yield was likely hampered by a double digit decline in Caribbean yields despite the addition of Getaway and Breakaway

- Ticket margins rose to 79%, a new high

- Net onboard and other yield grew 4.8%

- Gross onboard/other yields climbed 1.9%

- Onboard/other expenses fell 2.1% points YoY to 24.3% of onboard/other revenues

- Fuel expense was $6 million less than management’s guidance.

YIELD GUIDANCE

Q3: 2.25%-2.75% yield growth guidance came in below our estimate of +3.7% yield growth (Street: +3.5%). Guidance was surprisingly conservative given the strength in Europe and its largest quarterly contribution at 32% of total capacity in 3Q. We believe management is estimating Caribbean yields to be a couple % points lower than our projection of mid-single digit yield declines and a less stellar outlook for the Hawaii market.

Q4: Guidance suggests 3.8% yield growth to reach the midpoint of FY yield range. That’s an aggressive forecast. To achieve that yield target, one would need: slightly lower European yields than that seen in Q3, flat yields in the Caribbean, slightly lower yields in Hawaii, and modest growth in the Canada/England/other segment. Can the Caribbean hold its ground for the next couple of months for Q4 sailings even if Breakaway premiums shrink? NCL seems to think so.