SUMMARY

This is the summary version of our current thoughts on P. In short, we have a cautious view of P's long-term runway. We believe listener hours for its core ad-supported product will see pressure as the runway for new user growth isn't long enough to compensate for its churning members. We understand there are additional opportunities from both car & local advertising, but we're not sure it will be enough to produce the 30% growth that consensus is expecting for both 2015 & 2016. We are NOT short yet, given upside we see to 2Q14 revenues and 2014 guidance, but we will be looking for an entry point on the short side as we move closer to 2015. Until then, we'll continue to round out our analysis, and provide updates along the way.

NEAR-TERM OUTLOOK (2014)

-

2Q14 REVENUES LOOKING STRONG: P’s monthly disclosures are showing a significant increase in listener hours (despite a user growth slowdown) as the company comps the mobile listening cap that ran from 3/13 to 8/13. Factor in a considerable increase in ad load (see below), and a 50% increase in sell-through rates on its audio ad inventory, and we can see 10% upside to 2Q14 metrics.

- 3Q14/2014 GUIDANCE UPSIDE?: We're expecting P's prospects to fade as we move through 2014 as it comps out of both its mobile listener cap and increased ad load in August. We're expecting a 2014 guidance raise, largely because of a 2Q14 beat. And even though we see some upside to 3Q14 currently, management may play it safe on the 3Q guidance release. In short, if P raises guidance, it may be uninspiring.

LONG-TERM OUTLOOK (2015 - )

-

ACTIVE USERS TO DECLINE?: The question is when, but we expect low single-digit user growth to pressure investor sentiment before that occurs. P has glaring retention issues. Over the last +3 years (1Q11-1Q14), P has added at least 160M registered accounts, yet only gained 46M active accounts. In turn, P’s churn (114M) has outpaced retention during this period. But the bigger issue is its shrinking runway; with +250M registered accounts, and +160M added since 1Q11, the headroom for new account growth may not be large enough to offset its churning members for much longer.

- TUG OF WAR: P will need to continue increasing ad load to drive the 30% growth the street is expecting for both 2015 & 2016. But rising ad load could exacerbate its retention issues. P’s audio and video ads are intrusive; more ads could limit existing listener hours per user and/or incite even greater churn, especially in the wake of growing competitive threats. If listener hours decline, one of two events occurs: P’s ad inventory declines alongside declining listener hours, or that increased inventory gets pushed on to its more active users, which will test their loyalty as well.

NEAR-TERM CHART SERIES & ANALYSIS

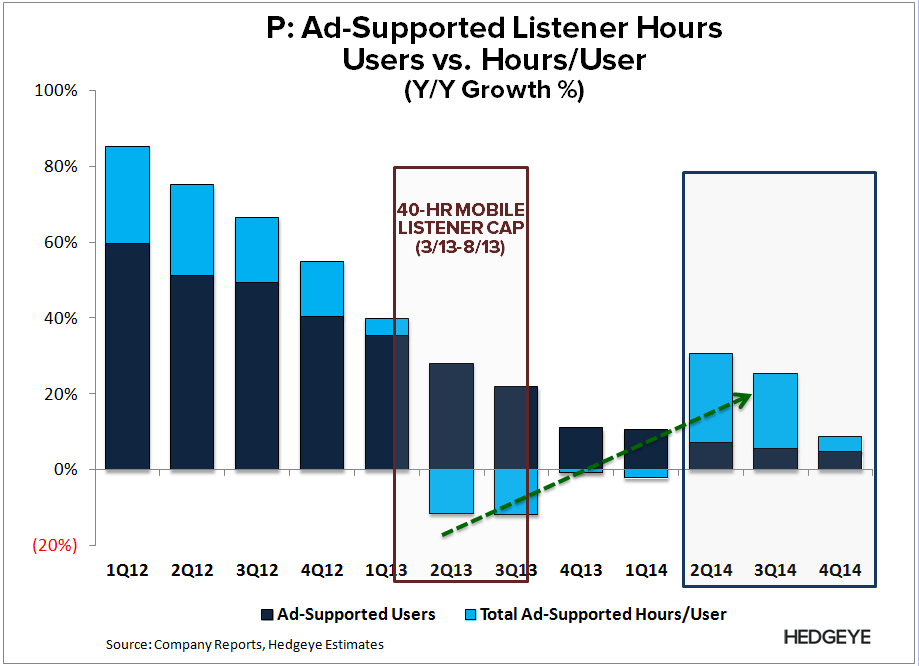

Comping the Mobile Listener Cap in 2Q14

P initiated a mobile listening cap for its free ad-supported service from 3/13-8/13. During this period, we estimate that ad-supported listener hour growth decelerated sharply, while per-user hours declined. P's 2Q14 monthly disclosures suggest that trend appears to be reversing; total hours are accelerating despite slowing active user growth, as per-user hours are comping against the first full quarter of the mobile-listening cap.

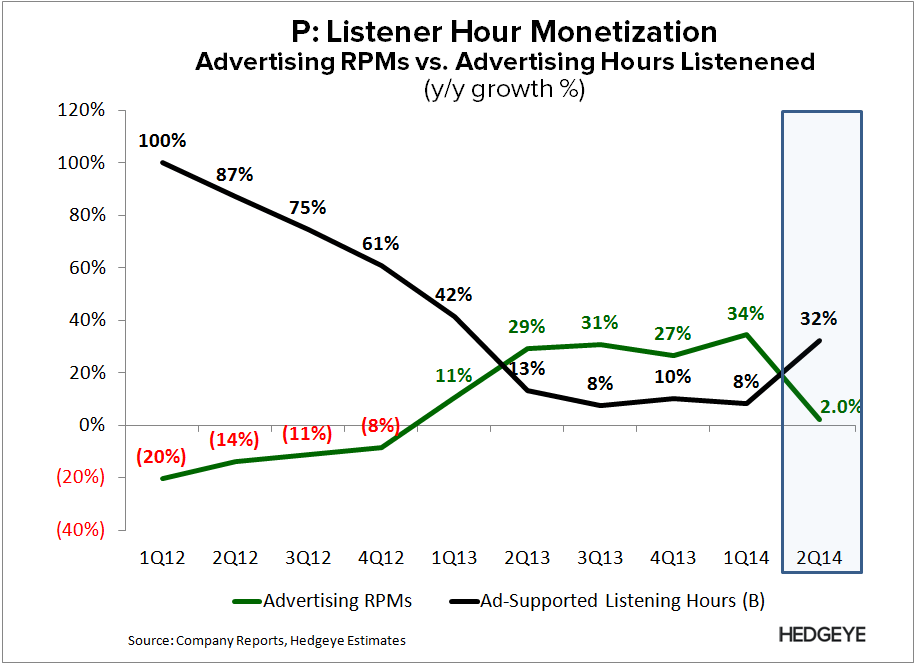

Ad RPMs Growth to Decelerate, But Increasing Ad Load Should Help

There is an inverse relationship between growth in RPMs (revenue per thousand minutes) and listener hours, suggesting a 2Q14 surge in listening hours may come with declining RPMs. However, P increased its max ad load/hr in August 2013 (4 to 6), but more importantly, altered its ad feed (from 1 ad/15 min to 2 consecutive ads/20 min). In short, some users are seeing considerable increases in ad loads, in some cases 100% higher. Management also stated that the sell-through rates on audio ads are up 50% y/y, so even though we expect a sharp deceleration in Ad RPMs, we still expect an increase y/y from the increased ad load.

Upside in 2Q14 Will Wane Therafter

Surging growth in listener hours, and a likely y/y increase in RPMs, suggest meaningful upside to 2Q14. We're expecting advertising revenue will accelerate in 2Q14, leading to total revenues of $235M (up 49% y/y) vs. consensus of $219 (up 38% y/y). But after 2Q14, P will lose the y/y comp benefit of both its increased ad feed (August) and the listener cap (September). Further, subscription revenue growth could see incremental pressure since P is no longer providing annual contracts (March 2014), which has created a mild uproar among existing subscribers (696 comments link). Note its subscription price increase currently only applies to new members.

LONG-TERM CHART SERIES & ANALYSIS

Churn Appears to be a Recurring Theme

We can’t calculate P’s churn rate explicitly because the company stopped providing metrics for actual registered users in 2Q11. Before that period, the math was pretty clear; following that period, we have to take a cumulative view of what has happened over the past +3 years, which we detail in the chart below. P’s churn (114M) has outpaced its retention (46M) during this period. Some users have multiple accounts, which could be partly to blame, but likely not enough to explain such high levels of churn (unless each of those active users averaged ~3.5 individual accounts). Churn has gone under the wire since new account growth (registrations) has outpaced its churn, but that cannot continue indefinitely.

Less Room for New Account Growth = Churn To Become More Evident

P has over 250M registered accounts, but there is definitely some double-counting of users (multiple accounts) in its account metrics since there are only 245M people in the US ages 10-69, which is likely its target market. But remember that over 160M of its +250M accounts registered in 1Q11-1Q14. So the better question is how many duplicate accounts were created during this period? The impetus to having multiple accounts is likely tied to P's listener caps, which only existed for 15 of the 39 months in this period., So while multiple accounts are definitely a driver, we question if its a material percentage; particularly in the more recent periods. But we still have work to do here, since answering this question is the key to breaking down P's realistic headroom, and whether the runway for new account growth can continue to compensate for churn. Stay tuned.

Rising Ad Load Will Exasperate Retention/Listener Issues

We estimate that ad-supported hours per/user declined marginally y/y on relatively clean comps in 4Q13 and 1Q14 (despite the easier comp from 1Q13 from one-month of the cap). We suspect P's adjusted ad feed (2 consecutive ads every 20 min from 1 ad every 15 min prior) may be partly responsible. For example, we estimate the average ad-supported user listens ~40 minutes daily. If turn, P has actually doubled the ad load for those users (4 ads in 40 minutes today vs. 2 ads prior). This isn't as much of an issue now, but casts doubts as to whether P can stick to its stated strategy of gradually increasing ad load...without pressuring listener hours at the same time, which appears to be the case over the last 2 quarters. Its important to remember that P's ads are intrusive, and the Pandora user as isn't captive as it once was given growing competition for listener hours from emerging threats.

CONCLUSION

Once again, this is the summary version of our current thoughts on P. As always, we will be publishing additional notes with incremental data and analysis in the coming weeks & months. In the interim, let us know if you have questions, or would like to discuss in more detail.

Hesham Shaaban, CFA

@HedgeyeInternet