Our Hedgeye Housing Compendium table (below) aspires to present the state of the housing market in a visually-friendly format that takes about 30 seconds to consume.

Today's Focus: Existing Home Sales

The National Association of Realtors (NAR) released its monthly Existing Home Sales report for April earlier this morning. Most of the data is largely useless because it's telling you what you already knew, but on a lag. This is because it mirrors the Pending Home Sales index, which comes out a month ahead.

Remember, the Pending Home Sales index reflects contract signings while the Existing Home Sales report reflects contract closings. There's typically a 1-2 month lag between signings and closings. That being said, there is one extremely valuable piece of data in the Existing Home Sales report that most market participants tend not to focus on, and that's the inventory number. It's the only measure of total housing stock for sale published by any source and it's not a stale number. It's reflecting the number of properties (existing) for sale at the end of the period.

Context

Taking a step back, our main call here is that we're bearish on the outlook for the rate of change in home prices in 2H14 and 1H15.

Why?

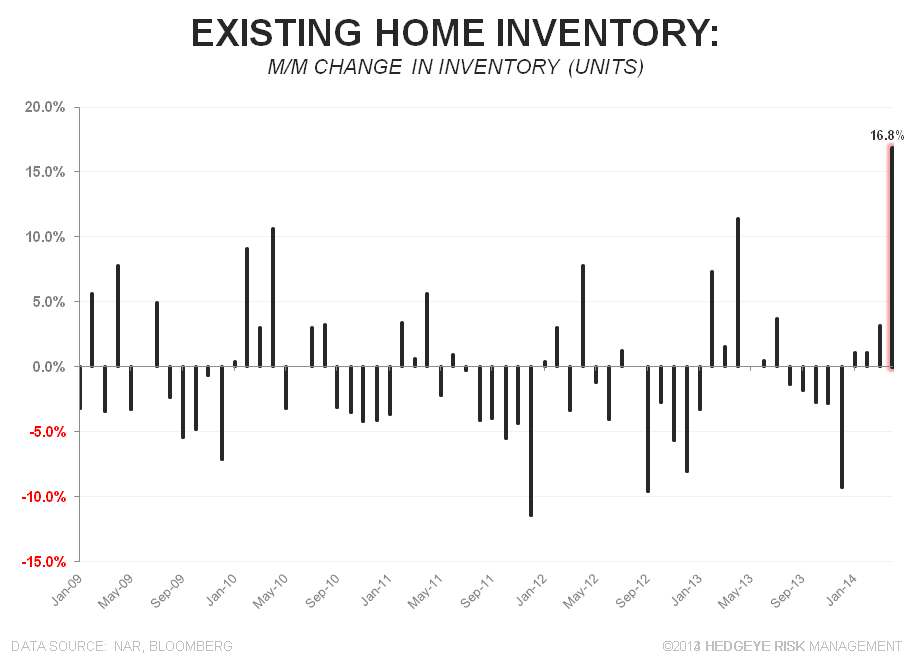

Principally, it's because demand has been in decline since mid-2013 and price changes tend to follow demand on a 12-18 month lag. The mitigating force, however, is that supply of homes for sale has remained quite low by historical standards. This morning's data is interesting principally in that there was a very large move up in inventory.

To be fair, unlike existing home sales, which are seasonally adjusted, inventory numbers are not. So one would expect to see a big month-over-month upturn in inventory in April, but the size of this year's increase is significantly larger than what we've seen in Aprils past. This increase lessens the mitigating effect of the tight inventory on prices, adding incrementally to our conviction in our call for the rate of home price appreciation to slow markedly.

Here's a summary look at the numbers:

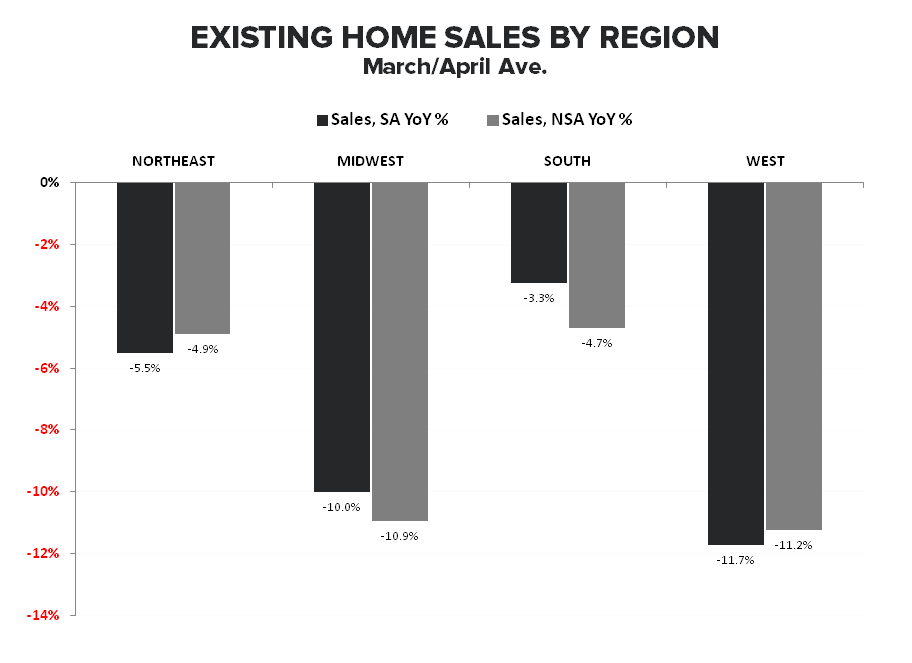

Demand: Better month over month but still weak, soft across all geographies and not reflecting any significant deferred demand from 1Q weather distortion.

- Total sales increased 1.3% MoM….but remain down -6.8% YoY (vs. -7.5% YoY in March)

- YoY Sales growth remained negative across all geographies with the decline accelerating in the Northeast (-6.3% YoY vs. -4.8% in March) and South (-3.5% YoY vs. -3.0% in March)

Supply: Large jump in Supply. Biggest MoM increase in inventory on a units basis ever (back to 1999) at +16.8% MoM

- Inventory (MM Units) = 2.3…up from 2.0 in March = +16.84% MoM & +6.5% YoY

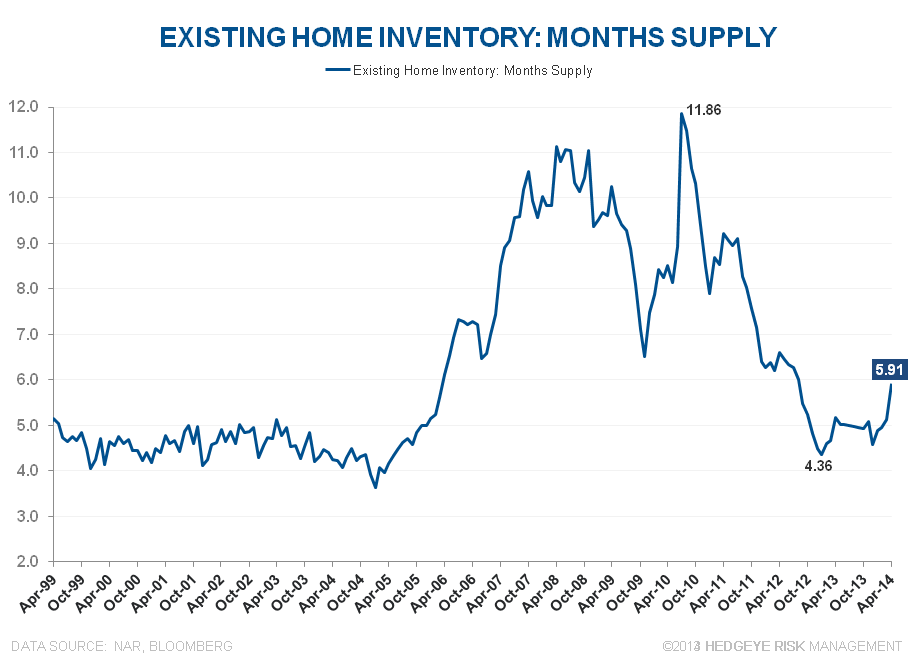

- Inventory (Months Supply) = 5.91…up from 5.12 in March = +15.3% MoM and +14.3% YoY

Other: All cash sales remain elevated and 1st time home buyers continue to run less than 30% as QM impacts, lower affordability, low inventory (among others) all continue to drag on young buyer demand – If you view housing as a ladder then inability for 1st time buyers to purchase = lower turnover & lower total transaction activity (although rising supply may help low end volumes)

- Distressed = 15% of April Sales down from 18% last April

- 1st time buyers = 29% of buyers in April – down from 30% in March and flat with 29% from April last year

- All-cash sales = 32% of transactions vs. 33% in March and 32% april last year

About Existing Home Sales:

The National Association of Realtors’ Existing Home Sales index measures the number of closed resales of homes, townhomes, condominiums, and co-ops. Existing home sales do not take into account the sale of newly constructed homes. Existing home sales account for 85-95% of all home sales (new home sales account for the remainder). Therefore, increases in existing home sales tend to signify increasing consumer confidence in the market. Additionally, Existing Home Sales is a lagging series, as it measures the closing of homes that were pending home sales between 1 and 2 months earlier.

Frequency:

The NAR’s Existing Home Sales index is published between the 20th and the 22nd of each month. The index covers data from the prior month.

Joshua Steiner, CFA

Christian B. Drake