THESIS SUMMARY

-

Absurd Attrition Rate; Will Only Get Worse: YELP’s “repeat rate” is misleading. YELP is losing almost 20% of its customers on a quarterly basis, potentially in excess of 90% annually. Recent customer User Interface enhancements & macroeconomic headwinds are likely to exasperate the issue.

- TAM is a Fraction of What’s Advertised: Estimates vary for YELP’s total addressable US market, ranging from 23M-27M….In reality, its closer to 170K.

- 2014 Consensus Lofty/2015 Unattainable: Consensus revenues imply an acceleration in new account growth on a per-market basis and/or improving attrition rates through 2015, we're expecting the opposite. Details below.

- $30 Stock?: YELP trades at a premium to FB & LNKD on a 2014 P/S basis given lofty consensus growth expectations. Once growth expectations collapse, the stock will too.

ABSURD ATTRITION RATE

YELP provides a quarterly metric called its customer repeat rate, which it defines as the percentage of its current customers that has advertised with YELP in the LTM. That rate has hovered in the low 70% range since the company went public, with the remaining 30% being new customers. What isn’t disclosed is how many of its customers that it is losing on a quarterly basis, but we have broken this down.

The math is simple. Multiplying YELP’s active customers by its repeat rate will yield its recurring customers. If that number is lower than its ending customer count from the prior quarter (i.e. the number of customer that have advertised in the LTM), then it lost customers.

On a quarterly basis, YELP loses almost 20% of its customers. However, management has stated that most of its customer contracts have 12-month terms (vs. 3 & 6-month contacts with higher CPMs). If that is the case, YELP’s attrition rate is considerably higher, potentially in excess of 90% annually depending on the contract mix. Put another way, the active customer base that YELP reported in 4Q13 is comprised almost entirely of new accounts signed in 2013: YELP added a total of 63K accounts in 2013; it ended 4Q13 with 67K in total.

WHY IS ATTRITION SO HIGH?

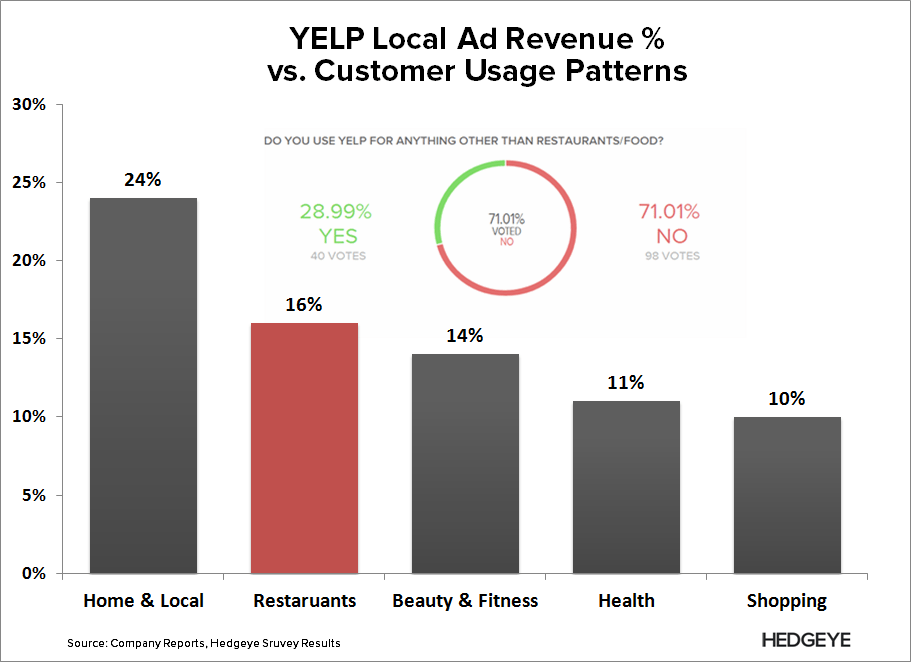

The main reason is a mismatch between the sources of YELP’s advertising revenue and how people use its website. Revenues are relatively distributed across 6 categories, but our proprietary survey suggests visitor use Yelp almost exclusively for restaurants.

In turn what happens is that restaurants do not see a material uptick in traffic to their pages (because they are already getting the traffic), while the remaining categories don’t see a material lift in traffic-related revenues unless they charge a high enough ASP for their services to justify the advertising cost for limited traffic (e.g. Interior Designer).

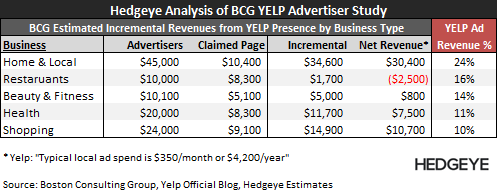

To illustrate, we delved into the BCG survey that YELP highlights on its official blog, which suggests that companies that advertise on YELP see increasing revenues ($23K on average vs. businesses without a YELP presence). However, the incremental benefit varies by business type.

What’s more important is the incremental revenue an advertising business receives relative to those that have claimed their YELP page, but do not advertise. We have broken down the BCG survey in the table below to highlight this concept.

What’s interesting about the survey results is that it reinforces the our view that restaurants do not see enough of a yield to justify the ad spend; and once again, this analysis is based on the BCG survey that YELP highlights on its official blog. While most of the remaining categories appear to offer a meaningful ROI, we suspect these results are not typical of most businesses on YELP. If they are, why is YELP’s attrition rate so high?

WHY ATTRITION WILL GET WORSE

There are two main drivers that we expect will lead to accelerating attrition: 1) YELP may be shooting itself in the foot with its new Revenue Estimator Tool, 2) Macroeconomic Headwinds will make it tougher for businesses to absorb advertising expenses.

- YELP’s Revenue Estimator Tool: Late in 1Q13 (3/25/13), YELP introduced a new tool for its businesses that estimates YELP-derived revenues based on the amount of estimated traffic YELP drives to the business. While a nice feature, we suspect the tool may incite greater attrition since it will likely highlight the limited advertising ROI for these businesses. The other risk is that the tool could grossly overestimate Yelp’s benefits to these businesses, which would reduce confidence in the disclosed revenue benefits (e.g. YELP calculates estimated business revenue on total leads, even though these leads are not mutually exclusive events). As contracts come up for renewal, we suspect the revenue tool will only exasperate YELP’s attrition issue since it will make limited advertising ROI more tangible to its customers.

- Macroeconomic headwinds: The setup is getting worse. Retail sales growth appear to be dropping sharply in 1Q14, and more importantly, input costs (i.e. commodities) are rising considerably YTD. Collectively, small business margins will see increased pressure given reduced economies of scale; particularly for restaurants. Some businesses may be forced to curb costs where they can; others will be taking a harder look at their P/L. In either case, it will be that much harder for YELP to curb attrition; especially if its Revenue Estimator Tool highlights limited advertiser ROI.

YELP's Customer Dashboard Example

TAM IS A FRACTION OF WHAT’S ADVERTISED

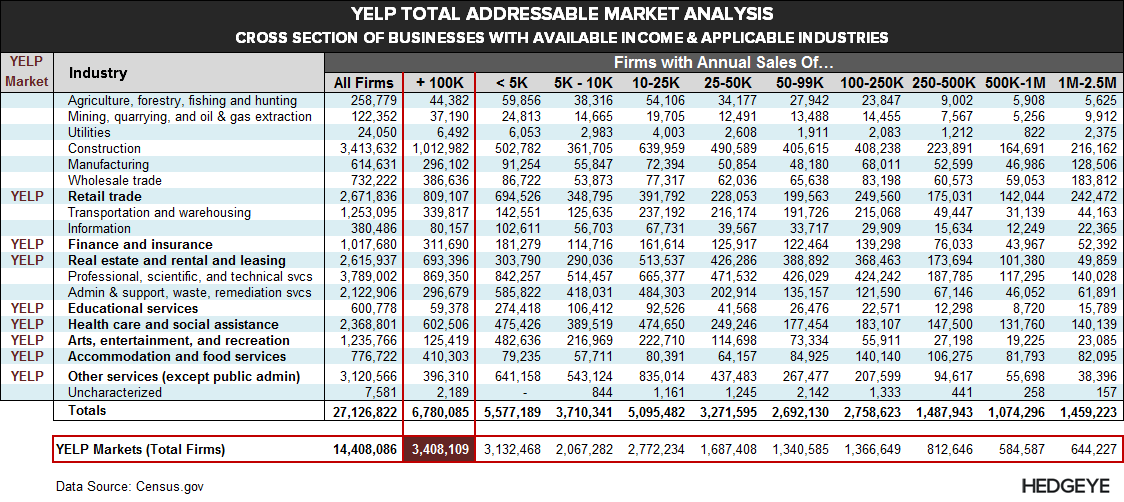

Consensus may argue that YELP’s total addressable market (TAM) is substantial, with a pool of 27M businesses in the US (22M Nonemployers, 7M Employers). But after digging deeper into census data, YELP's TAM is considerably smaller. Two things to consider

- Can’t Afford: 75% of US businesses make under 100K annually (YELP’s annual ARPU is $4.2K)

- Wrong Audience: ~50% are B2B, largely outside the scope of YELP’s core audience

After netting out B2B-focused businesses with less than 100K in annual revenues, we estimate the total addressable US market is closer to 3.4M. However, we doubt YELP approaches anything close to that.

YELP currently has 67K paying businesses, which is only ~4.5% penetration of its 1.5M claimed business pages as of 1Q14. In fact, YELP’s advertiser base has never exceeded 5.0% penetration of its claimed pages since the company has been public. That alone suggests the demand just hasn’t been there. So unless that changes, YELP’s realistic addressable market is 170K businesses (5% of the total 3.4M opportunity).

That may sound crazy relative to the consensus narrative, but YP, which owns yellowpages.com, only has 575K active customers, and it is the largest local internet ad platform in the US.

Based on its 67K current advertiser accounts, YELP has penetrated roughly 40% of realistic addressable market.

2014 CONSENSUS LOFTY/2015 UNATTAINABLE

The driving forces behind YELP’s revenues are new account growth and attrition. In 2013, YELP averaged 31% y/y growth in new accounts on a per-market basis, and an average attrition rate of 18.7%. As you can see in the table below, YELP will need to improve on one, if not, both of these metrics to hit 2014 estimates. We expect deterioration on both fronts for the reason we laid out above.

However, it’s in 2015 when we expect YELP’s fundamentals to take a material turn for the worse. It's attrition risk will increase alongside a waning opportunity for new account growth given increasing penetration. Consensus is assuming revenues of $512M in 2015; a moderate deceleration to 43% revenue growth on a base of $358M in 2014 revenues. In order to achieve consensus 2015 estimates, YELP will need to produce both accelerating new account growth on a per-market basis and improving customer retention vs. 2014. We’re expecting revenues of $444M, 30% increase on our 2014 estimate of $342M, and we're being conservative. In the table below, you can see the assumptions driving our model

$30 STOCK?

YELP’s trades at ~14x and 10x 2014 & 2015 revenues, respectively. That multiple is justified only if you believe consensus growth expectations. Below we relate the forward P/S multiples of the group to consensus revenue growth rates to illustrate this point

However, we do not believe YELP has the growth profile that the consensus assumes. In 2015, we believe it can grow 30% (vs. consensus 43%). On a growth-adjusted P/S basis, YELP should trade closer to LNKD (7.5x), if not lower, based on a more comparable growth profile.

That said, YELP shouldn’t be trading anywhere above a 2015 P/S multiple of 7x; a more appropriate multiple would be in the 5x-6x range given our estimate for 30% growth in 2015, which would translate to $30-$36 stock based on our 2015 growth estimates. We expect the stock to trade in this range once the street realizes YELP is a 20-30% grower, rather than a 40-50% grower.

ADDITIONAL DETAIL

The above analysis focuses on YELP’s core market: the US local ad market, which is the substantial majority of its revenues (~80%). We plan to prove additional detail during our YELP Short Best Ideas Call (details to be announced shortly), as well as discuss the rest of its business model

In the interim, let us know if you have any questions, or would like to discuss in more detail

Hesham Shaaban, CFA

@HedgeyeInternet