The Big Picture

Rapid advances and declines have largely muted the overall commodities basket to-date in 2014, with the CRB Foodstuffs Index up 40 bps YoY. However, the index ticked up 310 bps last week and a continuation of this trend would be bearish for all restaurant operators.

Commodity prices up YoY:

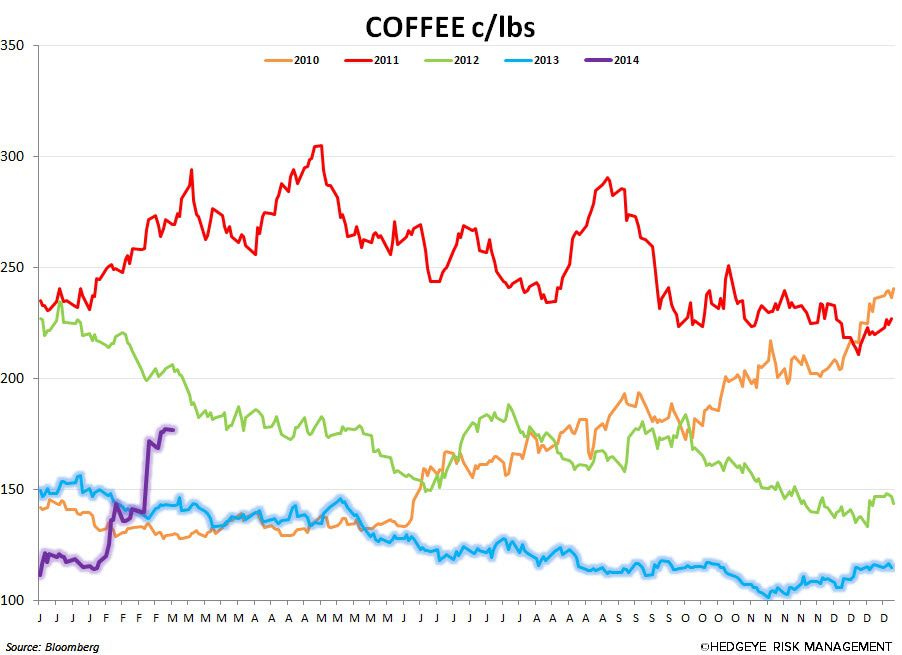

- Coffee

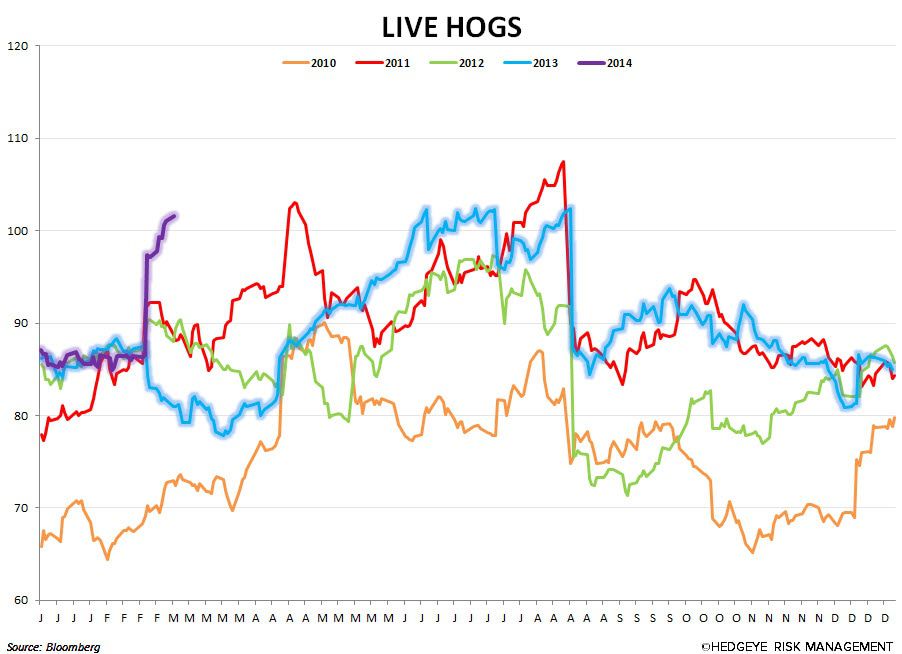

- Lean Hogs

- Cheese Block

- Live Cattle

- Soybean

- Milk

- Natural Gas

Commodity prices down YoY:

- Sugar

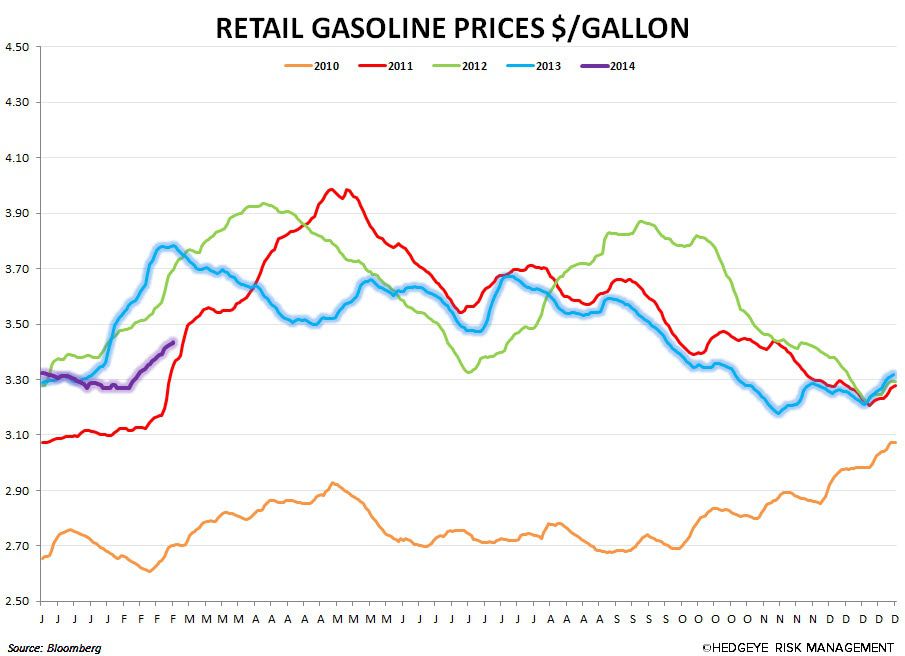

- Gasoline at the Pump

- Corn

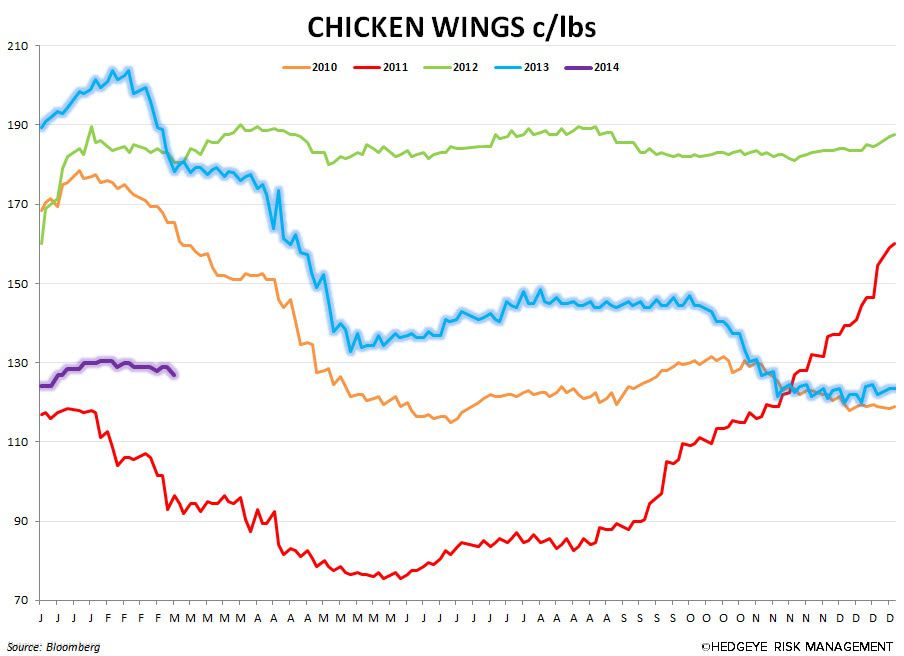

- Chicken Wings

- Wheat

- Rough Rice

- Chicken Whole Breast

Notable trends:

Coffee prices continue their rapid rise, ticking up 5.5% over the past week. They are now up 12.8% YoY. First, it was torrential rains in Brazil’s coffee belt hurting the crop. More recently, however, the Brazil crop has been hampered by a prolonged period of dry weather. Analysts estimate the global market could be facing its first shortage in over four years. Not only is this fundamentally bearish for coffee retailers, but it has also negatively affected sentiment within the space (see SBUX for example). Takeaway – bearish for SBUX, DNKN, GMCR, KKD.

Pork and Beef prices continue to rip higher, up 5.1% and 4.0% over the past week. They are now up 25.9% and 17.5% YoY, respectively. Pork prices have come under pressure lately due to the spread of the porcine epidemic diarrhea virus, also known as PEDv, which results in a very high mortality rate for piglets. Beef prices have been surging as cow herd sizes continue to decline. Restaurant operators don’t expect much relief anytime soon, as it takes well over two years for a cattle herd to hit the market. Takeaway – bearish for TXRH, RUTH, RRGB, BLMN, CMG, MCD, JACK, SONC, WEN and other operators with notable exposure.

Cheese Block and Milk prices are up 38.3% and 36.5% YoY. While cheese block prices ticked up 4.2% over the past week, milk held flat. CME cheese block prices are currently close to a decade high. We will continue to monitor these trends closely. Takeaway – bearish for CAKE, DPZ, PZZA and others.

Corn and Wheat prices continue to be the saving grace for many operators, effectively offsetting pressure from other commodity costs. Both commodities are down 20.6% and 21.3% YoY, respectively. Takeaway – bullish for everyone.

Chicken and Chicken Wing prices have also led several operators to offer new items and LTO’s as they seek to more prominently feature chicken on their menus. Both commodities are down 9.7% and 29.4% YoY, respectively, and should help the margins of operators with notable exposure to this group. Takeaway – bullish for PLKI, BWLD, YUM and others.

Gasoline at the Pump is down 8.8% YoY, but ticked up 1.1% over the past week. Takeaway – while the YoY decline is a positive for the industry, last week’s move gives us reason to be cautious on our outlook. We will continue to monitor this trend, as any sustained increase or decrease in gas prices could have a significant impact on the direction of discretionary spending and the consumer’s willingness to eat out.

Howard Penney

Managing Director