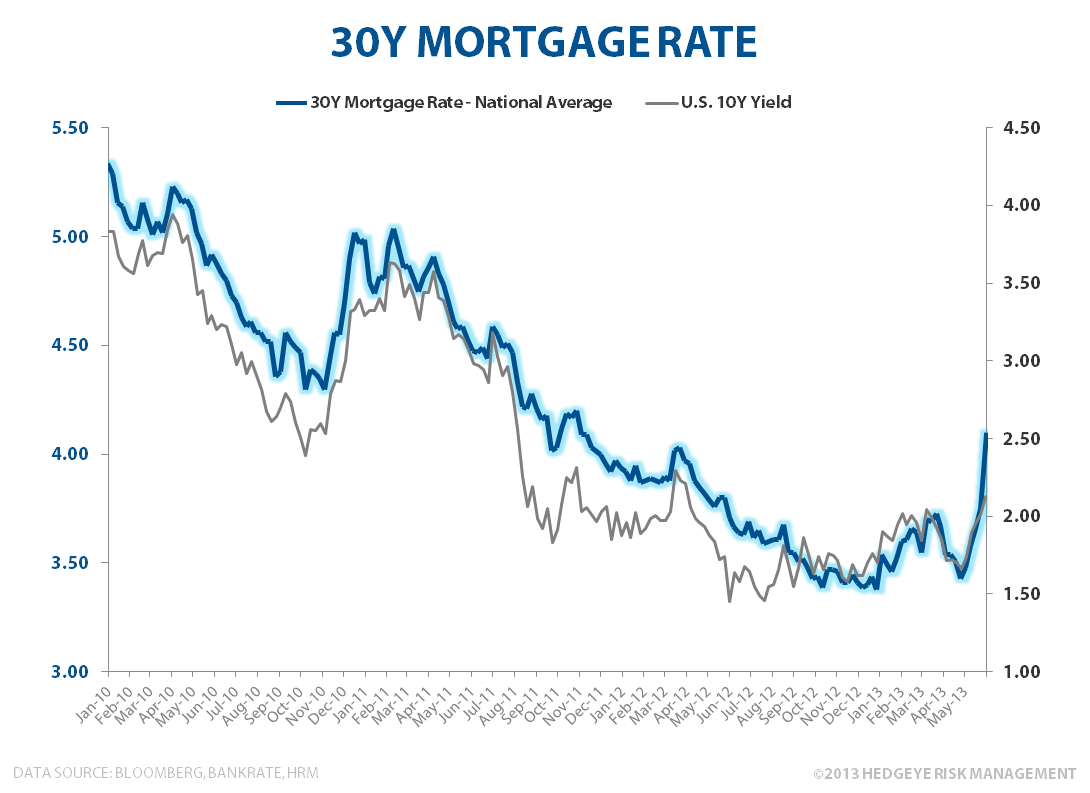

Last week saw a significant back up in 30Y Residential Mortgage Rates as the national average rose 35 basis points W/W to 4.10% from 3.75% the week prior. From the near historical low of 3.40% reached back on May 1st, we’ve seen an expedited 70 bps backup in rates over the last month.

The move in rates holds a few notable impacts for housing. First, the increase in mortgage rates should have a (unsurprisingly) significant, negative impact on refinancing activity – something that has already manifest in the MBA mortgage application data with refi activity down 12.3% in the last week and 23% over the last month. This contrasts with Purchase Activity, which was actually up 2.6% in the latest week and down just 2.3% over the last month.

While we believe the positive Giffen cycle in housing (see Here for fuller discussion) should continue to predominate with demand chasing higher prices in a reflexive fashion, higher interest rates have a direct, negative impact on housing affordability.

Previously, we have shown (Here, slide 49) that under standard median income and DTI assumptions for a 30Y Freddie Mac Mortgage loan, a 10bps change in rates equates to an approximate 1.0% change in affordability. A continued rise in interest rates would serve as a headwind to a further acceleration in home values, particularly as HPI growth comparison’s get steeper.

While we would view the breakout in treasury yields alongside the material sector level performance divergences (XLF +6.1%, XLU -9.0% in May) as pro-growth signals, with the housing recovery a key tenet underpinning our domestic growth outlook, we’ll certainly be monitoring rate impacts on affordability closely here.

Christian B. Drake

Senior Analyst