Darden Restaurants reports 3QFY12 EPS on Friday. We are not expecting management to reverse course on its bearish view of FY13 and FY14 and, as we outlined during a conference call with clients on 3/14, we believe the stock is in a “win-win” scenario. Here is a copy of our recent presentation materials and the accompanying audio link, titled, “DRI: The Unthinkable Long Case”.

While we would not object to a shakeup of the management team or the emergence of an activist investor to bring about a change in strategy, there have been some positive signs that the company is considering fresh approaches to how it is allocating capital.

Two marginal positives in a sea of negatives over the past couple of months include:

- During the Analyst Meeting, Dave George, the new President of Olive Garden, acknowledged the deteriorated value proposition of the concept, as well as the need to slow unit expansion and focus more narrowly on execution

- Red Lobster is testing a new “pay at the counter” version of its concept. Customers place their orders at a counter and a server delivers the food when it’s ready. It’s difficult to know if this concept will prove effective in attracting customers but we take the company thinking differently about its strategy, and capital allocation, as a marginal positive. For too long, as we detailed in our Black Book, “DRI: The Unthinkable Short Case”, in July, the company had been slow to react to decelerating trends and made poor capital allocation decisions. With seafood commodity prices, particularly Lobster, being so volatile, a move to a higher margin concept makes sense to us at first blush.

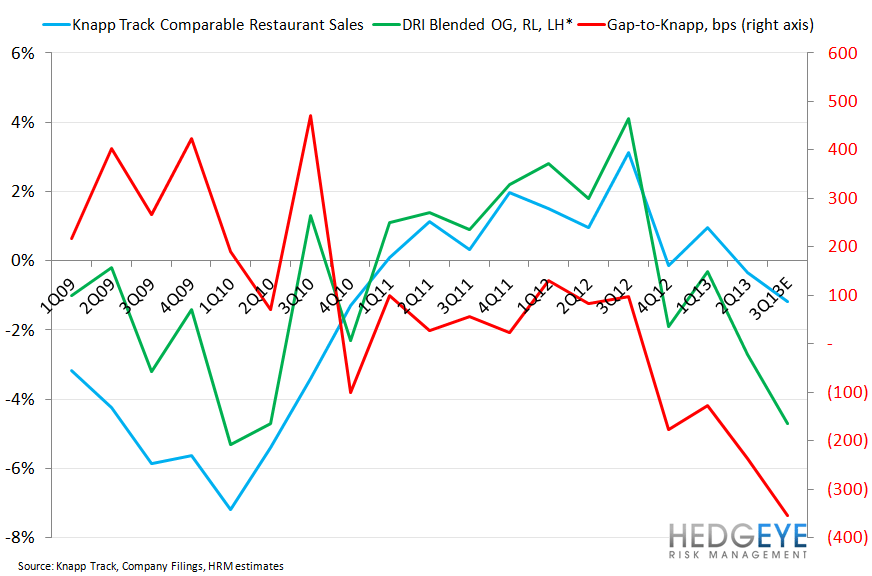

Sales

As preannounced, sales continued to be soft at Darden’s core brands during the third fiscal quarter. With Knapp Track comparable restaurant sales decelerating to -5.4% in February, we would anticipate that trends deteriorated intra-quarter at most, if not all, of Darden’s concepts. The chart below shows what the sequential acceleration in the Gap-to-Knapp that is implied by Darden’s preannouncement late last month.

Win-Win

Given the dividend, which it seems management is intent on preserving, and the fact that Knapp alluded to improving casual dining trends in March, we do not see significant downside to the stock from here. We believe, that after years of underperformance, any significant deterioration in guidance is likely to prompt intervention by an activist investor. Even at current levels, we believe the breakup value of the stock is exceeds the current share price. See the slide deck of our recent call for more details.

Howard Penney

Managing Director

Rory Green

Senior Analyst