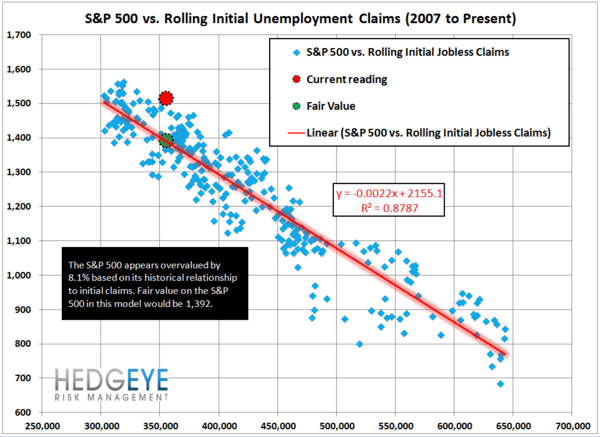

Investment Positioning Review: With the Housing and Labor Market data remaining positive alongside a strong dollar and commodity deflation, we remain positive on equities (US/Asia, consumption focused) and negative on gold & commodities at current prices.

4Q12 GDP – 1st Revision: This morning’s first revision to GDP for 4Q12 registered a +20 bps improvement, shifting the growth reading from marginally negative (-0.1%) to marginally positive (+0.1%). The Consumption, Investment and Government components were all revised down small while the downward revision to imports & upward revision to exports provided upside to the net export figure which drove most of the positive change in the aggregate revision.

Residential and Nonresidential Fixed Investment growth were both revised higher while National Defense Consumption & Investment, the largest discrete drag in 4Q12, was largely unchanged at -22% Q/Q. Inflation estimates were revised higher with the GDP Price Index revised +30bps to 0.9%. Overall, despite the miss to consensus at +0.5%, we'd characterize today's print as benign from an investment or catalyst perspective.

Initial Claims: Headline Initial Claims declined 18K taking the 4-week rolling average down 6.75K to 355K. The direction trend in the 4-week rolling average of NSA claims remains positive but the rate of improvement declined sequentially, coming in at -2.6% y/y this week vs. -3.9% Y/Y in the prior week. As a reminder, the seasonal distortion tailwind in the reported data peaks in February before reversing course and serving as a headwind over the March – August period (more detail below).

Below is the weekly detailed analysis of the claims data from our head of Financials, Josh Steiner. If you would like to setup a call with Josh or trial his research, please contact

One Away

Everything's coming up roses with the recent initial jobless claims data, this morning's better than expected print included. This should come as no surprise to anyone who's been following our work. The end of February marks of the peak of the seasonality distortion tailwind. Next week will mark the final tailwind datapoint. Then, beginning in March, we'll start to see the effect reverse and the market's perception around the momentum in the labor market will begin to weaken and ultimately will turn bearish as the reverse effect peaks in August. It's also worth noting that the sequester takes effect tomorrow, and may result in a notable short-term spike in jobless claims if Congress doesn't take action.

For reference, the XLF dropped 20% in 2010, 32% in 2011 and 15% in 2012 beginning in the late February through mid-April timeframe in each of those years. We think a major factor component of the decline is this labor market seasonality dynamic. It's important to note that the effect is getting steadily smaller over time due to weighting methodology in the government's seasonality models. It's also important to note that last year's decline was conspicuously smaller, and shorter in duration, than the previous two years. We think this owed to the ongoing strengthening housing recovery coupled with the lessening effect of the distortion. We think those two factors will again be present this year, likely making the pullback more comparable to that of 2012 than 2011.

For those with a longer-term view, looking past the next 3-6 months, they should take some comfort in the fact that the latest week's data, on a non-seasonally adjusted basis, showed continued improvement. The YoY change in NSA claims was better by 8.0%, the largest YoY improvement in the last 5 weeks. However, the rolling 4-week average of NSA claims improved YoY by 2.4%, which was modestly worse than the 3.2% improvement in the previous week. The bottom line is that the real labor market is still improving, just not by as much as the market thinks.

Prior to revision, initial jobless claims fell 18k to 344k from 362k WoW, as the prior week's number was revised up by 4k to 366k.

The headline (unrevised) number shows claims were lower by 22k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims fell -6.75k WoW to 355k.

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -2.6% lower YoY, which is a sequential deterioration versus the previous week's YoY change of -3.9%

Joshua Steiner, CFA

Christian B. Drake