Loan Underwriting Standards Continue to Ease. Demand is Heating Up.

The Fed released its 1Q13 Senior Loan Officer Survey yesterday afternoon. The survey, which contains data on lending standards and loan demand across asset classes, was conducted between December 27th, 2012 and January 15th, 2013. Overall, the results were positive again this quarter with a few categories showed significant sequential improvement. We look at the results for each loan category below.

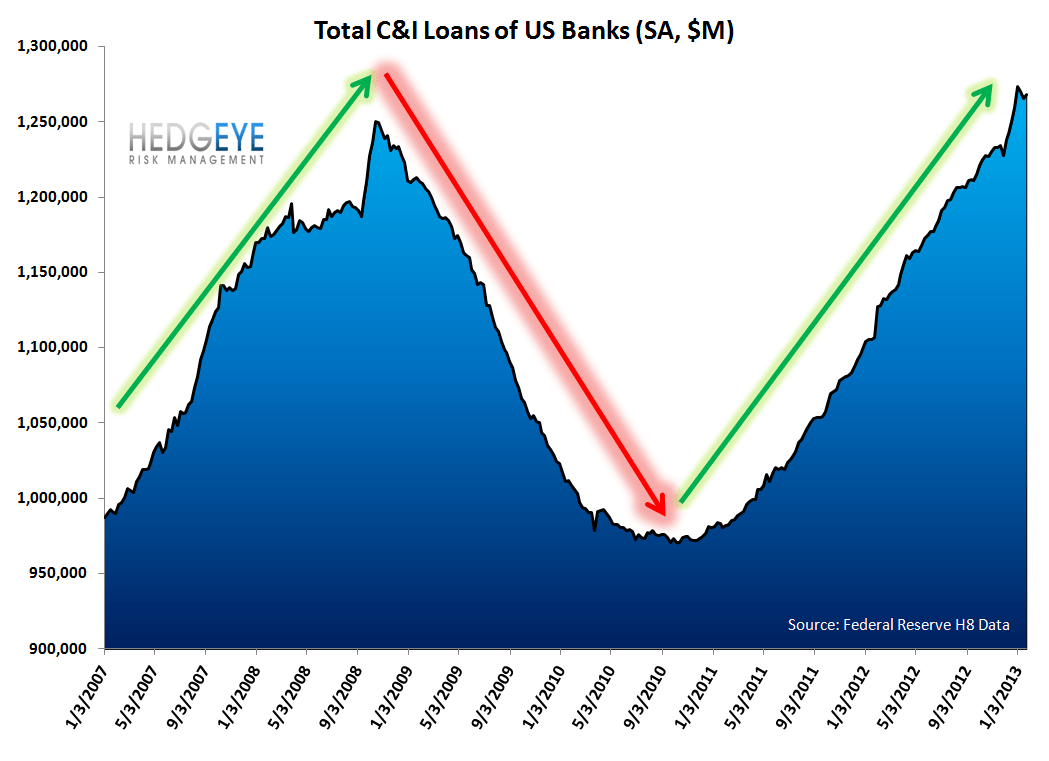

C&I Loans - Posting a Strong Sequential Improvement

Demand for C&I loans surged in the latest Senior Loan Officer Survey. Banks reporting an increase in C&I loan demand from large and mid-size firms rose to +19.1% from -6.2% in 4Q12. C&I loan demand among small firms was reported to have risen to +15.4% from +4.5% last quarter. Underwriting standards for C&I loans continued to ease at a rate comparable with what we saw in 4Q12. The same can be said for banks spreads: spreads are flat to down at a net 54.4% of banks on large firm C&I loans and 50.8% for small borrowers.

C&I lending remains the strongest area of growth for banks since the recovery began. In fact, C&I loans outstanding recently eclipsed their pre-crisis high. As such, this sharp increase in demand in the first quarter is a positive sign.

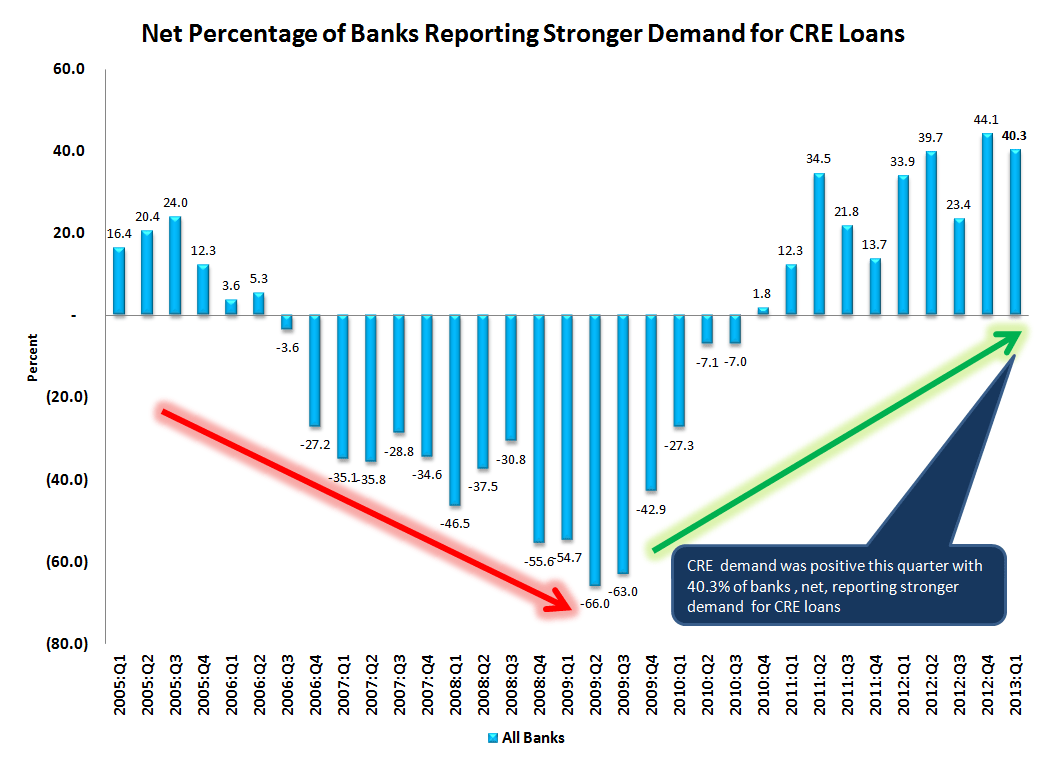

Commercial Real Estate - Demand Remains Strong As Standards Are Relaxed Further

Commercial real estate loan demand continues to heat up as debt maturities remain very high again this year, following a record year last year. Interestingly, you would think that all that demand would lead banks to be more choosey, but in fact the opposite has happened. CRE lending standards have eased each quarter since 2Q11 and this quarter was no exception.

Commercial real estate loans outstanding have finally begun to increase after posting years of decline following the bust of the real estate market. This is a significant inflection point, and should become a material driver of bank loan growth going forward.

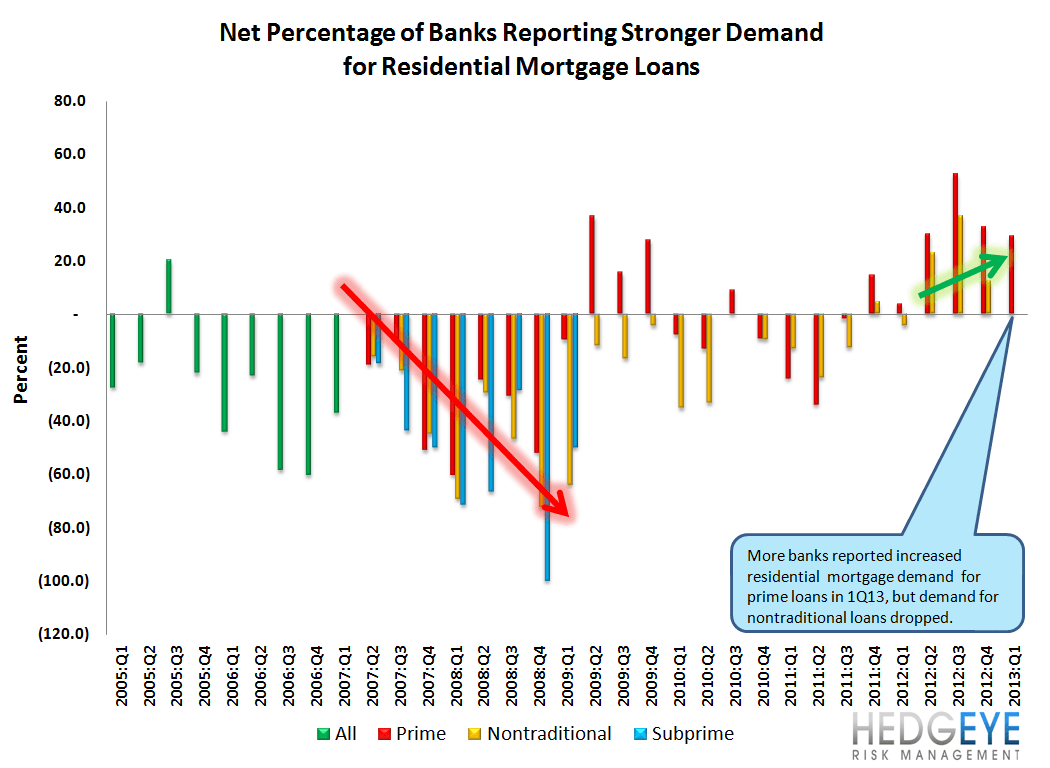

Residential Mortgage Loans - Prime Standards Easing

Banks reported a modest further net easing of standards on prime mortgage loans. On balance, 4.6% of banks reported flat to lower standards on prime resi loans. That is up from 1.6% last quarter. While not a huge change sequentially, the emerging trend of banks easing prime resi standards is a very important development that will continue to reinforce the recovery in residential real estate as additional cohorts of buyers find their way into the market.

It's also notable that Nontraditional resi loans saw standards tighten modestly (+2.9%), and that subprime loan standards were reported again. Bear in mind that the Fed hasn't reported a response on subprime resi loans since Q1 of 2009, so the fact that banks are even commenting on it is an indication that subprime loans are starting to re-emerge. That said, on the margin, 20% of banks reported tightening standards on subprime loans, likely in response to the recently issued new QM rules.

On the demand front, however, borrowers continue to show greater interest. 1Q13 marked the sixth consecutive quarter of banks reporting QoQ growth in prime residential mortgage demand. Naturally, much of this is refinancing demand.

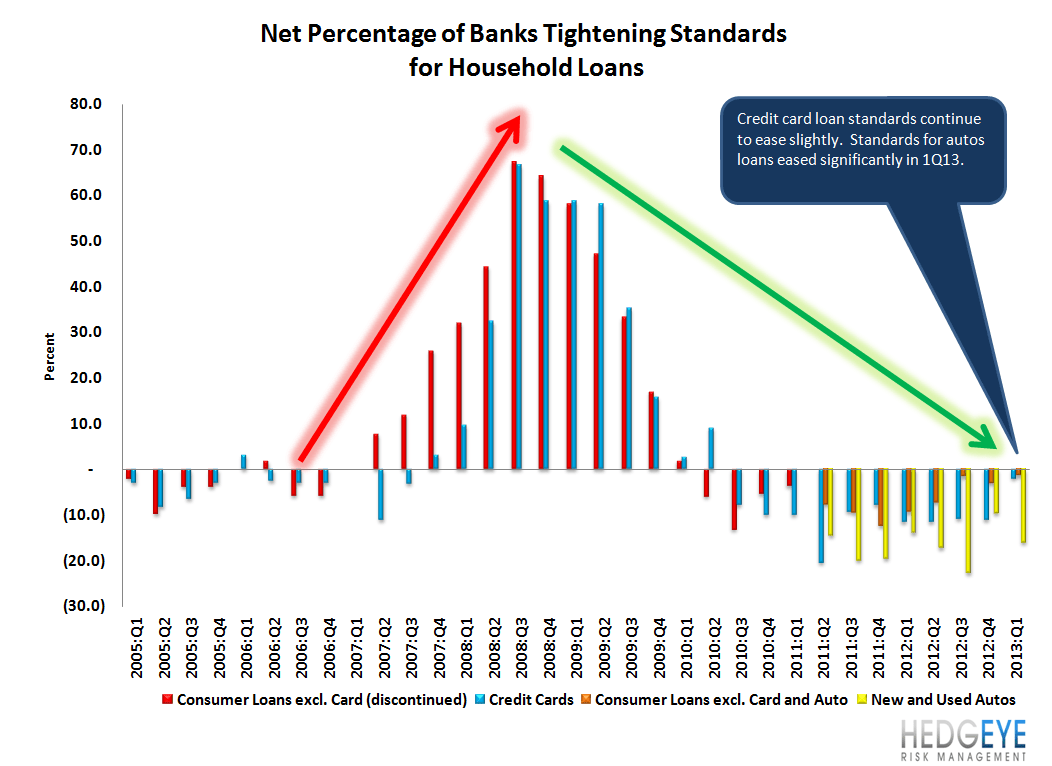

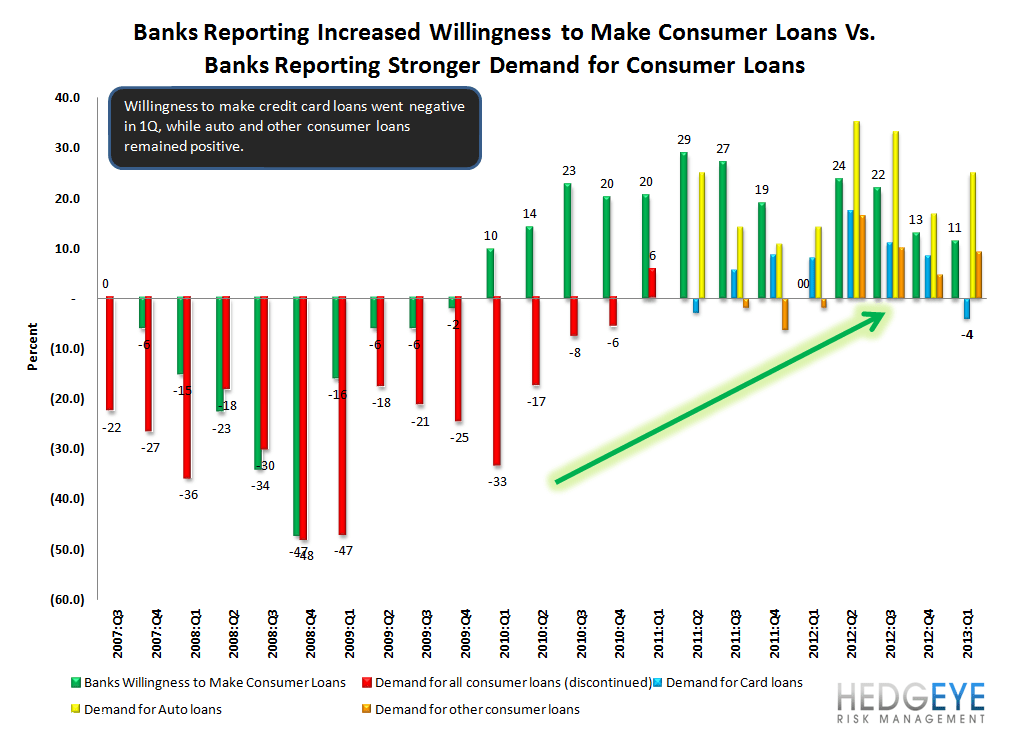

Two other noteworthy callouts are that demand for credit card loans took abrupt downturn in 1Q13 falling to -4% from +8.5% in the prior quarter. This is notable in that the prior six quarters were all positive. On the auto finance front, standards continue to ease while demand accelerated.

Joshua Steiner, CFA