This note was originally published January 30, 2013 at 10:03 in Macro

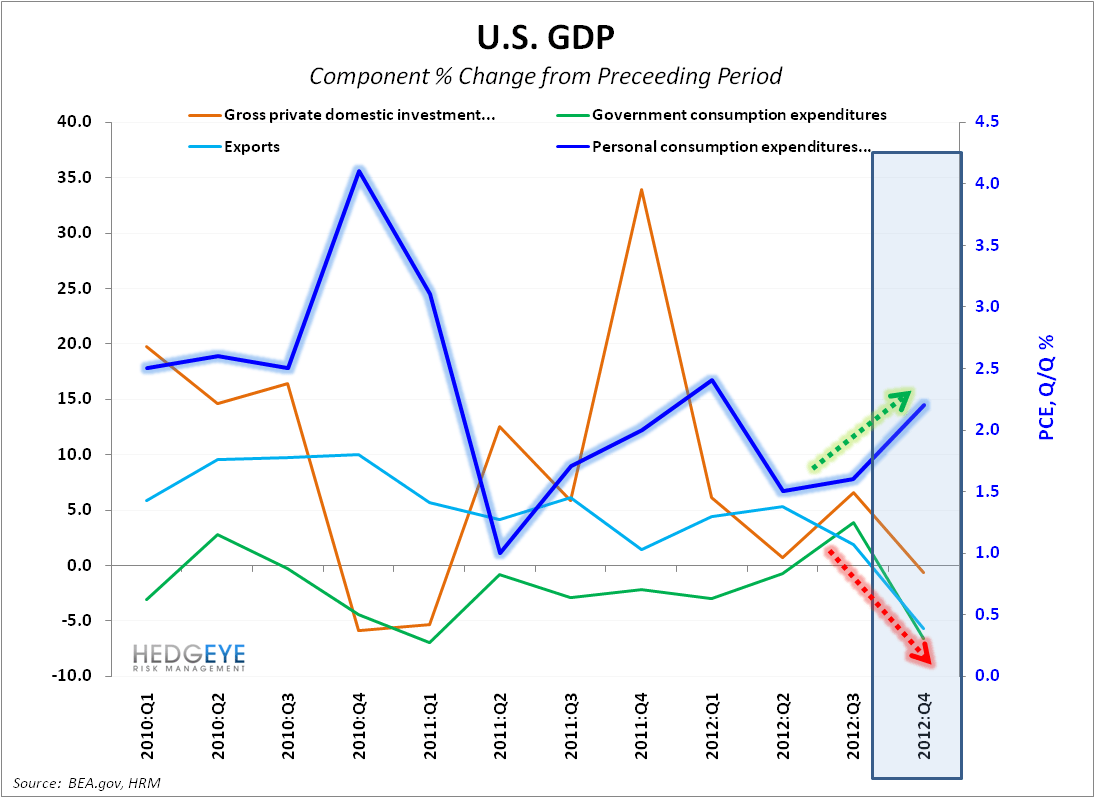

Looking across the C + I + G + (E-I) componentry, the callout contrast is the strength between consumption and the weakness across the balance of the other constituents. Personal consumption, which accounts for north of 70% of total GDP, accelerated sequentially for a net positive impact of 1.52% to real GDP. The negative outlier was Government Consumption and Gross Investment which went from an outsized positive impact in 3Q12 ahead of the election (+.75% impact, highest since 3Q09) to a material drag, contributing a -1.33% impact to net GDP.

Net-net consumption accelerated, Investment and Net Exports moved to flat from an impact perspective and Government Consumption and Gross Investment served as an outsized drag on the quarter. All-in, the negative headline print probably belies a more benign reality. Housing continues to recover, employment trends remain positive, and the high frequency consumer data remains stable-to-better.

Given these realities, does the market look through a rear-view 4Q GDP number and the negative influence of a government consumption component negatively impacted by odd comp dynamics? More than likely. As such, we are sticking with our forward looking view that growth is stabilizing, which is validated by the strength in consumer consumption.

As Keith highlighted this morning, from a tactical investment perspective, domestic and global equities are moving to overbought and treasuries oversold, suggesting a near-term opportunity to book some gains and tighten up gross and net exposure a bit. The current risk range for the S&P500 = 1492-1513

Ping us at macro@hedgeye.com if you want to dig deeper into this report.

US GIP OUTLOOK: WHERE TO FROM HERE?

With the inclusion of today’s GDP report, which came in in-line with our expectations for a trip to Quad #3 in 4Q (see chart below), our updated estimate range for 1Q is +1.8-2% YoY and +2-2.3% for full-year 2013. The slightly lower handoff figure (i.e. 4Q reading) in the algorithm reduced these estimate ranges from +1.9-2.6% YoY and +2.3-2.6%, respectively.

What would get us to walk our estimates down from here (i.e. shift our expectations to the low end of our US growth risk range) would be a continued breakout in energy prices from current levels and a breakdown in the DXY through its 78.11 TAIL line of support. For now, however, an expanding yield spread (+29bps over the past month) augments our call for a move to Quad #1 here in 1Q13 and likely in 2Q13 as well. Expectations around this marginal economic delta should continue to bode well for domestic equities with respect to the intermediate term.

Christian B. Drake

Senior Analyst

Darius Dale

Senior Analyst