Starbucks’ top and bottom lines are facing favorable conditions, versus last year, and we expect management commentary on today’s earnings call to be bullish.

We expect some positivity from Seattle after the close today. As we wrote two weeks ago, CPG and international growth offer talking points for management to highlight the growth runway still facing this company on a global basis. An improving employment picture in the US could be an important driver of the company’s most important market.

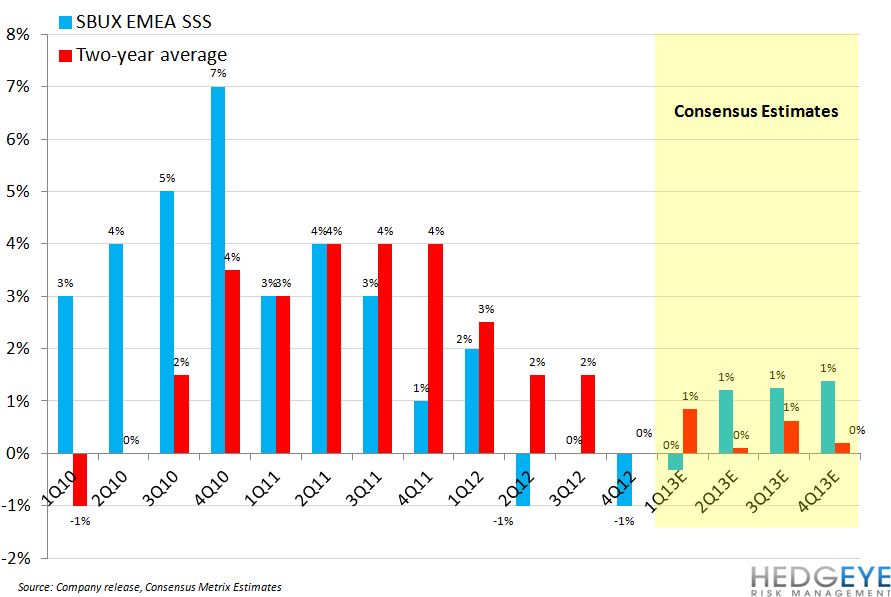

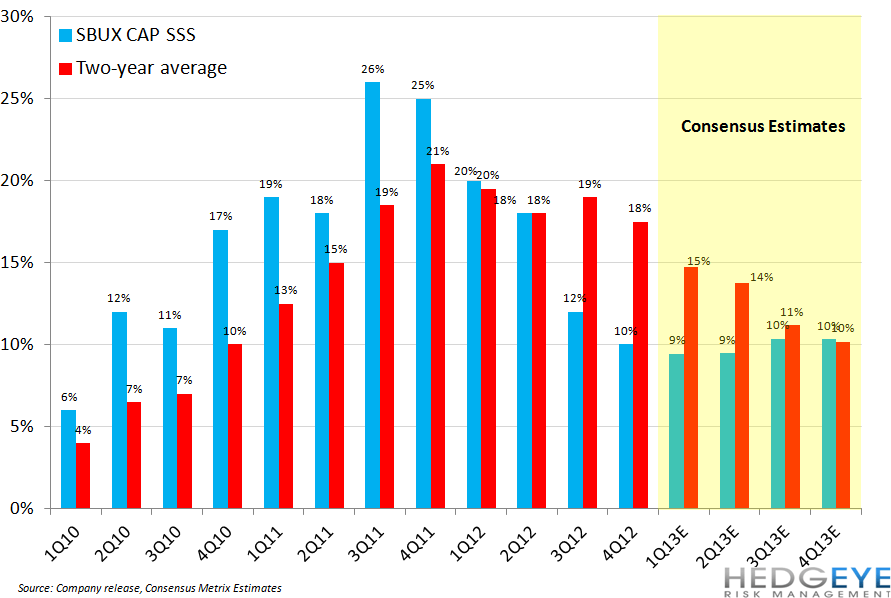

Below, we show the same-restaurant sales chart for the US and, in the third chart, the year-over-year change in restaurant operating margins versus the year-over-year change in the spot coffee price.

1. US Employment has been improving, as underlined by this morning’s initial jobless claims data, which came in at 330k vs 355k expected, and this increases our confidence in Starbucks’ ability to continue to drive industry-leading same-restaurant sales growth in the US.

2. Coffee needs are locked through 1HFY14 but, given the continuing softness in spot market prices since the company's most recent guidance, more positive news on input costs seems likely either on today’s conference call or at some point in the near future.

3. EMEA SSS will likely be negatively impacted by the UK market, where Starbucks has experienced some negative publicity related to its contribution to Her Majesty’s Revenue and Customs relative to the revenue the company sources in the country.

Howard Penney

Managing Director

Rory Green

Senior Analyst