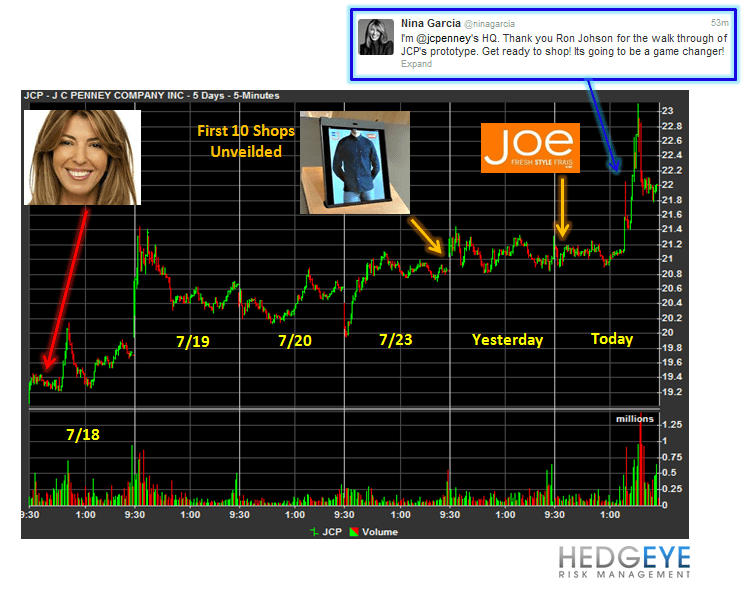

JCP closed up nearly 5% this afternoon following a tweet from the company’s new fashion curator Nina Garcia who said the new prototype is a “game changer.” Game Changers cost money- lots and lots of it.

Over the past Week, JCP has provided investors with several updates regarding its transformation from 400 brands to 100 shops which has put the stock back up above $22 from last week’s $19.06 low. Here are some details:

- Nina Garcia was announced as JCP’s “Resident Style Voice and Fashion Curator” on July 18th; Garcia is currently the Fashion Director of Marie Claire Magazine and Project Runway Judge.

- On Monday Afternoon, the company released details regarding its first 10 shops that will go into 700 of its 1100 stores by year end and some additional detail around the new format:

- August is all about Blue Jeans- 6 shops will debut (one in Men’s, one in Women’s per brand) with merchandise from Levi, Buffalo Jeans and Arizona. These will hit 683 of the 1100 doors though merchandise will be available chain wide.

- The Levi shop will feature 88 washes and 11 cuts ($40 a pair) and will offer shopping help through the denim bar which will be equipped with ipads to provide additional detail on each fit.

- September- Izod men’s shop, Liz Claiborne women’s, and one “JCP” branded shop per gender.

- Checkout Counters will be replaced with seating areas with sofas and long tables boasting built-in ipads and wireless internet.

- Town Square- Kicking off in August with free haircuts for elementary age students.

- Eliminating the 96 page monthly book which will be replaced by 2 weekly circulars that will focus on the new merchandise being offered (i.e denim in August).

- This Morning, the Joe Fresh shop was announced and will hit stores in April 2013 with a 1,000 to 2,500 square foot footprint across 700 stores.

As Canada’s largest apparel brand and priced similar to H&M, Zara and Top Shop, we think the Joe Fresh shop is a net positive from a brand perspective given the first 10 shops opening this year are legacy JCP brands with the addition of 2 “JCP” branded shops. Ron Johnson and Team will need to introduce several more new brands to drive the level of traffic and conversion required for the new concept to truly be a “game changer.” Regardless, “Game Changers” cost money- lots and lots of it, and JCP's got none of it (notice the nicely timed REIT sale days enforce end of the q). Sad.