Takeaway: Based on our math, the debt ceiling may be technically breached by late November, which may introduce a new and critical factor ahead of the November elections.

In the world of manic markets, the 2011 debt ceiling crisis seems like a lifetime ago. In reality, the deal to extend the debt ceiling in 2011 was reached on August 2nd, just under a year ago. In fact, President Obama signed the Budget Control Act of 2011 into law on August 2nd. This was the date that the Department of Treasury estimated that the borrowing authority of the U.S. federal government would be exhausted.

In true lagging indicator fashion, Standard and Poor’s downgraded the credit rating of the U.S. government a few days later. As outlined in the chart below, the U.S. equity markets, not surprisingly, were very volatile into and out of this. In fact, the volatility was comparable to the 2008 financial crisis with the Dow dropping north of 5.5% on August 5th alone.

Ironically, the debt ceiling had been successfully raised 70+ times from 1960 heading into the summer of 2011. The advent of the Tea Party elevated the debate on federal government debt and spending and turned a routine Congressional legislative activity into a major political football. The Tea Party pushed their Republican colleagues to reject any proposal that did not also incorporate immediate and sizeable spending cuts.

As noted above, the ultimate compromised proposal was the Budget Control Act of 2011 which had the following key provisions:

Debt Limit

- Debt was increased by $400 billion immediately;

- The President could request a further increase of $500 billion, which Congress could veto with a 2/3rds majority; and

- The President could request a final request of $1.2 -> $1.5 trillion, subject to the same super majority.

Deficit Reduction

- The bill outlined $917 billion of cuts over 10 years in exchange for the initial increase;

- The bill established the Joint Select Competitive Committee on Deficit Reduction to agree to cut at least an additional 1.5 trillion over the next 10 years; and

- If the Joint Committee did not come to an agreement on a bill of at least $1.3 trillion in cuts, then Congress could grant a $1.2 billion increase in the debt ceiling but this would trigger across the board $1.2 trillion in cuts equally split between security and non-security spending.

The widely discussed “Fiscal Cliff” in 2013 is a function of both a potential roll back of the broad Bush tax cuts and the automatic spending cuts outlined in the provisions of the Budget Control Act. In our Q3 2012 themes call tomorrow, we will go into a discussion of the “Fiscal Cliff”. In addition to this fiscal cliff and potentially even more pressing, is the issue of once again bumping into the debt ceiling.

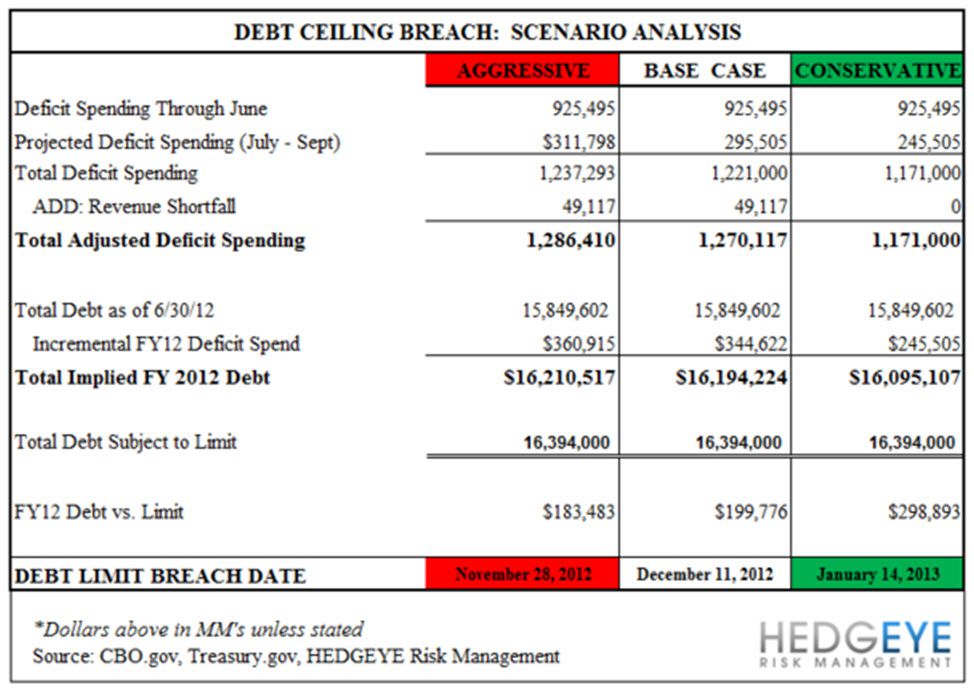

In the table below, our Healthcare team outlines three different scenarios when the U.S. may hit the debt ceiling. In the analysis, we show an aggressive scenario, base case scenario, and a conservative scenario. In the most aggressive scenario, the debt limit is breached on November 28th, 2012. In the most conservative scenario, the debt limit is breached on January 14th, 2013. In the aggressive scenario, the debt limit becomes a key issue in the 2012 election. On the other hand, if the debt limit is pushed into January, it becomes an issue just as the fiscal cliff becomes reality.

As our Healthcare team emphasized in a recent note, the post election period looks potentially very frightening as both the Fiscal Cliff and Debt Ceiling back up on each other within weeks. The post election period between November 6th, and the deadline for the “Fiscal Cliff” on January 1, 2013 may be more uncertain than last summer when volatility skyrocketed.

The wild card as it relates to some resolution of either the Fiscal Cliff or the Debt Ceiling may well be the increasing likelihood that U.S. Employment and GDP will still be growing at a vulnerable pace. In effect, it seems highly unlikely that a standoff over the Fiscal Cliff or the Debt Ceiling will materialize in the very short term as either or both items will likely induce a recession. That, of course, assumes that our politicians will act rationally, which is of course is not very likely in an election year.

Daryl G. Jones

Director of Research