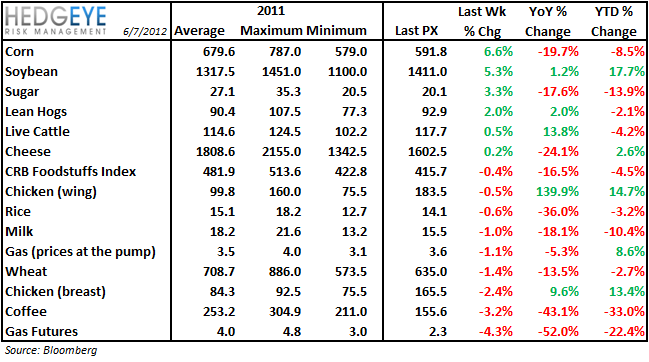

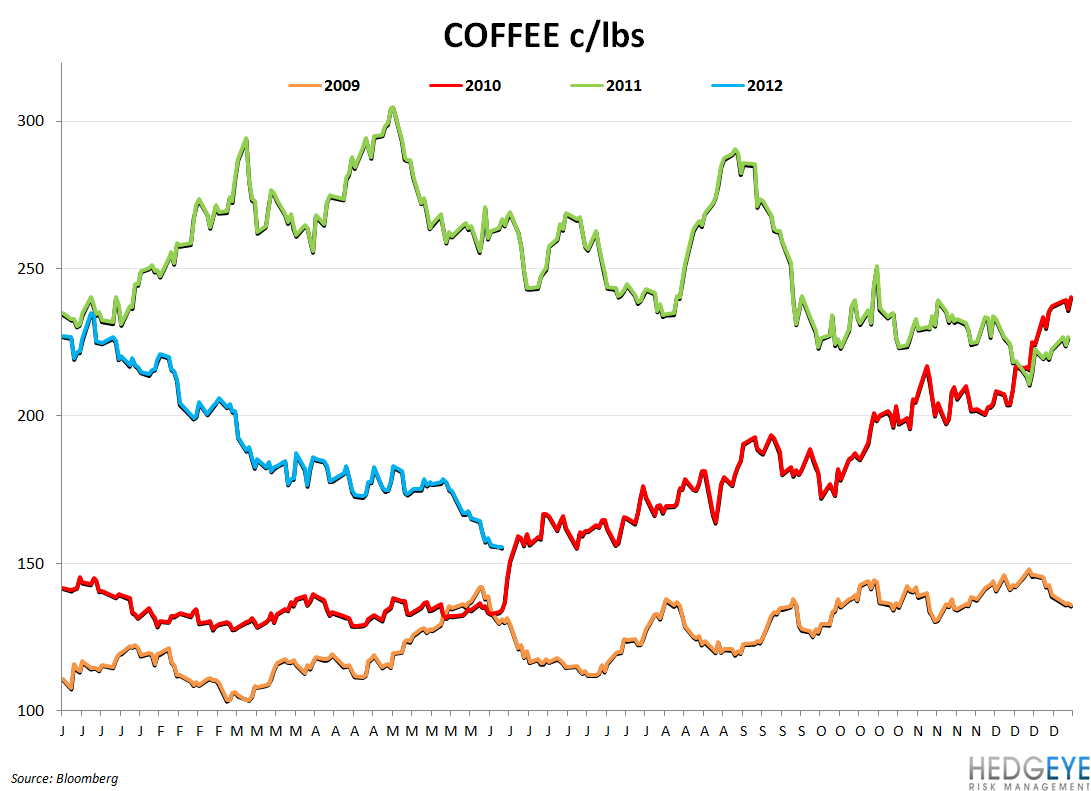

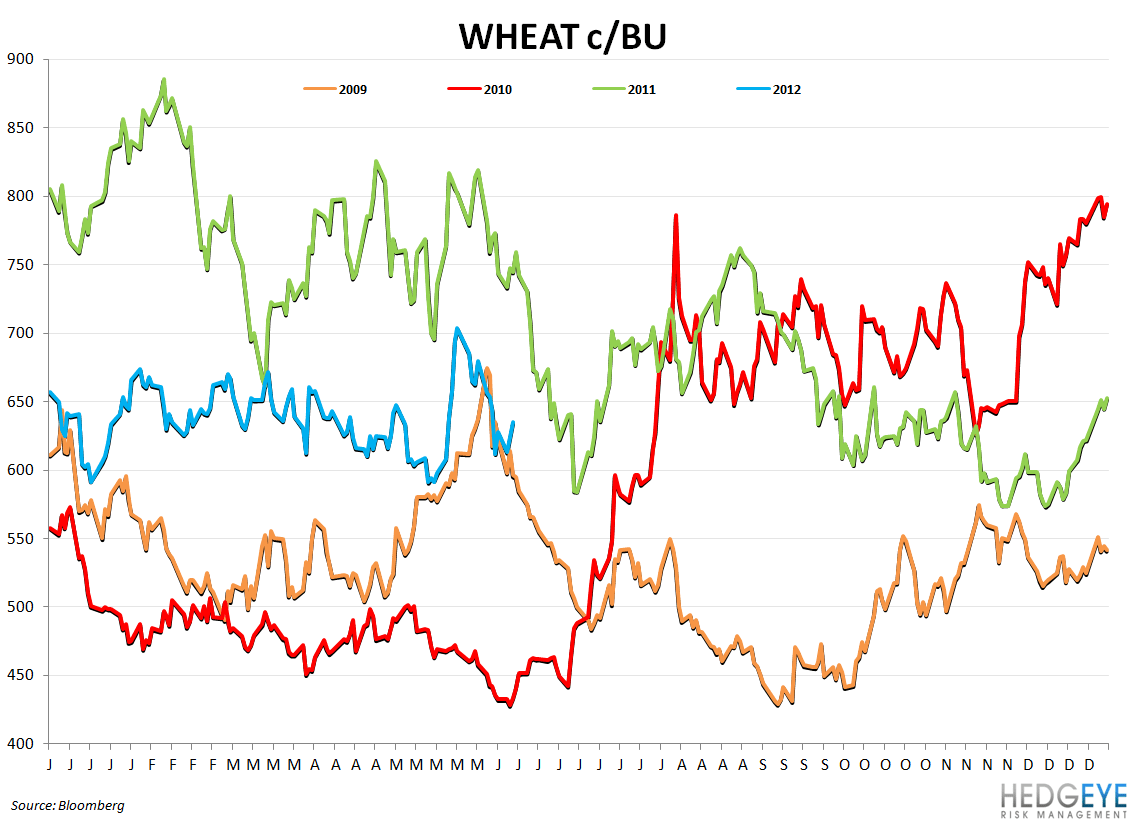

Dollar weakness sent corn higher over the past week which is has dampened the performance of SAFM and also drove beef prices higher for the week. There is still plenty of good news for restaurant companies with corn, wheat, cheese, rice, milk, and coffee all down double digits versus last year. Coffee and chicken breast prices were the biggest decliners on the week, of the foodstuffs that we track.

General Overview

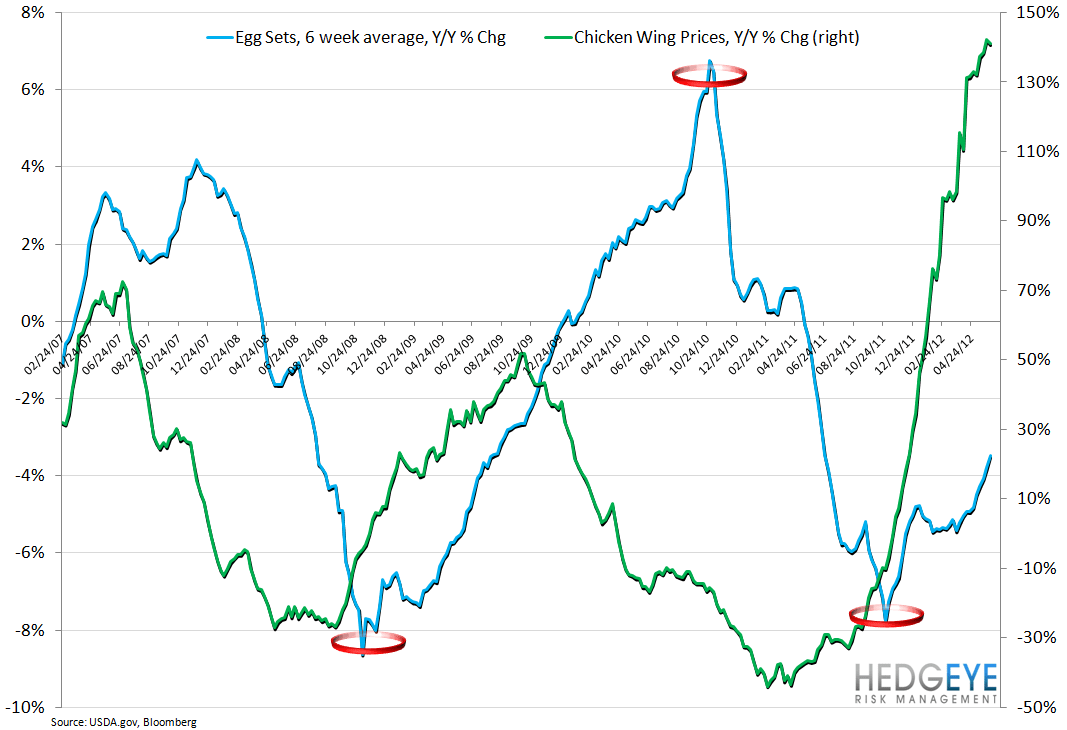

Chicken wing prices remain the standout item in our commodity monitor but a close second is the growing amount of red that we see on the table over the last few weeks. Increasing economic uncertainty and dollar strength is helping to bring down food costs for operators in the restaurant industry after a prolonged period of margin pressure in part due to rampant inflation in beef, dairy, coffee, and other items.

The chart of the CRB Foodstuffs Index versus the US Dollar Index, below, indexed from September 1stof last year, highlights the inverse relationship between the U.S. dollar and foodstuffs prices over the last nine months. As a firm, Hedgeye has been of the opinion that a Strong Dollar translates into Strong Consumption in America, which helps the top line growth of restaurant companies but it is also helping to relieve margin pressure – as the chart below shows.

Gasoline Prices

Gasoline prices continue to decline. The easing of pressure at the pump is having an impact on demand. According to AAA, US retail gasoline prices are now -5.5% year-over-year and consumers are responding. Earlier this week, Mastercard reported that the gasoline consumed over the 4 weeks prior to June 1stwas -1.9% year-over-year, which is the smallest decline since 9/16/11. Gasoline consumption has been negative, on a year-over-year basis, for 40 straight weeks as lower prices spur demand but the weak economy weighs on fuel purchases.

Beef Prices

Beef prices traded moderately higher over the last week as dollar weakness provided support. Optimistic expectations for this year’s corn crops, as well as economic concerns, had been weighing on beef prices but mounting concern that dry, hot conditions across the Corn Belt are sending prices for the grain higher. Below, we detail some thoughts on several companies’ exposures to beef prices.

JACK: Jack in the Box is one of our favorite longs. On May 17th, the company said that it expects beef costs to be up 5-6% versus prior expectations of high single-digit inflation. While prices have gone up since then, we do not think that the company will have revised its stance, yet. The company also said that, if beef prices were to continue to “stay low”, its guidance of 14.5-15% for restaurant operating margins might could have been conservative. We think expect its restaurant operating margin to come in close to that target given the recent gains in beef costs. Beef, which is 20% of the company’s spend, is the biggest wildcard in its commodity basket.

WEN: Wendy’s, like Jack in the Box, purchases fresh beef (20% of its basket) on the spot market. On May 8th, the company said that it expected beef prices “back up” by the fourth quarter and that its purchasing is pretty much “at market with a three months lag as you see the impact of market changes on beef”.

TXRH: Texas Roadhouse, as of April 30th, had pricing arrangements in place for well over 90% of its beef.

Chicken Wings

We have to highlight, once again, the resilience of chicken wing prices even as other commodities and protein costs roll over. Our conversations and analysis continue to point to undersupply in the market which, given the price action, is not being addressed by the marginal increases in egg sets that the data is showing every week. As the chart below shows, egg sets are still declining at ~4% year-over-year.

Correlation Table

Charts

Howard Penney

Managing Director

Rory Green

Analyst