Conclusion:

The irony with VRA is that positives actually outweighed the negatives with this print – albeit modestly – and the stock is still down 10%. Apparently short interest as a percent of float at 47% was not a factor. Our long-term (which is evolving into intermediate term -- i.e. reality) concerns remain 100% in tact, and there was little in the quarter that we heard to change that. Consider the following:

On the plus side…

- The print came in ahead of our expectations. It was driven by costs, some of which was timing-related, some was not. Nonetheless, not what we will pay up for in looking at a name like VRA. A beat, yes. But not a clean one.

- The company is accelerating door growth at Dillard’s by nearly 2x. Initial plans were to add another 60 doors this year. VRA opened 41 new doors in Q1 alone and increased its plan to add 110 new doors (175 in total).

- In addition, VRA announced its second department store partnership with the mid-west chain Von Maur. With 27 stores, it’s not exactly a national retailer with incremental door expansion opportunity, but a net positive and vote of confidence from the department store channel and incremental boost to Indirect revenues.

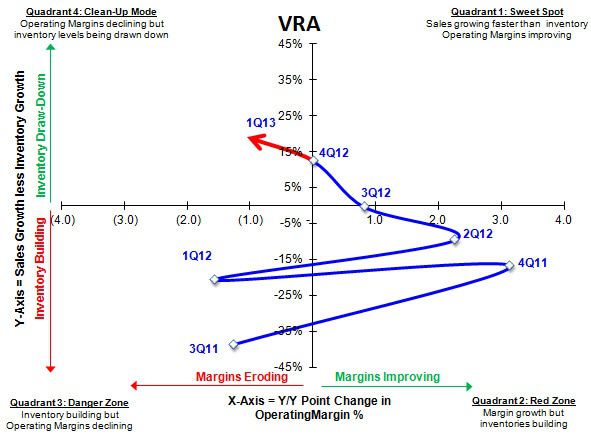

- Inventories look good down -3% with the sales/inventory spread up +7pts to +19%. It turns out that timing artificially boosted this figure due to a ~$7mm push of inventory into 2Q. But even after adjusting for the event, the +12% spread looks good.

On the negative side…

- The company continues to move at a feverish pace to open large wholesale accounts. We still think that the motherload for VRA will be in connecting with JCP for a shop-in shop. That would be a big channel fill/short squeeze event. It would also do wonders for eroding its relationships with 3,400 wholesale customers – and its salesforce that serves them.

- Indirect sales were up +1.3% at the low end of management’s guidance.While the growth at DDS is very real and sustainable, we remain concerned about contraction at VRA’s small independent retail account base – a trend that even increased growth in the department store channel will not be able to offset over the intermediate-term.

- Comps came in up +4.3% a bit shy of expectations of +4.8% reflecting a continued deceleration in both the 1Yr and 2Yr demand. This is perhaps the most concerning trend as the company looks to aggressively ramp distribution. The underlying demand is not as strong as we’d like to see for a company looking to grow as aggressively as VRA is planning.

- A timing shift in marketing spend pushed into Q2 likely added $0.02 in EPS to the quarter. These costs don’t simply go away and the SG&A outlook for Q2 suggests that management is still expecting higher costs through 1H. We expect higher costs to continue due in part to investments made in 2H that we don’t expect to lever until Q4.

We’re not sure if this is a positive or negative, but in an effort to drive demand, the company is starting to enter categories that it thinks make substantially more sense than its foray into rolling luggage – an incremental positive if it can pull it off. While VRA now offers cell phone covers, the more notable addition is its bigger bet in the baby category with an expanded line of bags, throws and comforters to be launched next year. This is a positive change on the margin and could help reinvigorate demand, BUT we’re still a year out from when this product will hit shelves and VRA is not helping scarcity value by accelerating door growth in the meantime. The ultimate key will be to spend the right dollars in the right places, and take on the right licensing partners under the right terms.

All in, we’re shaking out at $0.35 for Q2 and $1.65 and $1.67 in EPS for F13 and F14 respectively 17% below the Street next year (F14). While the company is beginning to expand into categories that make more sense for the brand (i.e. baby), internationally into Japan, and further in the department store channel, we think these efforts are not enough to offset the declining core wholesale business as it becomes cannibalized by VRA’s own retail stores. We think that the best way to ensure success will be to spend behind it, and we’re not convinced that this is happening. Our model has SG&A and capex climbing in 2H and 2013.

What Drove the Beat?

Top-line sales came in modestly better than expected driven primarily by new store growth and e-commerce coupled with deferred spending resulting in the $0.02 EPS beat of $0.31 vs. $0.29E and our $0.27 estimate.

Outlook: In order to properly measure performance relative to original expectations, we look at management’s Q1 results relative to management guidance as well as any updates to previously provided full year 2013 outlook:

Highlights from the Call:

- EPS $0.31

- Revs +16%

- +34% rev growth in Direct

- Opened 5 full price, 1 outlet - new store showing some of strongest new productivity to date

- Now have 53 full price; 9 outlets

- E-comm +26%

- Added 41 DDS locations

- Expecting some near term revenue headwinds primarily in the indirect channel via the retirement of some carry over patterns

Product Launches:

- Summer collection has been well received by customers

- 2 fall releases : 1 in July with back to campus, 1 in August each with 3 styles and expanded assortment

- Will launch Ribbons for breast cancer awareness in September and a winter collection in October

- Recently launched cases for I phones currently featured in 100 Verizon stores nationwide in a licensing deal

- VRA launching new Baby category next year

Indirect: +1.3%

- Some of specialty retailers impacted by underperformance of carry over patterns which is impacting re order activity

- Will continue to grow indirect segment through furthering relationship with specialty retailers to grow productivity

Department Stores:

- Opened additional 41 DDS doors in Q bring current total to 106

- Plan to accelerate the addition of DDS from 60 to 110 bringing the total to 170+ this year

- New Partnership with Von Maur with 27 store footprint concentrated in the central US

Continue to be optimistic re long term opportunity in Japan

Direct: +34%

- Significant growth across all channels

- 51% of revs in Q1 vs. 44% LY

- Sales +63% by owned stores

- +4.3% comp increase

- e-commerce +26% (19% of sales)

- Driven by higher traffic and modest increase in conversion

- Have reduced size and scope of markdowns as the channel shifts to a more full price model

- Outlet revenues in line with expectations at $11mm

Gross Margin 55.7% in line with LY

- Reflects higher cotton and labor offset by favorable channel mix

SG&A: deleveraged by 80bps due to F12 infrastructure investments made last year and a shift of marketing spend that will take place in Q2 of this year

BS:

- Inventory: -4%

- ~$7mm in inventory received in Q2 that was expected in Q1 accounting for 7pt difference inventory growth (would have been +3%)

F2013 Outlook:

2Q:

Revs $121-$123mm

MSD comp

Indirect revenue growth of LSD as VRA addresses issues of carry over inventory

GM in line with prior year as they work through remainder of high cost cotton

SG&A $48-49

Other income $1.5mm

EPS $0.34-$0.36

Tax 39%

Share count 40.5mm

3Q indirect sales growth expected to be LSD-MSD

Full year:

- Net revs $535-$540mm

- Included indirect growth of LSD

- Expect 2H growth to be LSD-MSD as assortment changes

- Comps MSD-HSD for the full year

- GM expect to improve ~90bps for the full year up from previous guidance of 50bps

- Better visibility in input costs

- Favorable channel mix

- EPS $1.68- $1.71

- 39% tax rate

- 40.5mm shares

Expected to open 19 stores

Capital spending remains at ~36mm

Q&A:

Revenue Guidance:

- No expectation for higher churn in the channel

- Primary reason is the weakness in spring product assortment and its impact on independent retailers working through carry over inventory

- Reduction reflects reorder size vs initial orders

Back to College Strategy:

- Optimistic re 2H due to marketing campaigns around back to college

- Working hand in hand with partners to better understand the brand wide marketing that’s going on to help focus individual store marketing

- Traditional marketing elements going to all doors

Direct Operating Margins:

- Primary driver- earlier occupancy on some stores opening earlier expecting 8 stores in Q2, and 5 in Q3

- Outlet sales - primary promotion is about $11mm welcoming loyal shoppers and moved through older inventory which impacted margins

- Continue to strike the right balance of pricing in the outlet channel

Monthly Comp Cadence:

- Nothing particularly dramatic

Indirect:

- The balance between EOPs and reorders if 50/50 - currently a little heavy in EOP vs reorder but would prefer EOP to be less than 50% of reoders

- Some retailers have too much inventory and the wrong assortment in stores

- 25% of retailers dealing with some level of too much inventory or assortment

- At any given time with 3300 retailers there is always some level of the element in the channel

- Underperformance of Fall and Winter has increased the impact to some degree

- Some of the problems stem of independents trying to have every style in every color

- Reorders: focusing on synching supply and demand to fulfill orders with shorter lead times into the indirect segment.

- Q1 sales growth negative when excluding DDS stores

Dillard's:

- Originally anticipated $5mm but have not updated guidance given incremental openings

- Sales/foot productivity in line with direct performance

Von Maur – New Dept. Store Distribution:

- Launching into all 27 of their stores in conjunction with July release

- Roughly half of what is currently in Dillard's, not unlike the start at DDS

- DDS roughly 150 square feet, will start under 100 at Von Maur

- Von Maur not starting with Bedding but rather core assortment

- Expecting the GM to be slightly below that of the specialty store but OM essentially the same given the lack of labor cost

Carry Over Patterns:

- Those launched last July and September which collectively underperformed

- Patterns challenged the indirect segment

- Independents have a little too much

- Working to make sure independents are buying into the top selling patterns

New Store Productivity

- Have been getting more favorable real estate

- Focusing on having the right teams to open the store

- Please with performance of stores that have opened YTD

Inventory Levels:

- Result of internal efforts to evolve supply chain processes

- Comfortable with ability grow inventory in line with sales over the long term

Mother Day Performance in Direct Stores:

- Pleased with Mothers day - in line with expectations

Expansion plans:

- Goal of expanding into central US

- Continue to see a lot of data points pointing to the opportunity in the western US

- A lot of e-commerce traffic growth is coming from the central to west US

- 4 of top 5 markets of e-commerce traffic channel growth coming from West and Hawaii

Third Quarter sales Decline

- For indirect only

Comp:

- No major change in ticket

- Core drivers traffic and conversion

Rolling Luggage category:

- In line with expectations overall though still a small piece of the business

- Have recently been brought into DDS and is not quite meeting expectations

- Have new styles coming out in the Fall that should have positive impact

VRA Baby

- A historical challenged with new categories has been channel of distribution

- A number of independent partners are right for the category

- The real opportunity for baby gifting items are partners like DDS and Von Mar

- Dillard's showed a favorable response to seeing some of the baby product two weeks ago

- Will drive excitement and full price selling in the e-commerce channel

DC under Construction

- Currently all of the channels distributed out of current DC which is at capacity

- New DC will create capability to serve all of the various channels in a more specialized way