Today’s employment data was strong across the board for the restaurant industry.

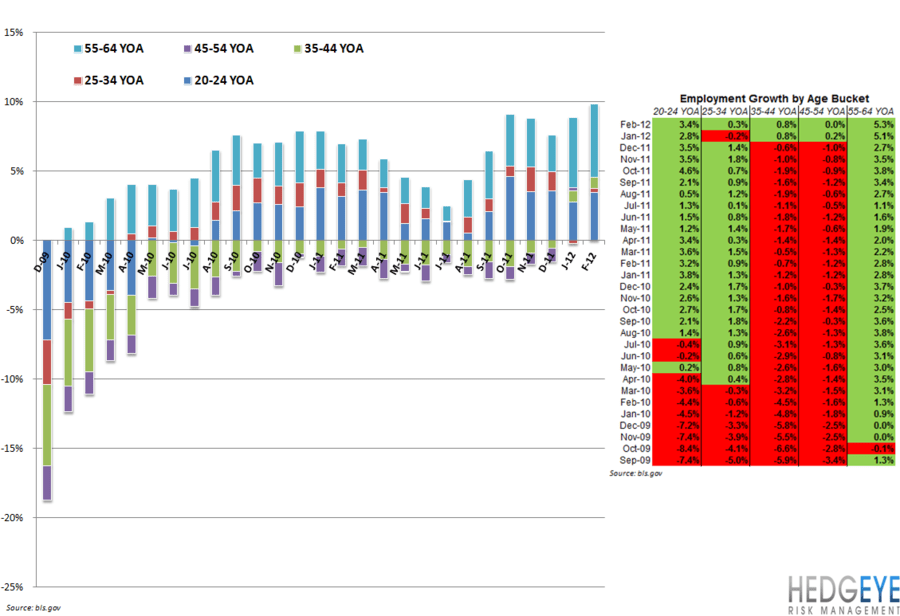

As the chart below shows, all of the age cohorts we track on a monthly basis avoided year-over-year decline in February. This is the first time we have seen green all the way across the table since February 2007. The 20-24 YOA cohort saw a 60 basis point sequential acceleration in year-over-year employment growth which is a positive for QSR companies. The one sequential slowdown in employment growth came in the 45-54 YOA cohort. Overall, this employment data is a positive for casual dining, given both the broad-based employment gains and the improvement in the older 55-64 YOA cohort’s outlook.

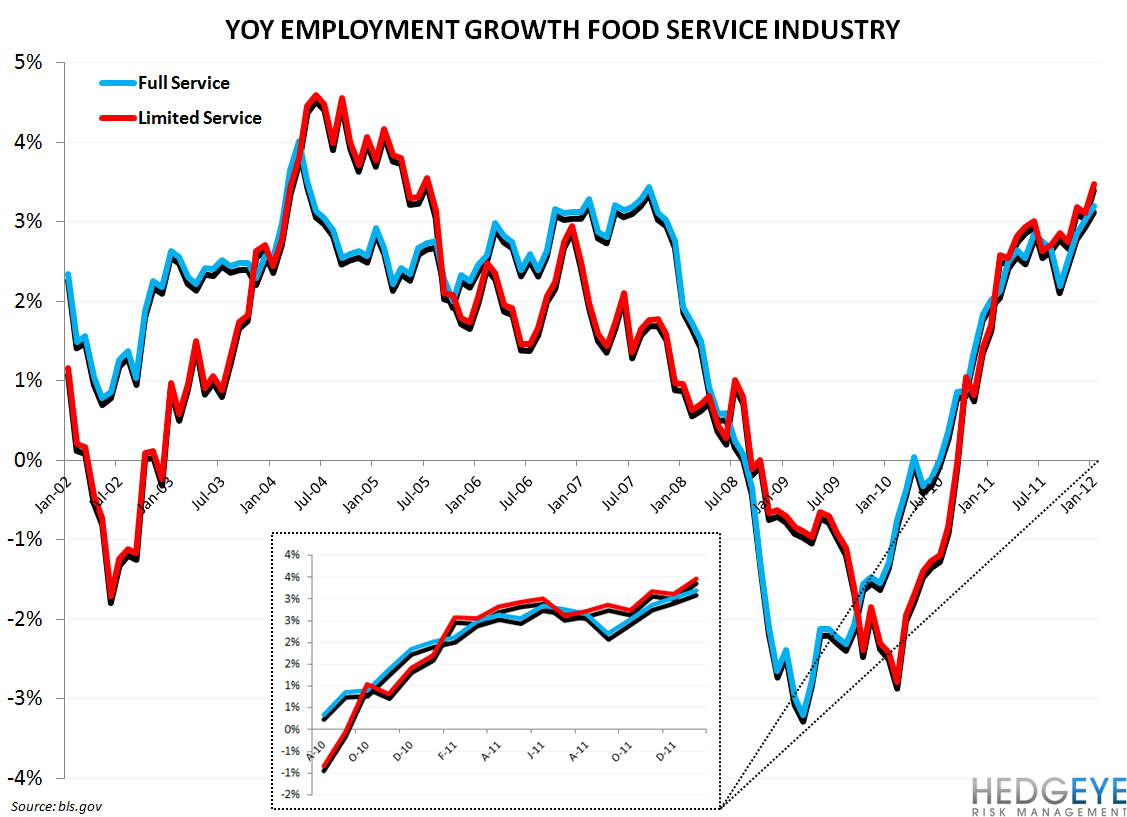

Hiring trends in the restaurant industry remain strong as of January (this data set lags by one month). As the chart below illustrates, hiring growth in the full service and limited service dining industries are growing at prerecession levels. The U.S. Employment Situation Report for February called out the food service industry as a bright spot in the recent employment trends:

"In February, employment in leisure and hospitality increased by 44,000, with nearly all of the increase in food services and drinking places (+41,000). Since a recent low in February 2010, food services has added 531,000 jobs."

Howard Penney

Managing Director

Rory Green

Analyst