Good Morning,

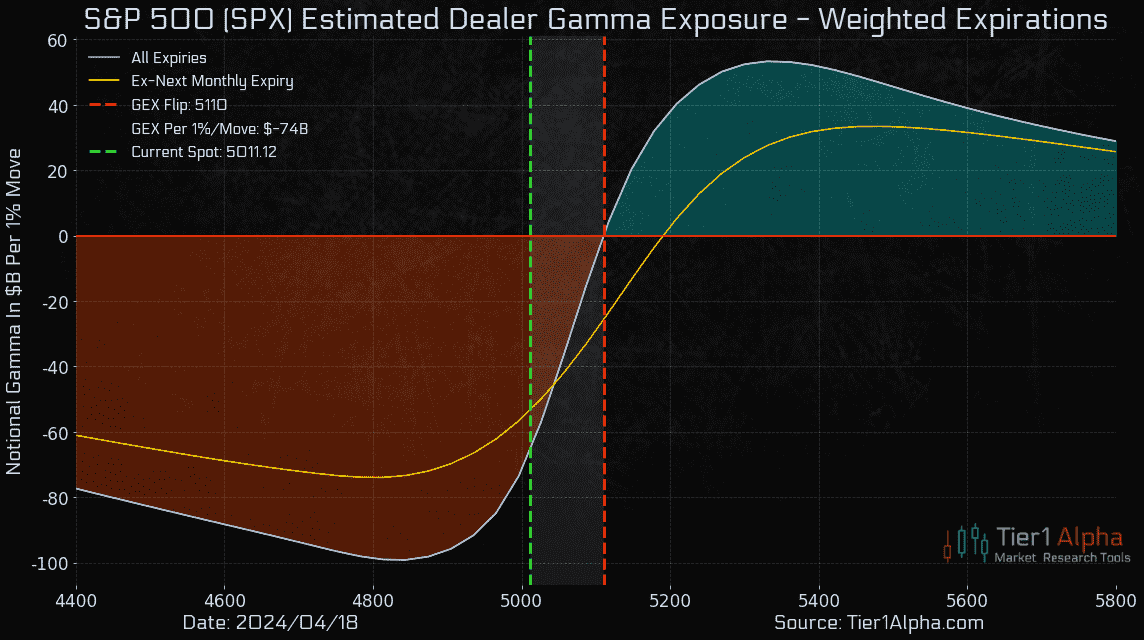

- Dealers continue to tread in negative gamma, which suggests the market remains susceptible to a sudden increase in volatility.

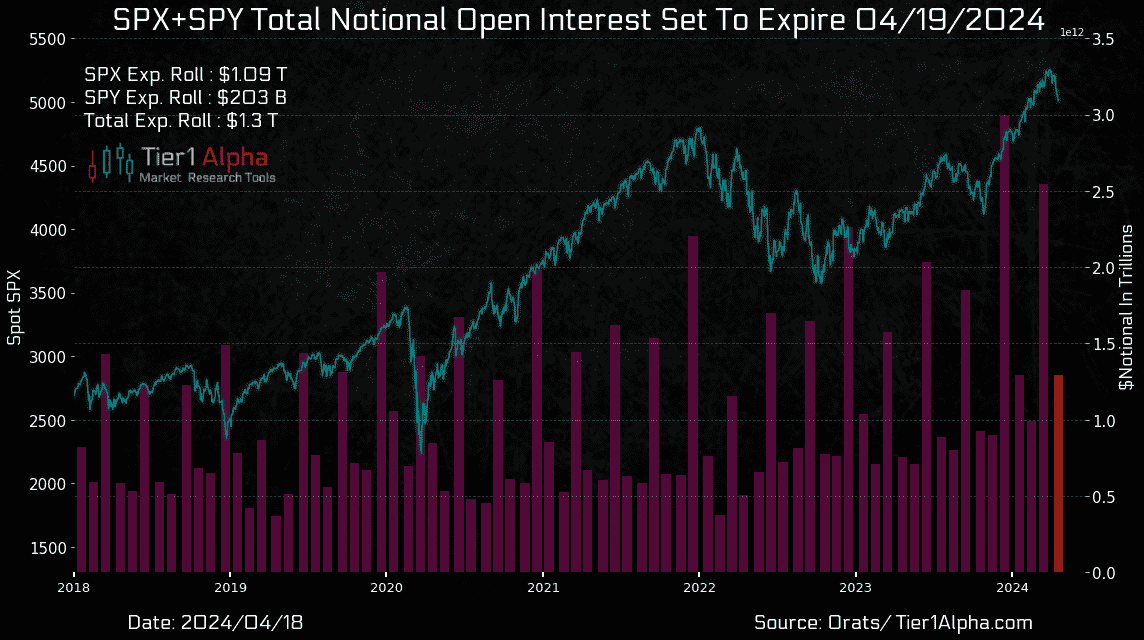

- However, after today's expiration, we should see a significant amount of gamma removed from the market, which will ease some of the hedging requirements market makers face. Overall, we expect to see around $1.3T in notional open interest either expire or be rolled into the next month's contracts, which is slightly above average for a monthly expiration.

- Even after OpEx, we expect market makers will remain in negative territory, since the gamma flipping point will shift back up to the 5200 strike, which is around 3.75% higher.

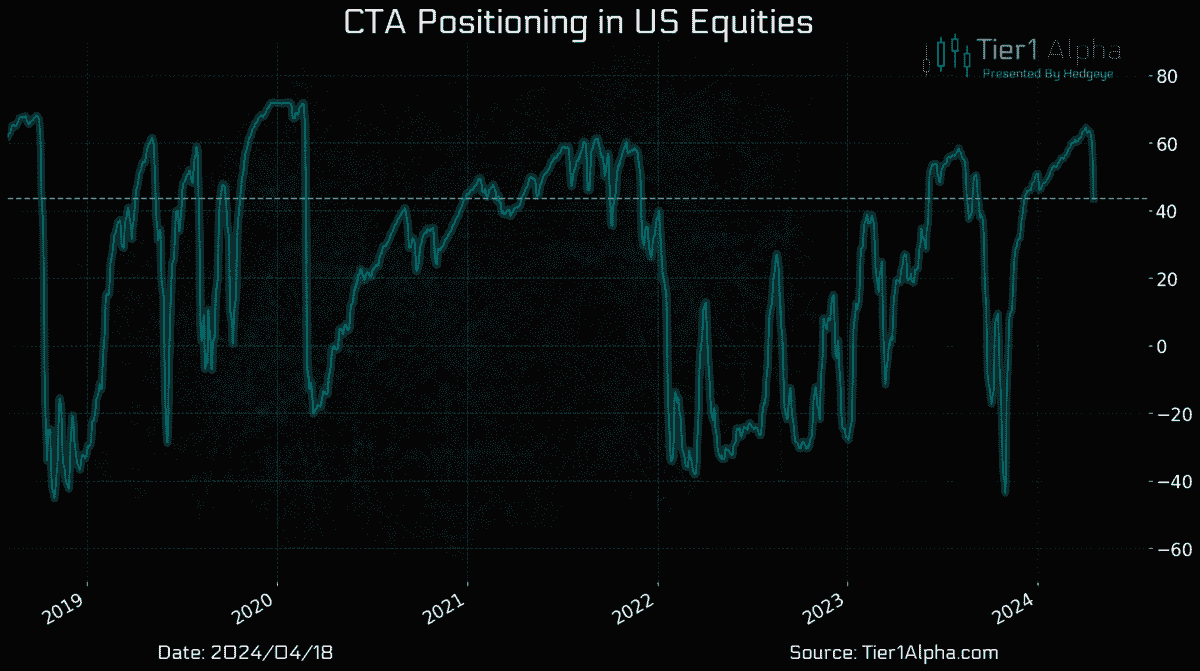

- This means we'll be entering the heart of earnings season in a higher volatility regime, while at the same time, geopolitical risks are rapidly escalating, and CTA funds have started deleveraging at the fastest pace in nearly 8 months.

- Given even just one of those factors, we'd expect to see a rise in volatility, but the confluence of all four vastly raises the potential for a more significant event.

- CTAs have sold off an estimated $20B in equities since Monday, but the selling flows from Vol control funds and Risk parity strategies have been much less aggressive. In fact, Vol control funds have actually been adding back around $7B in equity exposure over the past two days, although we suspect that’s the last bullish flow we'll see until the end of the month.

- In any case, that leaves a lot of potential deleveraging risk on the table if volatility increases from here, which is why we're still considering this an extremely dangerous setup from a positioning standpoint, especially as we head deeper into the Q1 earnings season.

For access to the full report, please click here!

-Craig Peterson