Good Morning,

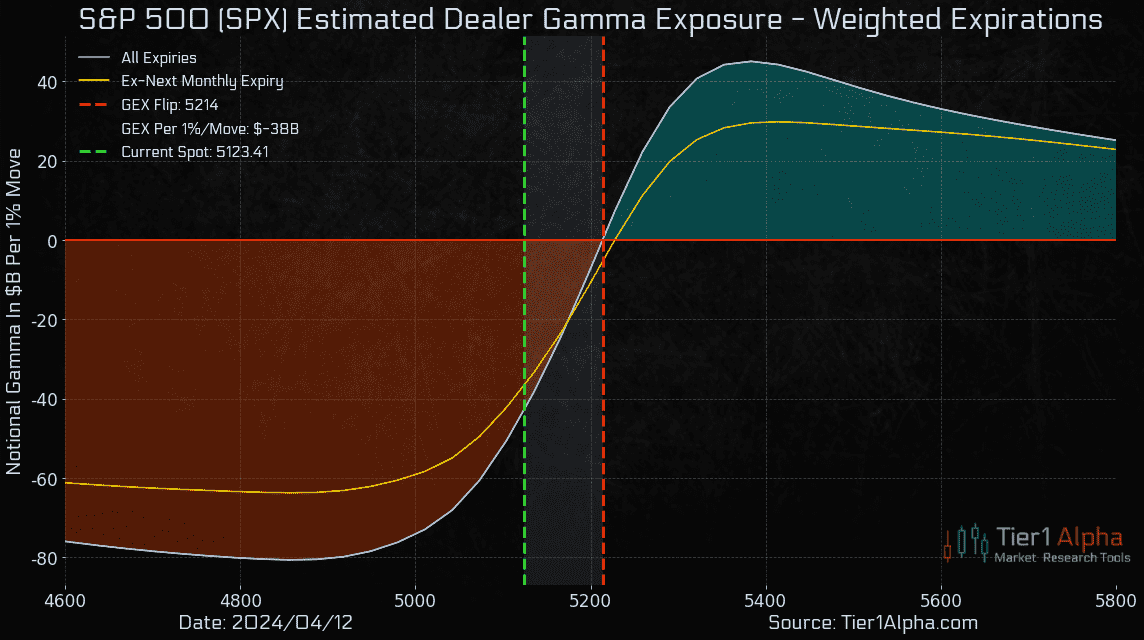

- Dealers will kick off the week in negative gamma, which means higher volatility should be expected. Although we can attribute last Friday's sell-off to various catalysts, including macro and geopolitical developments, the underlying mechanics of the decline were relatively straightforward.

- Ultimately, we suspect a bulk of the sell-off was driven by a considerable increase in demand for longer-dated Put contracts, which caused both premiums to surge and implied volatility levels to rise. As these Puts were net sold by the market makers, they were forced to hedge the deltas of these contracts by aggressively shorting SPX futures, which put further pressure on the market.

- The other byproduct of these Puts being sold is that it increases the overall negative gamma dealers have to hedge on any subsequent moves in the underlying. This means selling SPX futures when the market declines and buying back futures when it rises, which can create some additional volatility.

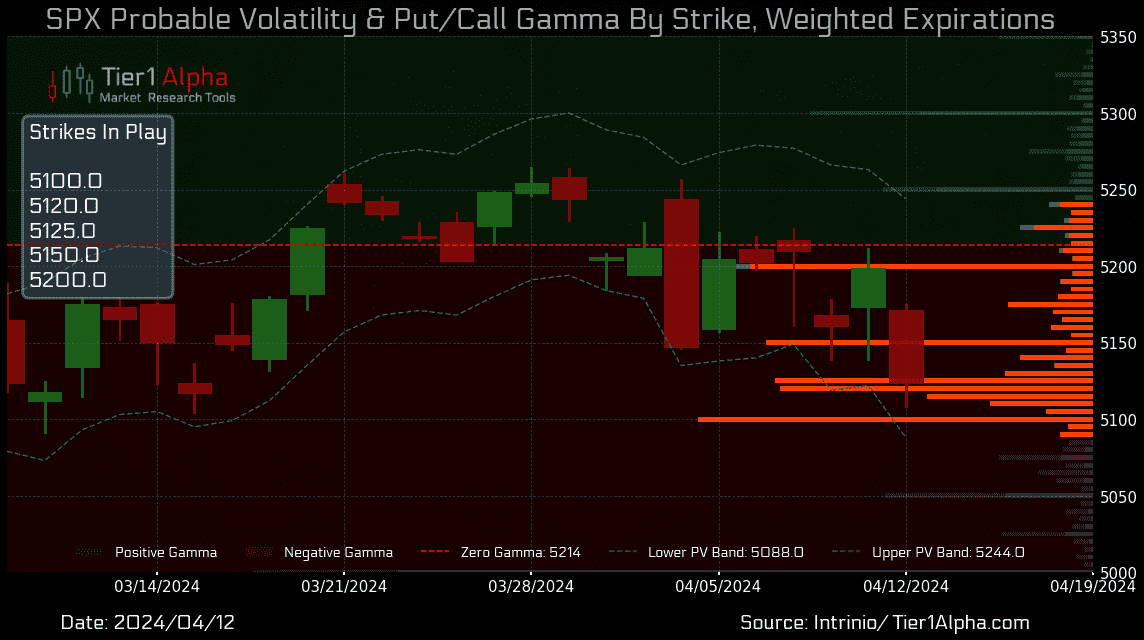

- Last Friday, our PV bands performed exceptionally well as the SPX closed within just one point of our lower range at the 5122 strike. However, following the move, our bands have shifted notably lower, bringing the 5100 strike back into play for the first time since mid-March.

- Although the overall direction of the trend is concerning, it also presents a significant potential for upside, particularly if we observe some of those weekend hedges being sold back to the dealers. Such a scenario would necessitate the dealers to buy back the deltas of those contracts, providing the fuel for a short-term rally in equities.

- Remember, though, upside volatility is still volatility, which presents its own set of risks, particularly with the Systematic fund community.

For access to the full report, please click here!

-Craig Peterson