Good Morning,

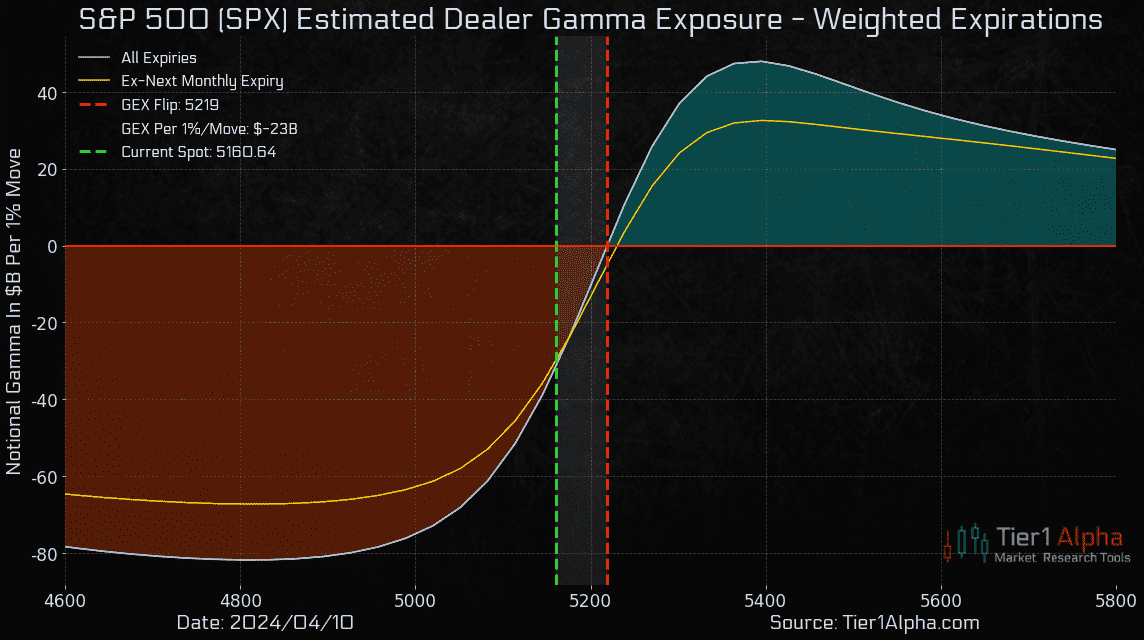

- Dealers slipped further into negative gamma yesterday, which suggests that more volatility could be on the horizon.

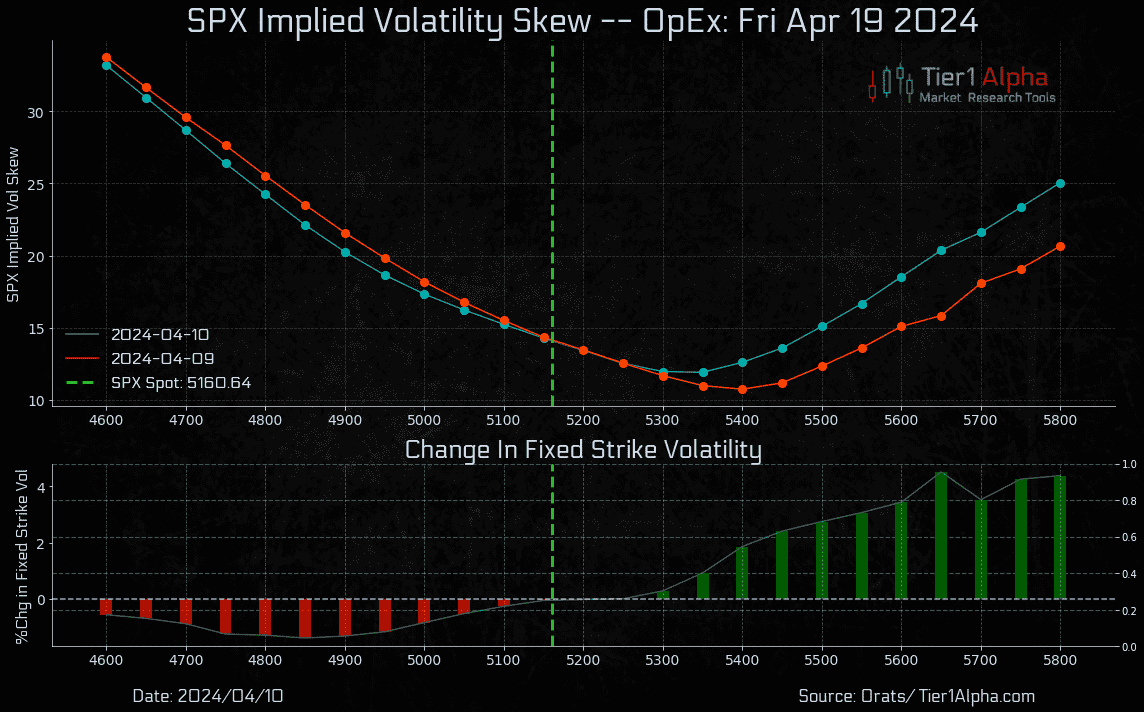

- Interestingly, despite the broad-based nature of yesterday's sell-off, there was no significant increase in implied volatility skew. This indicates that the downward move was not driven by a surge in demand for longer-dated put options.

- Instead, it's more likely that the sell-off was largely a result of dealers hedging their existing downside exposure, combined with some less predictable, actively managed flow.

- We're seeing a similar dynamic in our fixed strike volatility model, where implied vol for Puts slightly fell, implying the lack of demand for downside protection.

- On the other hand, there was a strong increase on the Call side, which we suspect was largely driven by Call overwriting programs, essentially betting that the market won't exceed the 5300 strike by the April OpEx next week.

- As a consequence of these Call options being net sold to the dealers, dealers become more long gamma, which will ultimately have a greater vol-compressing effect on the market if/ when the SPX approaches the 5200 strike again.

For access to the full report, please click here!

-Craig Peterson