This commentary was written by Dr. Daniel Thornton of D.L. Thornton Economics. Thornton spent over three decades at the St. Louis Fed as vice president and economic advisor.

The Fed recently made what many believe will be the last of the increases in its target for the federal funds rate. As was the case with all of the previous increases, the media suggested this rate increase will cause interest rates on car loans, mortgages, bank loans and virtually all interest rates to rise. In two previous essays (here) and (here), I demonstrated the Fed’s rate increases had no effect on the 30-year mortgage rate. This essay will present the reason the Fed’s actions cannot have a significant effect on interest rates. I will also present the evidence that the Fed’s rate increases since March 2022 didn’t affect interest rates.

The Fed cannot have a significant effect on interest rates because interest rates are determined in the credit market. The credit market is made up of a vast number of different securities that are connected in various ways through arbitrage. Arbitrage is the process of selling an asset with a lower interest rate (higher price) and purchasing a similar asset with a higher interest rate (lower price). Arbitrage is the glue that binds together all of the interest rates in this very complicated interest rate structure.

If the Fed were to lower the interest rate on say the 3-month T-bill significantly, market participants would sell T-bills and purchase similar assets. These actions would cause the 3-month T-bill rate to increase and the rate on the similar asset to decrease. The fact that Treasury securities are default-risk free makes them special, but there are other short-term securities that have very low default risk, e.g., 3-month high grade commercial paper. The critical point to understand is that there is a spread between the 3-month T-bill rate and other rates that will cause some investors to sell T-bills and purchase other securities. There is always a rate spread that will cause some investors to engage in arbitrage. Arbitrage is the reason the T-bill rate and the 3-month high grade commercial paper rate have tracked each other historically and particularly closely since early 2020.

For those readers who have taken a course in microeconomics, arbitrage is the financial market equivalent of the substitution effect of microeconomics: You might prefer Honeycrisp apples, but if there is a significant price difference between these apples and Fuji apples, then you will purchase Fuji apples rather than Honeycrisp apples. How large the difference must be to cause one to make the switch depends on the strength of the preference.

There is, however, a significant difference between the substitution effect and arbitrage. In the case of Honeycrisp apples and Fuji apples, there is a difference in the utility one gets from consuming the two products. In the case of arbitrage, the difference is always the same – the amount of income gain one can make by making the switch, or purchasing one rather than the other. Nevertheless, the more similar the two assets are, the larger the spread would have to be to get person to invest one rather than the other.

There also is the fact that the Fed has never taken actions large enough to have a significant effect on the total supply or demand for credit in the market. Given the enormous size of the credit market relative to any actions the Fed has taken, it is virtually impossible that such actions could have had a significant effect on the entire structure of interest rates, or on any particular interest rate in the structure.

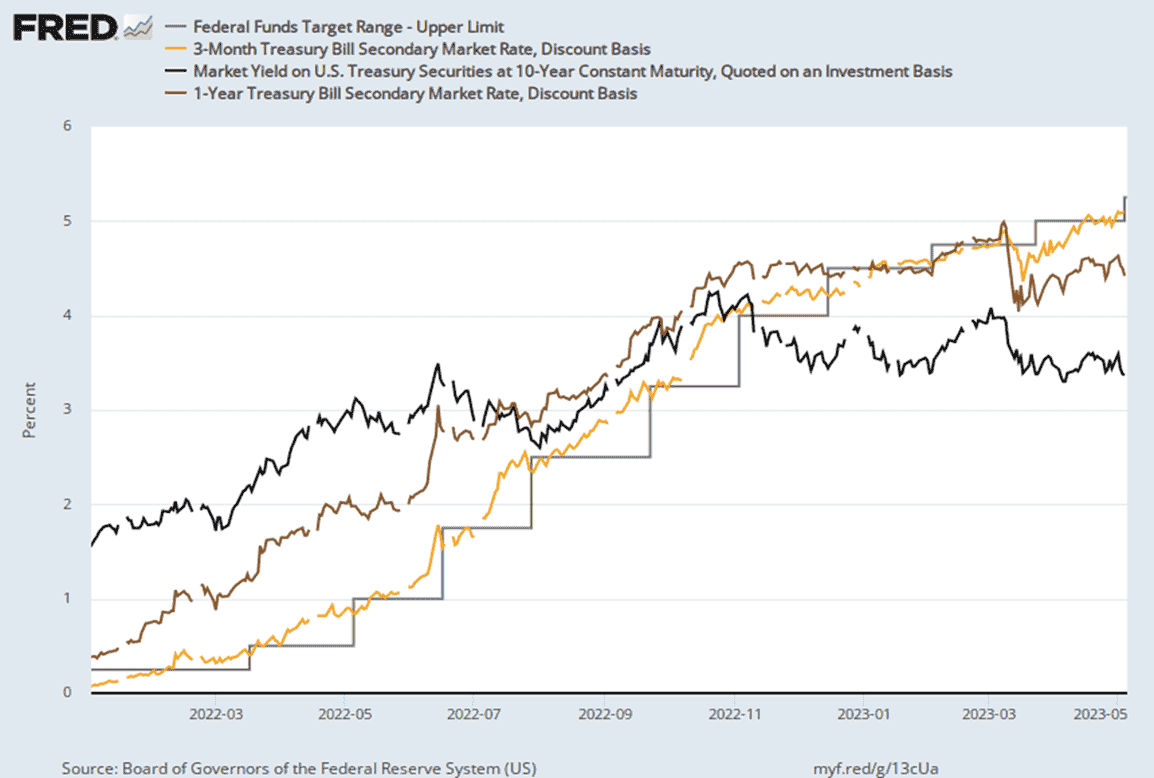

Now, let’s take a look at the effect of the FOMC’s recent rate changes on several interest rates. The figure below shows the upper end of the FOMC’s target range for the federal funds rate, the rates on 10-year and 1-year Treasuries, and the 3-month T-bill rate from January 3, 2020, to May 6, 2023. The figure shows that these rates were increasing long before each of the first six rate increases, when the 10-year Treasury rate started to decline.

The next four rate increases happened after the 3-month T-bill rate had increased. This fact suggests the FOMC was following the market rather than pushing interest rates higher. True believers will argue this happens because market participants correctly predicted the Fed would increase the target. Market participants' expectations can’t be known. This makes the belief that the Fed can affect interest rates a tautology. The belief that interest rates moved ahead of the FOMC’s announcements make the belief that the Fed can affect interest rates becomes an article of faith.

This belief is difficult to reconcile with the fact that increases in the FOMC’s federal funds rate target mimicked changes in the 3-month T-bill rate. The 3-month T-bill rate moved up almost exactly to the level of the rate increase, paused and then moved up to the level of the next increase. Movements in the T-bill rate almost exactly predicted the Fed’s rate increase: The larger the increase in the T-bill rate, the larger the increase in the target; the smaller the increase in the T-bill rate, the smaller the increase in the target.

This pattern is consistent with a previous essay (here), where I showed that during the period from July 2017 to January 2020, the FOMC followed interest rates up and down even though the Fed officials took credit for pushing rates up and then pushing them down. I quoted from FOMC statements, which suggest that at least four of these changes should not have been anticipated.

Finally, there is the fact that when the inflation rate began coming down, the 1-year and 10-year Treasury rates began to level off and even decline. This should not have happened if the Fed was controlling interest rates.

It is time policymakers and economists who believe that the Fed can significantly affect interest rates provide some non-tautological evidence – that is, scientific evidence – that the FOMC’s target changes have a significant effect on interest rates. If they can’t do that, and I for one believe they cannot, the belief that the Fed can move interest rates is more akin to religion than it is to science.

EDITOR'S NOTE

This is a Hedgeye Guest Contributor piece written by Dr. Daniel Thornton. During his 33-year career at the St. Louis Fed, Thornton served as vice president and economic advisor. He currently runs D.L. Thornton Economics, an economic research consultancy. This piece does not necessarily reflect the opinion of Hedgeye.