Positions in Europe: Short Italy (EWI); Short Spain (EWP)

As an update to our research note on 3/16 titled “Portugal Shakes on Debt Dues”, today we heard from Portugal’s PM Minister Jose Socrates that he increasingly believes that the main opposition party (the centre-right Social Democrats) are not willing to agree with his additional austerity programs to further trim the country’s budget deficit at tomorrow’s parliamentary vote. Socrates has previously announced that if the plan is rejected he would likely resign.

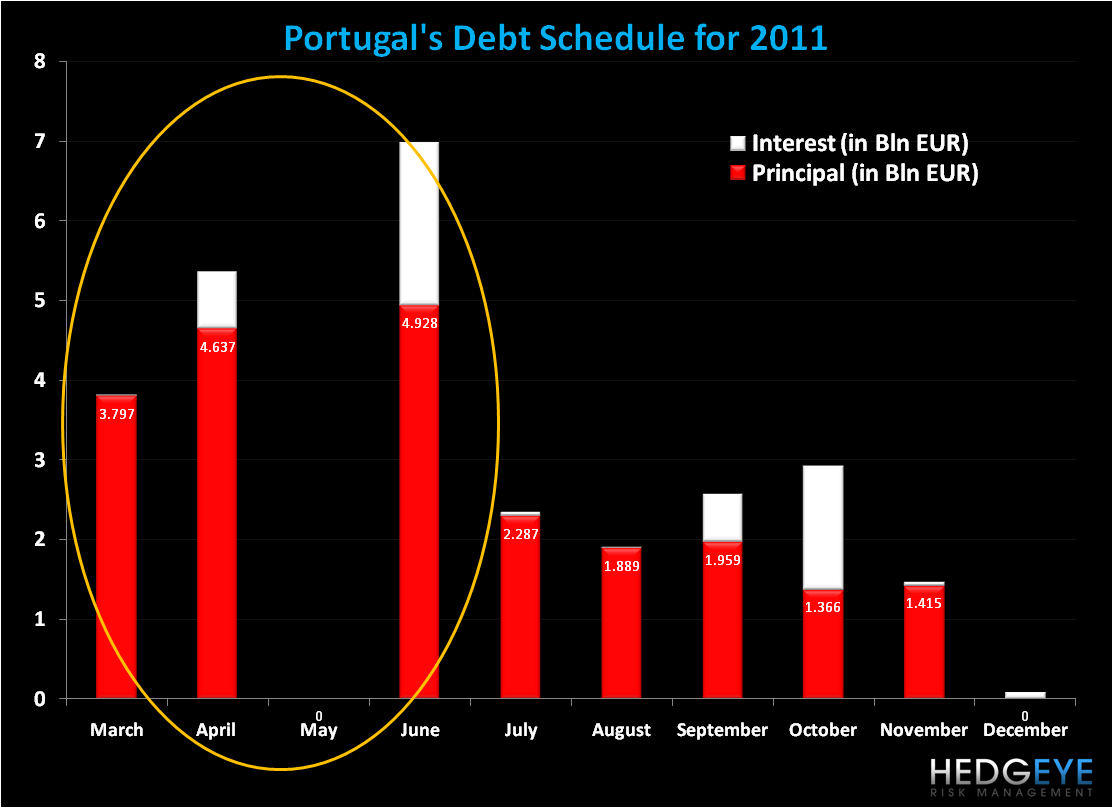

Should austerity be voted down tomorrow and Socrates call his resignation, which is looking increasingly probable, we’d expect the political indecision to heighten the need for and shorten the duration of a bailout from the European Financial Stability Facility (EFSF) to help shore up a hefty schedule of sovereign debt coming due over the next months (see chart below).

Socrates and his minority Socialist party’s new austerity plans aim to control operational and administrative expenses in the public sector. Given that the government on Monday recognized that annual GDP in 2011 will be -0.9%, versus a previous estimate of +0.2%, the government’s deficit reduction program over the next three years looks increasingly overly “optimistic”, as negative growth will further impair revenues need to pay down its deficits. The government’s budget deficit plan is: from 9.3% of GDP in 2009 to 7.3% in 2010, 4.6% in 2011, and to the EU limit of 3% in 2012.

If Socrates were to resign, a general election would follow; given the country’s constitution snap elections could be held at the earliest 55 days after called.

Tomorrow could well be another volatile day for Portugal and across European markets. Keep your head up.

Matthew Hedrick

Analyst