“The only real failure in life is not to be true to the best one knows.”

-Buddha

Yesterday was the biggest down day for US stocks since August 11th of last year. If and when the US stock market starts to really break down again, I think the only real failures in our industry will be revealed by those who have chosen not to evolve their global risk management process from 2008.

One down day certainly does not a bearish trend make. But a -2.1% drop in price momentum on an accelerating volume study of +31% (week-over-week) combined with a one-day rip of +27% in volatility (VIX) should definitely have the bulls’ attention.

PRICE, VOLUME, VOLATILITY …

That’s the core 3-factor model I use across risk management durations. That’s what I have stayed true to since I re-built the model in 2007. That’s just part of my process. In order to embrace uncertainty as a given, I think a risk manager is best equipped to be Duration Agnostic.

The only real failure in my process would be choosing not to change the process as this globally interconnected marketplace changes. One of the key changes that I’ve made in the last 3 years is changing the durations in my models, dynamically, as volatility levels change.

I model all security level volatility from the bottom up, but to simplify this point I’ll use the VIX. Here’s where a closing price of 21.11 in the Volatility Index (VIX) fits across my 3 core risk management durations (TRADE, TREND, and TAIL):

- TRADE (3-weeks or less) = bullish, with TRADE line support at 16.17

- TREND (3-months or more) = bullish, with TREND line support at 18.09

- TAIL (3-years or less) = bearish, with TAIL line resistance at 22.09

So, in Hedgeye-speak, what’s happened to the VOLATILITY factor in the SP500’s 3-factor model is critical to acknowledge. Whether the TRADE and TREND lines of bullish VIX support hold or not is something that Mr. Macro Market will decide but, for now, what was overhead resistance in VOLATILITY is now support – and that’s bearish for US stock market price momentum. A breakout in the VIX above the TAIL line will make things crash.

Now if you take this 3-factor model:

- PRICE down

- VOLUME up

- VOLATILITY up

And overlay it with a critical correlation – the inverse correlation between the SP500 and the VIX – you’ll see that this relationship has been one of the most important concurrent risk management indicators we’ve been offered since the early part of 2008. Ignore it at your own risk.

In the chart below, you can see that this isn’t foreign land for me to be treading on. When I made the bearish call for a US stock market correction in April of 2010 (our Hedgeye Macro Theme was “April Flowers, May Showers”) I gave you the same signals.

Well, almost the same…

Nothing in my models are ever really the same, particularly when I blow out the vantage point to that other sneaky little critter called The Rest of the World. That’s why my baseline Global Macro Risk Management Model includes 27-factors (which also change and re-weight dynamically) and include important real-time prices like the US Dollar, Indian stocks, Copper, etc…

And this is really where I can look myself in the mirror and say, despite the fierce lobbying for me to chase US stock market fund “flows” into their mid-February crescendo, I stayed true to the best top-down risk management process I know – when Global Inflation Is Accelerating, and Global Growth Is Slowing, it’s time to build up a large asset allocation to Cash.

Now not a lot of people have Street credibility on moving to Cash. Not only because they didn’t start making this move in early 2008, but because they don’t have an investment mandate that allows them to move into Cash. That’s an industry problem, not yours.

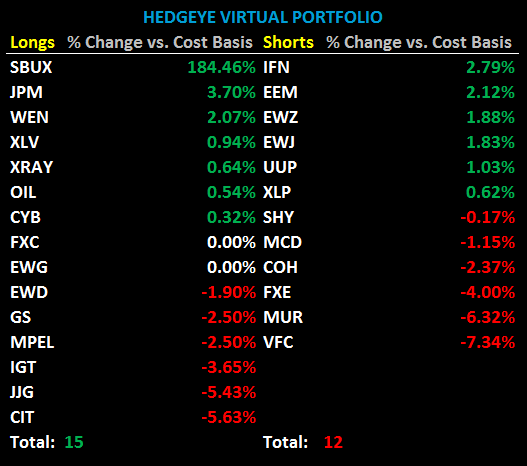

Global Growth Slowing is perpetuated by Global Inflation Accelerating. Anyone who has ever invested in emerging markets recognizes this basic reality. Everyone who is short Emerging Markets (EEM), India (IFN), and Brazil (EWZ), like we are in the Hedgeye Portfolio gets the profitability of it too.

The biggest question about Growth’s Failure in virtually all of Asia and the austere side of Europe that you can answer for yourself is will Global Growth Slowing affect the said “safe havens” of US and Japanese stocks?

My answer to this is not only implied by the high-frequency growth data that I grind through every macro morning, but it’s amplified by the math that stands behind the reality that Structural Long-Term Growth Is Impaired By Rising Sovereign Debts.

Whether it’s American, Japanese, or Western European debt, it’s all the same thing – debt. And that’s why we’re not surprised to see consumption growth slowing in these Developed Debtor countries as we infuse them with $95 oil and other inflation related taxes.

Growth’s Failure won’t be crystal clear to Wall Street until it’s in the rear-view mirror, but yesterday’s PRICE, VOLUME, and VOLATILITY readings combined with continued breakdowns in Asian Equities and a breakout in oil prices should read true “to the best one knows” about globally interconnected risks.

My immediate term support and resistance lines for the SP500 are now 1307 and 1330, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer