This note was originally published at 8am on February 10, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“The world is not dangerous because of those who do harm, but because of those who look at it without doing anything.”

-Albert Einstein

One of the most influential books that I have read in the last few years has been “Einstein: His Life and Universe” by Walter Isaacson. I say most influential because it fortified something within me that the best teams I played on took to battle every day on the ice. Courage.

If you are going to play this globally interconnected game of risk management at the highest level, you need to have the confidence and courage to play it with everything you’ve learned. You have to trust yourself and your process. You have to accept its weaknesses. You have to maintain opposing thoughts in your mind and remain calm.

You also have to be able to challenge accepted dogma, groupthink, and consensus when you have an opposing point of view.

Now that America’s Almighty Central Planner has laid down the Keynesian consensus, it’s time to take this puck right to the net on him and show the crowd what’s going on in this world outside of the bubbles that Ben Bernanke admits he never realizes he’s in:

To recap, Bernanke’s conclusions in his testimony before Congress yesterday were as follows:

- US Monetary Policy doesn’t affect Global Inflation

- US Inflation is benign

- US Dollars are “relatively attractive”

Let’s go through these in reverse order, given that’s how I’d weight the risk implied by a man with this amount of power who looks at the world right now without doing anything:

1. US Dollar – after a +1.3% three-day recovery ahead of Bernanke’s testimony, the US Dollar Index dropped immediately following his aforementioned comments and is now down for the 6th out of the last 7 weeks. The world’s currency market votes on credibility real-time.

With the US Dollar being bearish across all 3 of our core risk management durations (TRADE, TREND, and TAIL)… and without any respect or support from the manipulator of the world’s reserve currency, I don’t see why we shouldn’t be modeling a probable scenario analysis for another US Dollar crisis (i.e. a retest of its prior lows).

2. US Inflation – while Bernanke did point out that central banks hold more than 60% of their foreign currency reserves in US Dollars, he forgot to remind himself that “the Dollar is used in 85% of all foreign exchange transactions worldwide.” (Barry Eichengreen, “Exorbitant Privilege”)

Furthermore, there isn’t one major asset class in the world right now that implies that inflation expectations are low. Sure, the Fed’s compromised and conflicted calculation of inflation is benign, but we’re not willing to accept that as gospel. Here’s three ways to look at inflation:

A) Bonds – US Treasury and Emerging Market bonds have been going straight down, literally, since QG2 was introduced at the beginning of November of 2010. Inflation is bad for bonds. Bernanke is implying the entire global bond market has this wrong.

B) Stocks – Emerging Market stocks have been getting absolutely crushed since QG2 in November, 2010 and in the US stock market there’s a huge sector performance divergence embedded in the SP500 that is also inflationary. The S&P Energy Sector (XLE) is the best sector of the 9 we track for 2011 YTD at +7.51%, while the S&P Consumer Staples Sector (XLP) is the worst at +0.75% YTD. Ben, who is taking it in the margin? Bingo, the American consumer.

C) Corporations – Yesterday on the Coca Cola conference call (a relatively large company with a global footprint) this is what management had to say about inflation - citing bills for juice, plastics, and sweeteners, they saw a 60% ramp in cost of goods sold in the October to December period. Management went on to say that they’ll need to raise prices on beverages in the US in 2011 as it faces $300-$400M in cost increases from commodities. McDonald’s, Proctor & Gamble, and Sysco Foods have had similar comments.

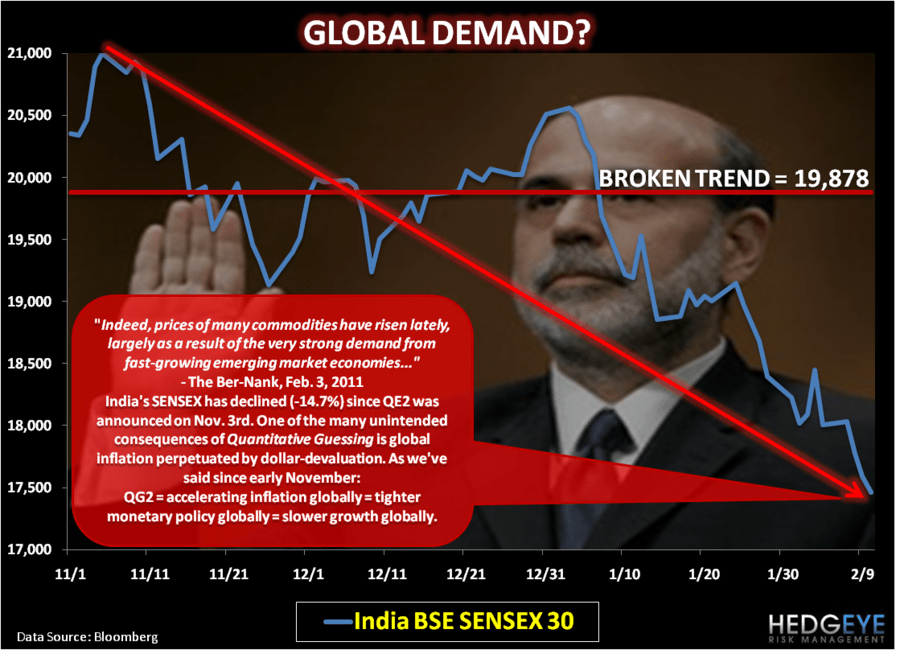

3. Global Inflation – in a shining moment for his academic dogma, Bernanke blamed the highest world food prices in the history of mankind on “emerging market demand.”

All the while, almost every single Emerging Market demand signal we measure sequentially is getting hammered as Global Inflation (which is priced primarily in US Dollars) slows last year’s cyclical economic recovery. Overnight, Indian stocks traded down another -0.74% taking the BSE Sensex to down -14.9% for the YTD as concerns of Asian growth slowing continue to spread to Thailand, Philippines, and Indonesia (down -2.1%, -2.8%, and -1.3%, respectively).

Pakistan, which is the world’s 6th largest population (so we think worthy of considering in light of The Ber-nank’s accelerating emerging market demand thesis), saw import demand DROP from +29% year-over-year growth in December to +3.7% year-over-year growth in January. Since commodity inflation was raging in January (with the USD down for 6 of the last 7 weeks), we’d have liked to have Ben’s rebuttal to that…

Now do I have courage here or common sense? Does Ben Bernanke’s new world order of the world’s reserve currency having no impact on global prices make any sense to anyone who isn’t levered long the inflation trade? How about this concept of the USA decoupling from the Rest of the World? These are important questions that, sadly, our 112th Congress didn’t have the analytical competence or courage to ask…

The World’s Danger remains a US Central Planner’s academic dogma.

My immediate term support and resistance lines for the SP500 are now 1306 and 1336, respectively. At 11AM EST, our Macro team will be hosting a conference call on one of the latest bubbles perpetuated by the Federal Reserve’s policy of zero percent interest rates in perpetuity – Munis (email sales@hedgeye.com if you’d like to participate).

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer