|

Editor’s Note: Below is a complimentary excerpt written by REITs analyst Rob Simone and taken from our daily Bitcoin Trend Tracker note. To sign up to get daily tracker updates CLICK HERE |

While Hedgeye as a firm has been at the forefront of advising clients to avoid Bitcoin and related equity exposure in Quad 4, we wanted to present the facts as we see them related to MicroStrategy Incorporated (MSTR) and the company’s levered Bitcoin position.

In short, any rumors that MSTR may become forced sellers of their Bitcoin amidst this Quad 4 drawdown may be unfounded and premature. We understand the company is lightly covered and obviously controversial, so we want to get the facts right for investors.

Specifically:

- MSTR has three tranches of non-callable debt outstanding with no maturities inside of 2025:

- $650 million of 0.75% 2025 Convertible Senior Notes, with a conversion price of $397.99,

- $1.05 billion of interest-free 2027 Convertible Senior Notes, with a conversion price of $1,432.46,

- And $500 million of 6.125% Senior Secured Notes, due 2028 with a “springing” maturity date of 9/15/25 at the earliest should MSTR fail to meet liquidity tests under the 2025 Converts; these notes are secured only by Bitcoin purchased subsequent to 6/14/21.

- MSTR’s business intelligence software operating business generates run-rate annual EBITDA that covers cash interest expense greater than >3x. It is important to consider that only $35.5 million of MSTR’s annual ~$44 million interest expense burden is a cash obligation, with the balance being non-cash amortization.

- MSTR’s total Bitcoin position is currently levered ~48% based on current Bitcoin pricing and following a 50% drawdown, and assuming no debt conversion given MSTR’s current share price. Effectively the debt is collateralized both by MSTR’s recurring cash flows as well as 2x coverage by the Bitcoin held on the balance sheet. For illustrative purposes, if the 2025 Converts were to be converted to equity, LTV drops to ~35%.

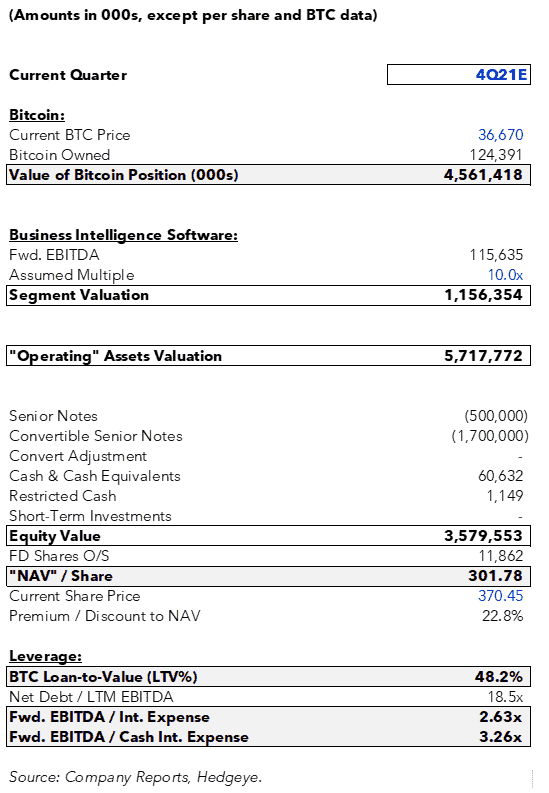

- Additionally, the last $1 billion of Bitcoin purchased by MSTR was executed via tapping of the ATM, aka MSTR “re-equitized” its Bitcoin position by selling stock to fund its purchases. Interestingly, with MSTR trading at an estimated ~22.8% premium to NAV, the share price is still somewhat conducive to additional equity issuance, should the market be open. This is similar to a REIT that sells “expensive” stock under a favorable cost of capital to buy assets and grow (vs. dilute) value. That window is obviously closing in Quad 4, but interesting nonetheless. See Figure 1 below.

- Additionally, as this is Bitcoin, it should be considered that all of MSTR’s debt is termed out beyond the next halving in May 2024.

Figure 1: MSTR Cap Table / Trading Value vs. “NAV”

These are the facts as we see them, and we would love to hear from clients if they are seeing something differently.