“He doesn’t spend months or years proving what he has observed.”

-Professor Heinz-Otto Peitgen, on Benoit Mandelbrot

Benoit Mandelbrot was one of the most important contributors to my multi-factor, multi-duration, global macro risk management model. After publishing “The Fractal Geometry of Nature” in 1982, Mandelbrot eventually landed in New Haven as a professor in Yale’s math department. He finally earned his tenure as I was leaving campus for Wall Street in the late 90’s. Over time, he’s been recognized as one of the forefathers of fractal math.

On October 14th of this year, Professor Mandelbrot passed away in Cambridge, MA. He was 85 years old. A few days later, one of our analysts, Matt Hedrick, sent me a nice tribute that Jascha Hoffman wrote for Mandelbrot in The New York Times. That’s where the aforementioned quote came from and it was followed by this one (which is taped on the insert of my notebook):

“But if we talk about impact inside mathematics, and applications in the sciences, he is one of the most important figures of the last 50 years.”

-Professor Heinz-Otto Peitgen (“Benoit Mandelbrot, Novel Mathematician, Dies at 85”, by Jascha Hoffman, NYT, October 16, 2010)

Amen Professor Peitgen. And thank you Jascha Hoffman. Benoit Mandelbrot was no one’s yes man. He wasn’t academically dogmatic either. He kept learning and re-thinking. As a result, I think the principles of Mandelbrot Math will be applied by global macro risk managers for decades to come.

I call this out this morning as I just got back from an investor trip that took me to Western Canada. The contours of the Rocky Mountain tops would most certainly fascinate Mandelbrot inasmuch as they would the fractal dimension of the Pacific Ocean’s coastline. Anyone flying across this world attempting to consider its deep simplicity from a top down perspective probably gets what I mean. It’s what make this game fun.

When you wake-up every morning trying to make a global macro market “call”, you need a place to start from. In order to attempt to know where you are going with that “call”, you most certainly need to know where you’ve been. By the time that market’s bell rings, you don’t have “month or years to prove what you have observed.” You have minutes. This is the game.

This morning’s global macro game is confusing. The US stock and bond markets are sending completely different messages as Asian stocks and bonds continue to break down. All the while European sovereign risk premiums continue to fluctuate like twitter.

Let’s look at US markets first:

- The SP500 had its 1st up day in the last 3, making a bullish comeback from an outside reversal on the day prior, hitting a new YTD high at 1228.

- The SP500 is now up +81.7% from its March 2009 lows and down -21.5% versus its October 2007 highs.

- The immediate-term TRADE range for the SP500 moves to 1, with the daily downside risk being about equal with upside reward.

- Volatility (VIX) at 17.74 is testing a breakdown towards its April lows; while this is a bearish contrarian signal, the VIX could easily test 16.

- US stock market Volume and Breadth studies continue to flash bearish, despite higher prices, there is a very negative skew.

- In our SP500 Sector Studies, 2/9 sectors are bearish (XLV, and XLU) and 7/9 bullish from an immediate-term TRADE perspective.

- The US Dollar Index continues to flash bullish on both our TRADE and TREND durations, with intermediate term TREND support at $79.49.

- US Treasury Yields continue to boom to the upside with 2s, 10s, and 30s all busting out into what we call Bullish Formations.

- The Yield Spread (10s minus 2s) continues to widen at +10bps for the week-to-date, supporting the rally in Financials (XLF).

Overseas, the immediate-term game is much less confusing:

- Chinese equities were down another -1.3% overnight and remain bearish from an immediate-term TRADE perspective at -14.3% YTD.

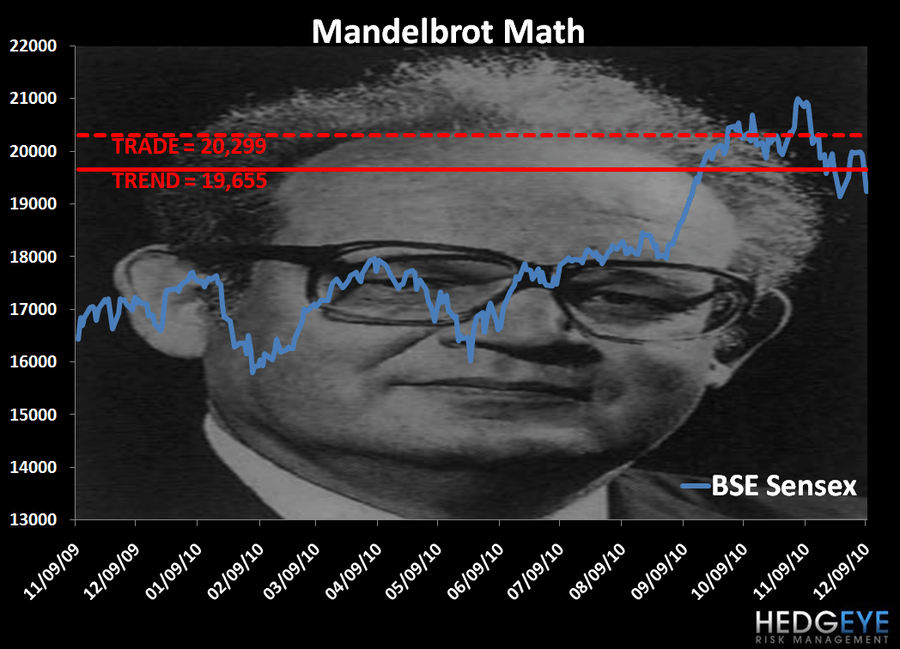

- Indian equities got tagged for another -2.3% drop overnight as the BSE Sensex broke its intermediate term TREND line of 19,655.

- Japanese equities are the only bullish immediate-term TRADE market in Asia as the POSITIVE correlation to the USD reigns supreme.

- Australia’s central banking guru, Glenn Stevens, continues to prove that raising rates and seeing unemployment drop can work together.

- Germany, Russia, and the Netherlands continue to flash bullish TRADE and TREND signals in both stocks and bonds.

- Spain, Italy, and Greece continue to flash bearish TRADE and TREND in both stocks and bonds.

- Brazil looks like India, as stocks on the Bovespa are down every day this week and now bearish on both TRADE and TREND durations.

- The Euro continues to flash bearish on both our TRADE and TREND durations with intermediate-term TREND resistance = $1.34.

Global Commodities markets continue to confirm what almost every country’s central banker who has real-time quotes sees – inflation:

- The CRB Commodities Index closed at 316 yesterday = +21% higher than Bernanke’s decision in Jackson Hole to Quantitatively Guess.

- Oil is in a Bullish Formation with immediate-term TRADE lines of support and resistance of $87.17 and $91.47, respectively.

- Copper prices are testing ALL-TIME highs again this morning = +29% since The Ber-nank opted to sponsor inflation.

Gold, meanwhile, looks a little bit less-like most commodities all of a sudden. To a degree, if real-interest rates continue to push higher, the gold bulls will have to compete with that yield. That’s new. Tops are processes, not points, but Gold will need to get back above its immediate-term TRADE line of $1390/oz to get me interested in getting long it again (I sold our GLD position on Monday).

Altogether, if you take the beginning and end of 2010, you can draw plenty of conclusions that are now crystal clear. From my global macro model’s vantage point, the deep simplicity of all of these global macro factors and what they mean prospectively to the global markets remains as follows: Growth Slowing, Inflation Accelerating, and Interconnected Risk Compounding.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer