The guest commentary below was written by Jesse Felder of The Felder Report.

Earnings growth has been terrific over the past several quarters, proving a strong tailwind for stock prices.

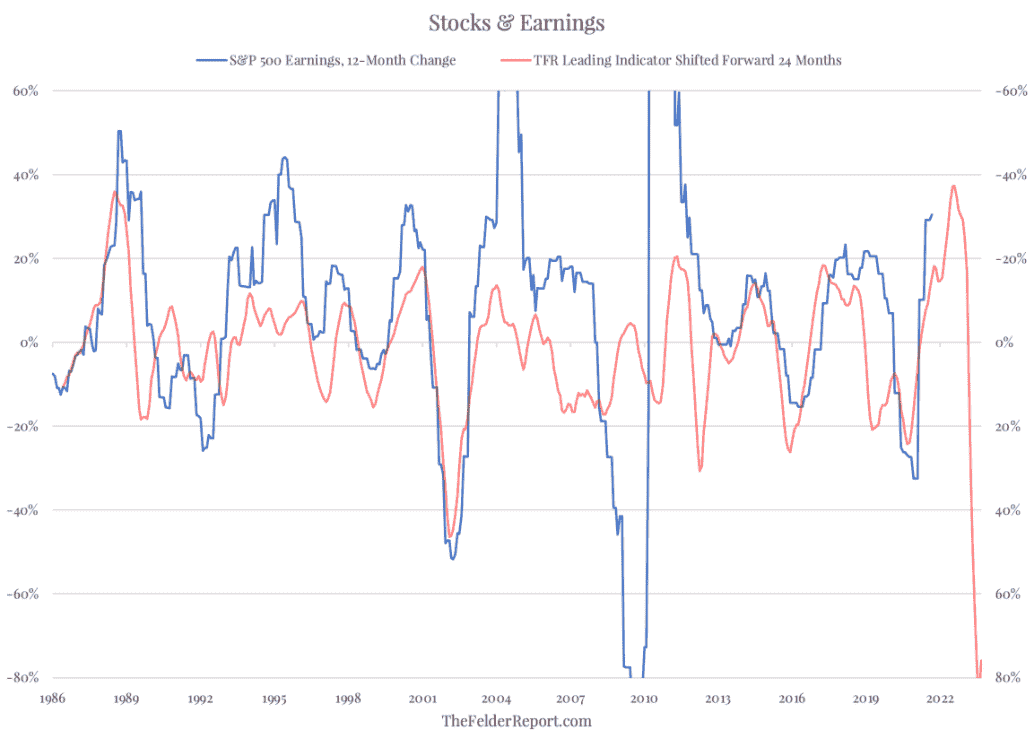

For astute market watchers, however, this should not come as any surprise. The decline in interest rates, oil prices and the dollar over the past couple of years, in fact, predicted it.

As a group, these markets have proven for decades now to be a far better forecaster of S&P 500 earnings growth than any analyst on Wall Street.

The chart below plots a composite of these indicators, shifted forward 24 months, against the 12-month change in S&P 500 earnings. The relationship is not perfect but generally gets the trend right.

With inflation pressures continuing to rise even as record amounts of fiscal stimulus begin to wear off and the economy clearly slows, however, an earnings recession over the next several quarters should also come as no surprise.

In fact, that is exactly what the recent action in interest rates, oil prices and the dollar now point to.

Considering valuations are more extreme than ever before and investors are also more highly leveraged than any other time in the past, a shifting in this fundamental driver of stock prices from tailwind to headwind should be something investors pay close attention to.

EDITOR'S NOTE

This is a Hedgeye Guest Contributor piece written by Jesse Felder and reposted from The Felder Report blog. Felder has been managing money for over 20 years. He began his professional career at Bear, Stearns & Co. and later co-founded a multi-billion-dollar hedge fund firm headquartered in Santa Monica, California. Today he lives in Bend, Oregon and publishes The Felder Report. This piece does not necessarily reflect the opinion of Hedgeye.