“History is the first casualty of media’s microsecond attention span.”

Key takeaways

-

Post virus, post Boeing-shutdown, and post some Millennials getting fired for the first time in their lives (jobless claims #accelerating), the ROC (rate of change) of US GDP growth is only going to slow further in both Q1 and Q2.

- The sum of the net contributions to the headline growth rate of 2.1% QoQ SAAR from Consumption and Investment totaled 12bps – a mere 5bps higher than our final nowcast of 0.07% for the headline figure. That represents the lowest net contribution of “C” and “I” since Q1 of 2011.

The big picture

That was one of my favorite quotes from Jim’s latest book, Aftermath. If the general population of people on the Old Wall doesn’t know what The Quads are, what do their journos know about the historical economic data and time-series driving them?

I can tell you that there’s a lot I don’t know about everything. One of those things is where a large place like China stops slowing during a national virus lock-down. Markets don’t know where the #slowing will stop either.

But, there’s a diversified portfolio for that. It’s called Hedgeye’s #Quad4. And, after selling both EM (Emerging Markets) and Energy (XLE) yesterday, I’m staying long of what I’ve already been long for 16 months: Treasuries, Gold, Utilities, REITS, etc.

Macro grind

Sometimes you have to take small losses before they become bigger ones. We booked plenty of gains in Oil and Energy (XLE) while being long of them from early October to the Iranian headline highs earlier this month. Recent losses were what they were.

If you have no losses, ever (especially during pandemics), don’t tell anyone that. They might get you a cell next to Madoff’s.

If you have politicized friends who believed yesterday’s US GDP report, you might want to get them a Hedgeye subscription. Here are the 3 Quadzilla (Darius Dale) takeaways that anyone running other people’s money (or their own) should be aware of:

- CORE: The sum of the net contributions to the headline growth rate of 2.1% QoQ SAAR from Consumption and Investment totaled 12bps – a mere 5bps higher than our final nowcast of 0.07% for the headline figure. That represents the lowest net contribution of “C” and “I” since Q1 of 2011.

- NOISE: The sum of the net contributions from Net Exports and Government Spending totaled 195bps – yes, a whopping 93% of the headline growth rate of 2.1%! That represents the highest net contribution of “NX” and “G” since Q2 of 2009.

- DEMAND: Real Final Sales to Private Domestic Purchasers slowed -6bps to 2.16% on a YoY basis and -90bps to 1.4% on a QoQ SAAR basis. Those growth rates represent the slowest rates of change since 2Q13 and 4Q15, respectively.

And, like China’s no-bounce PMI report for January (slowing to 50.0 this morning), the aforementioned mainline #slowing in the US Consumption, Demand, and Investment economy happened #PreVirus.

Post virus, post Boeing-shutdown, and post some Millennials getting fired for the first time in their lives (jobless claims #accelerating), the ROC (rate of change) of US GDP growth is only going to slow further in both Q1 and Q2.

If the US government didn’t literally make-up a “Deflator” of 1.5% yesterday, the headline GDP # would have been closer to 0.2-0.3%, fully loaded with all of the aforementioned ROC #slowing realities.

But don’t get mad, bro. The Bond Market, Gold, Utes, etc. already know the rate of change truth.

The other #Quad4 truth US Dollar Bears (which became Consensus Bearish CFTC futures & options positioning, post the December Dollar decline) should be aware of is that the US Dollar doesn’t want to go down in #Quad4.

There’s this thing called the US Federal Reserve that is going to have to deal with that.

If the Dollar isn’t going down:

A) Commodities aren’t going back up like they did in December

B) Our 6-month #InflationAccelerating call is over

C) Long-term Bond Yields are going down, faster

D) The Yield Curve is going to re-invert

E) Repo market US Dollar shortages will continue

F) China’s leverage & liquidity problem (in USD denominated debt) continues

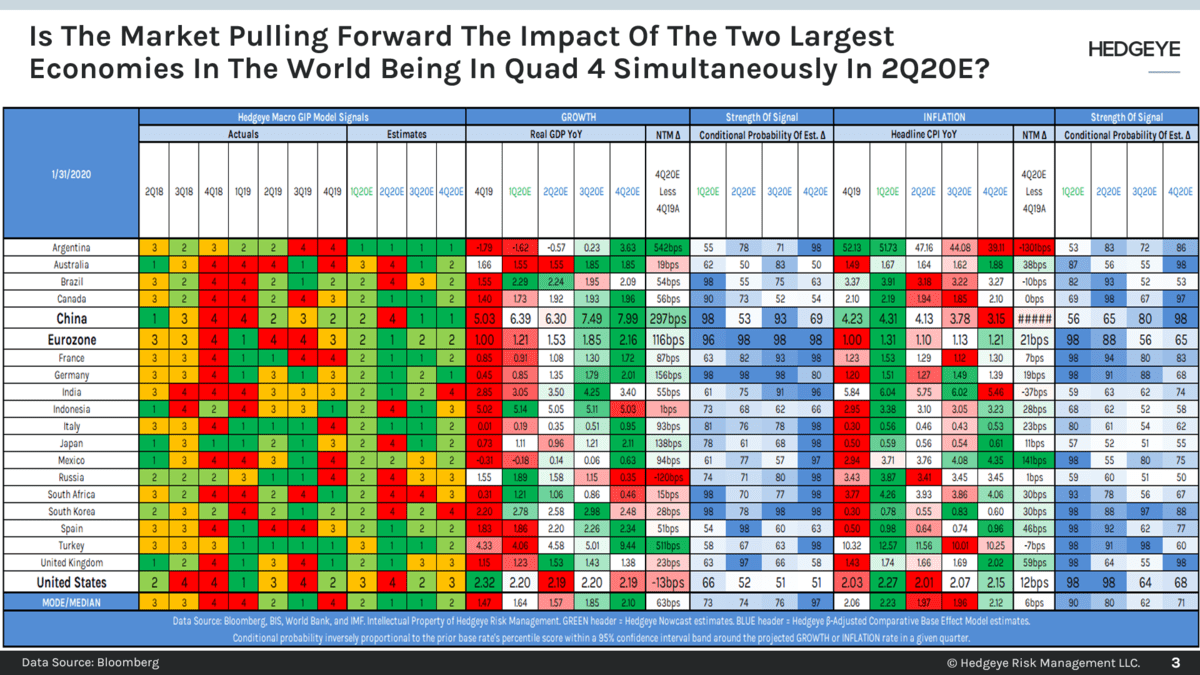

And… to summarize what could be G through Z… both the US and Chinese economies will be in #Quad4 in Q2 of 2020.

Our levels

Our immediate-term Global Macro Risk Ranges (with intermediate-term TREND signals in brackets) are now:

UST 10yr Yield 1.51-1.75% (bearish)

SPX 3240-3320 (bullish)

RUT 1632-1691 (bearish)

Utilities (XLU) 66.17-69.71 (bullish)

REITS (VNQ) 93.74-96.10 (bullish)

Energy (XLE) 53.30-56.93 (bearish)

Shanghai Comp 2850-3076 (bearish)

Nikkei 22674-23615 (bearish)

VIX 12.01-18.60 (neutral)

USD 97.10-98.25 (neutral)

Oil (WTI) 50.50-57.23 (bearish)

Nat Gas 1.77-2.01 (bearish)

Gold 1545-1595 (bullish)

Copper 2.45-2.66 (bearish)

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer