Dear ETF Pro Plus Subscriber,

Welcome back!

|

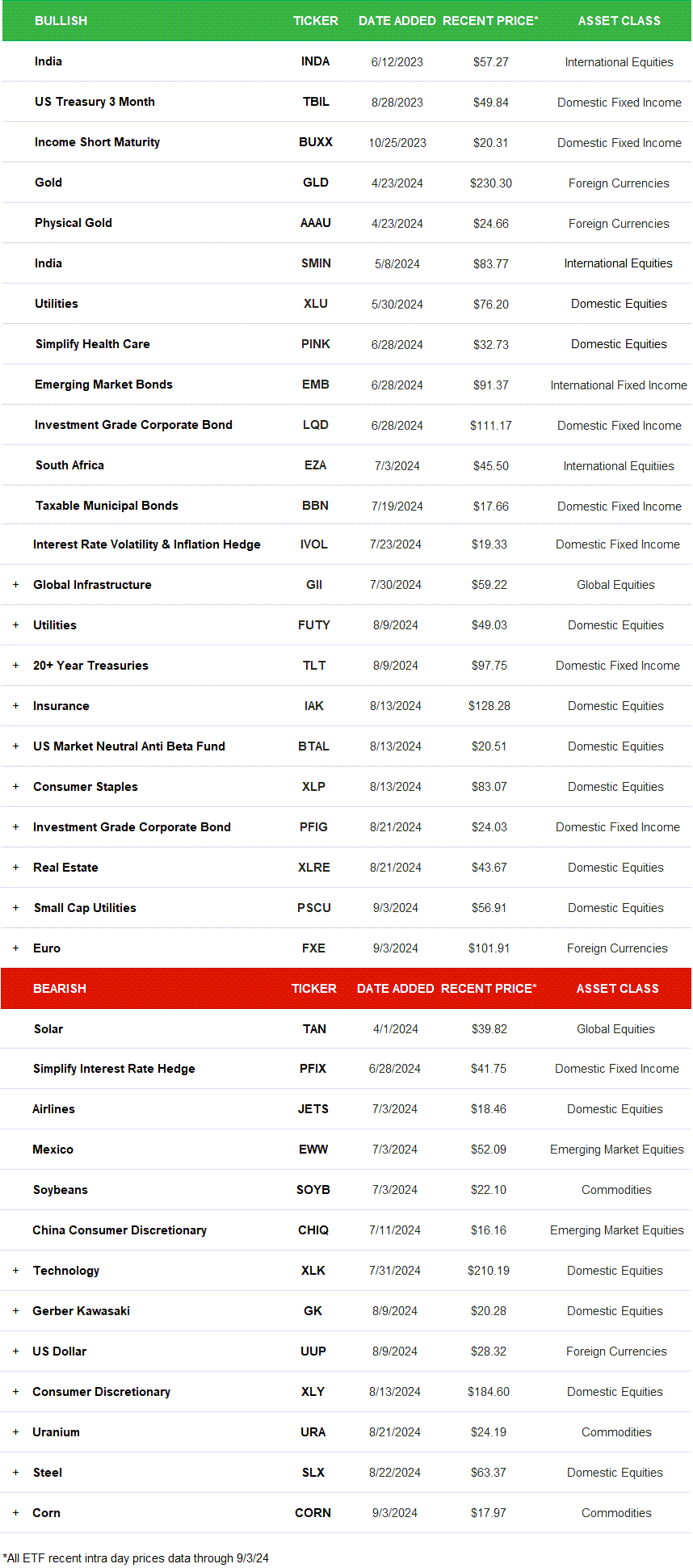

The current lineup of ETFs is as follows: Long: INDA, TBIL, BUXX, GLD, AAAU, SMIN, XLU, PINK, EMB, LQD, EZA, BBN, IVOL, GII, FUTY, TLT, IAK, BTAL, XLP, PFIG, XLRE, PSCU, FXE Short: TAN, PFIX, JETS, EWW, SOYB, CHIQ, XLK, GK, UUP, XLY, URA, SLX, CORN |

Below are updates to our Quarterly Macro Themes via on 3Q24 Mid-Quarter Update on 8/11/2024.

THEME 1: USA’s #Quad3 to #Quad4 Transitions

|

The back half of the year remains poised for a mathematical deceleration in year-over-year growth as the confluence of further (plodding) labor deceleration, further cumulative deterioration for the bottom slant of the economic K and #HFL constraints on further acceleration in the cyclical economy and consumer credit growth serve as a collective rate-of-change drag. On the Inflation side, steeper comps, favorable seasonality, domestic demand deceleration and China/EM Quad4 should drive a short stretch of disinflation and deliver a condition set supportive of policy easing in September. Quad 4 in 3Q will again give way to elevated macro chop with a ping-ponging between Quad 3 and Quad 2 back to defining the monthly Quad cadence into 1H25. Fourth Turning geopolitical and election dramatics should continue to amplify the turbulence associated with the #Quad4 catalyzed rise in macro and market fragility. |

THEME 2: Inflation Down (Small), Then Up

|

The setup for disinflation in Aug/Sep is there amid generally steepening comparative base effects, seasonality distortions, and bearish TRENDs (for now) in oil markets. Beyond that, however, the base case path appears set to resume higher in RoC terms. The overlays of Fed meeting timing and the fulcrum risk posed by an acute Quad 4 growth/labor shock are important considerations. |

THEME 3: Country Quad Setups

|

The signal remains bullish on India as its world-leading economic growth is set to hold at these levels, with probabilities pointing towards shallow accelerations in the 2H24 on buoyant domestic demand and government spending as well as strong credit growth. Meanwhile, Europe continues to increasingly transition from "bad" to "less bad" to "better" as it emerges from the global industrial recession that weakened European manufacturing activity; however, the recent political turbulence in France have raised some new questions. The setup is much less favorable in the orient as the track of decelerating growth is likely to extend from 2Q24 into 3Q24 in China, whereas Brazil continues to work as a short exposure with market forces looking past the model-implied probabilities of shallow growth acceleration in 2H24 as uncertainty around the full-year growth estimate builds. |

GLOBAL QUAD OUTLOOK

Below is an updated list of the 36 current ETF Pro Plus tickers. Keep reading for an overview of our thesis for each of these current ETFs, along with what we’ve added and removed since the last newsletter.

New users should definitely check out the Appendix for a brief primer on our Macro process and how we select (and remove) the exposures in ETF Pro Plus. Review last month's edition of ETF Pro Plus.

CURRENT ETF LINEUP

COMMODITIES

"Commodities, as an Asset Class, do NOT like #Quad4," CEO Keith McCullough wrote recently in the Early Look. "This we know. Why? A: we invented #Quad4." As a reminder, #Quad4 is when Growth and Inflation slow. With both the U.S. and China in #Quad4, Commodities is not an asset class to own here.

Given the bearish setup for Commodities from a GIP model perspective, CEO Keith McCullough's quantitative signal is bearish on the following: Soybeans (SOYB), Uranium (URA) and Corn (CORN).

DOMESTIC EQUITIES

The #Quad4 in Q3 market environment favors low beta and specific equity sectors. A big Sector pivot has been adding long Utilities (XLU, FUTY and small caps in PSCU), an exposure that works in #Quad4 (and our projected #Quad3 in 4Q).

Our preferred Health Care exposure (another classic #Quad4 long) is Simplify Health Care (PINK). The fund is managed by portfolio manager Michael Taylor, who discussed his largest holding Sarepta Therapeutics (SRPT) at Hedgeye Live in May and before the stock went up +40%. We continue to like PINK here (as it hits all-time highs).

Three other Sectors that benefit from #Quad4 are Consumer Staples (XLP), Real Estate (XLRE) and Insurance (IAK), all of which benefit from our preference for lower beta and lower volatility.

Given the #Quad4 environment and our preference for low beta versus high beta, we like long US Market Neutral Anti Beta (BTAL). The ETF attempt to "generate positive returns regardless of the direction of the general market, so long as low beta stocks outperform high beta stocks... [and] Provides consistent negative beta exposure and can be used as an effective equity hedge to lower portfolio volatility and reduce the impact of drawdowns."

The opposite of our preference for lower volatility, low beta stocks is high beta, high volatility stocks. Technology (XLK) and Gerber Kawasaki (GK), with their overweights to Microsoft (MSFT), Nvidia (NVDA) and Apple (AAPL), fit the bill. These mega-cap Tech stocks have been breaking down to Bearish Trend (note: AAPL remains bullish trend).

Another Bearish Trend is Consumer Discretionary (XLY), with 37% of the ETF allocated to Amazon (AMZN) and Tesla (TSLA) both of which are Bearish Trend. We also have Airlines (JETS). Pull up a chart of JETS and you'll see what a Bearish Trend looks like.

Talk about an exposure tethered to declining global demand: Steel (SLX). This ETF is also commodity-sensitive, another negative in #Quad4.

DOMESTIC FIXED INCOME

Yielding near ~5%, we continue to be long the US Treasury 3 Month (TBIL). Income Short Maturity (BUXX) provides investors with exposure to short-term, high-quality bonds while minimizing volatility. Due to their shorter duration, short-term bonds have less time to be impacted by changes in interest rates.

We added a series of new Fixed Income long exposures recently, including Taxable Municipal Bonds (BBN), Investment Grade Corporate Bond (LQD and PFIG) and Interest Rate Volatility & Inflation Hedge (IVOL). CEO Keith McCullough wrote an Early Look recently which simply explains why in five words, "#Quad4 = Buy Gold, Bonds, Utes." Don't overcomplicate things.

Another classic #Quad4 signal, longer-term bond yields are Bearish Trend (meaning the price of longer-term bonds is bullish). Keith added 20+ Year Treasuries (TLT) on that signal.

In a Real-Time Alert last month, CEO Keith McCullough had this to say about our short on Simplify Interest Rate Hedge (PFIX). "For PFIX to stop working, we'd need to see a Bullish @Hedgeye TREND breakout in Bond Yields. My #VASP (Volatility Adjusted Signaling Process) isn't signaling that."

EMERGING MARKET EQUITIES

Bearish TRENDS with poor Quad setups? Mexico and China are about to hit #Quad3 in Q3. Mexico (EWW) and China Consumer Discretionary (CHIQ) are Bearish Trends. Remain short both.

FOREIGN EXCHANGE

We remain long Gold via Gold (GLD) and Physical Gold (AAAU). Why? "We buy it on sale in both #Quad3 and #Quad4," CEO Keith McCullough wrote in a recent Early Look titled "#Quad4 = Buy Gold, Bonds, Utes" published on 7/26/2024.

Another interesting set-up in is long the Euro (FXE). Europe is entering #Quad2 through 2Q 2025, we continue to like FXE on European economic strength relative to the U.S. The converse of that is our short on US Dollar (UUP). It's a bearish trend and as the Fed coos dovish, the purchasing power of the people will continue to be devalued.

GLOBAL EQUITIES

On paper, the adoption of clean energy technology is something everyone can get behind: Roll out environmentally friendly alternatives, become more energy efficient, save the environment and, eventually, lower utility costs. But the transition comes with several challenges, including the poor economics of implementing clean solutions, political and social inertia, and regulatory delays.

The movement to install solar panels on neighborhood rooftops has slowed, as many public solar companies have filed for bankruptcy. The remaining industry leaders posted big losses in their latest quarterly earnings reports. We are short Solar (TAN) amid these setbacks (as it remains bearish trend).

An offset to short TAN is Global Infrastructure (GII). About 42% of this ETF is Utility exposure (a classic low beta exposure in #Quad4).

INTERNATIONAL EQUITIES

The signal remains bullish on India (INDA and SMIN) as its world-leading economic growth is set to hold at these levels, with probabilities pointing towards shallow accelerations in the 2H24 on buoyant domestic demand and government spending as well as strong credit growth.

Another bullish trend with a strong GIP outlook? South Africa (EZA) is in #Quad1 in 3Q and 4Q, a unique bright spot alongside India in a challenging global economic environment.

INTERNATIONAL FIXED INCOME

Why do we like Emerging Market Bonds (EMB) long side? Hedgeye CEO Keith McCullough continues to like fixed income long exposures as bond yields continue to signal lower highs on declining volatility.

APPENDIX

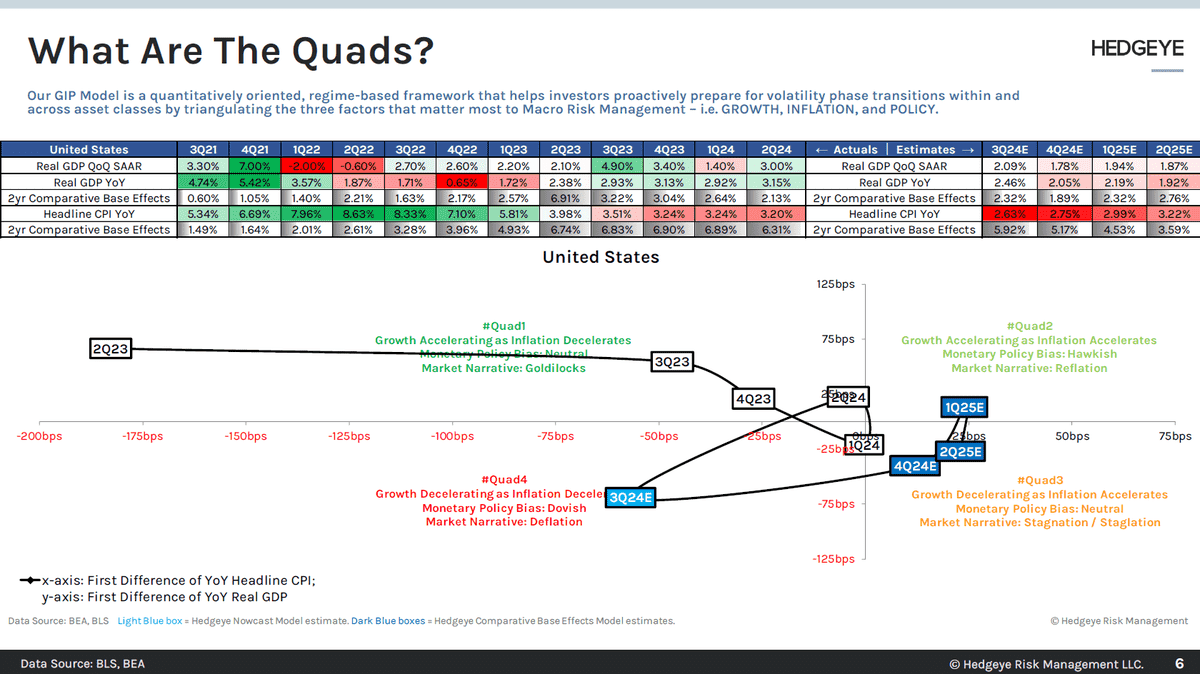

We find two factors to be most consequential for forecasting future financial market returns: economic growth and inflation. We track both on a year-over-year rate of change basis to better understand the big picture then ask the fundamental question: Are growth and inflation heating up or cooling down?

From there, we get four possible outcomes, each of which is assigned a “quadrant” in our Growth, Inflation, Policy (GIP) model and the typical government response as a result (neutral, hawkish, in-a-box or dovish): Growth accelerating, Inflation slowing (QUAD 1); Growth accelerating, Inflation accelerating (QUAD 2); Growth slowing, Inflation accelerating (QUAD 3); Growth slowing, Inflation slowing (QUAD 4).

After building this base of knowledge, we can now select what we like and don’t like based on our historical back-testing of the different asset classes that perform best in each of the four quadrants. The chart above shows the U.S. economy dipping into Quad 4 in 3Q 2024 followed by Quad 3 in 4Q.

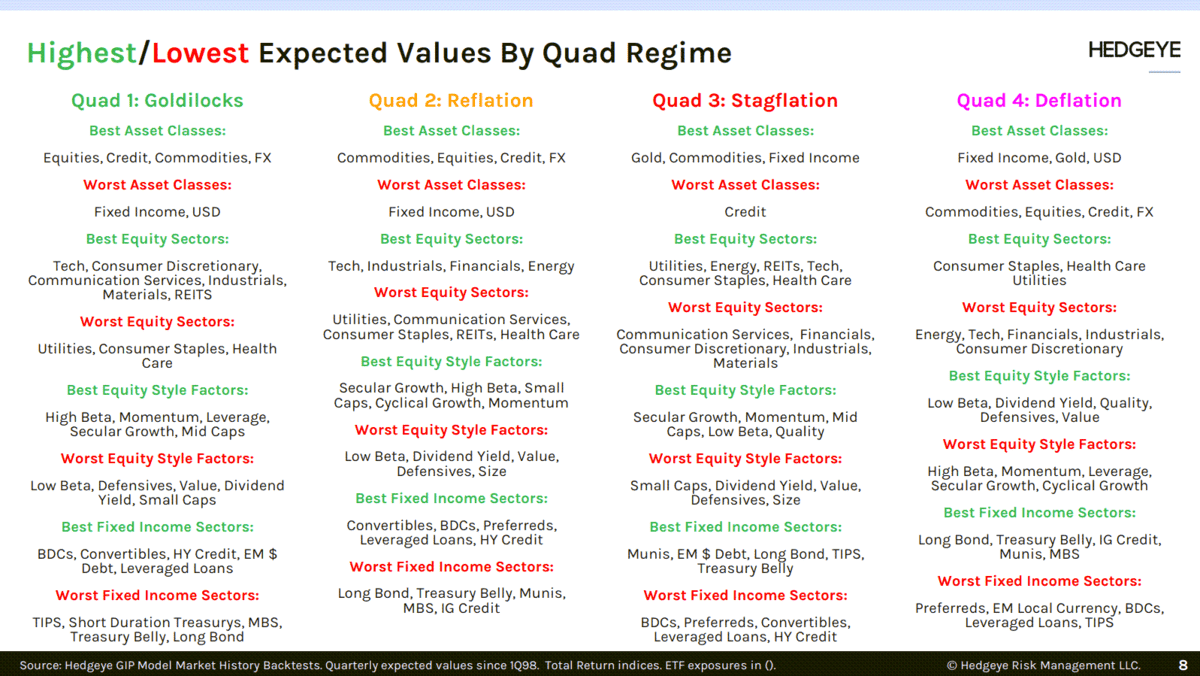

Below is a chart that lays out precisely what we like and don’t like when an economy is in each of the four quadrants. This chart should help you make better investment decisions, even outside our recommendations in ETF Pro Plus. (For more on our Macro team's overall research process, click here to read our detailed "Macro Playbook.")