“I saw and loved.”

Key takeaways

- When we first started, we used to get criticized for our unorthodox and relatively simple forecasting techniques. Now, not so much.

- We nailed the 2008-09 downturn, the 2009-10 recovery, the 2011 stagflation, the 2011-13 deflation off those highs, the 2012 slowdown, the 2013 recovery, the 2014-16 deflation, the 2015-16 slowdown and the 2017 recovery.

- Do we nail everything? Of course not! We turned bearish (on the market) too early in late-2010; Stayed bearish throughout 2012; and Stayed bearish well into 2H16.

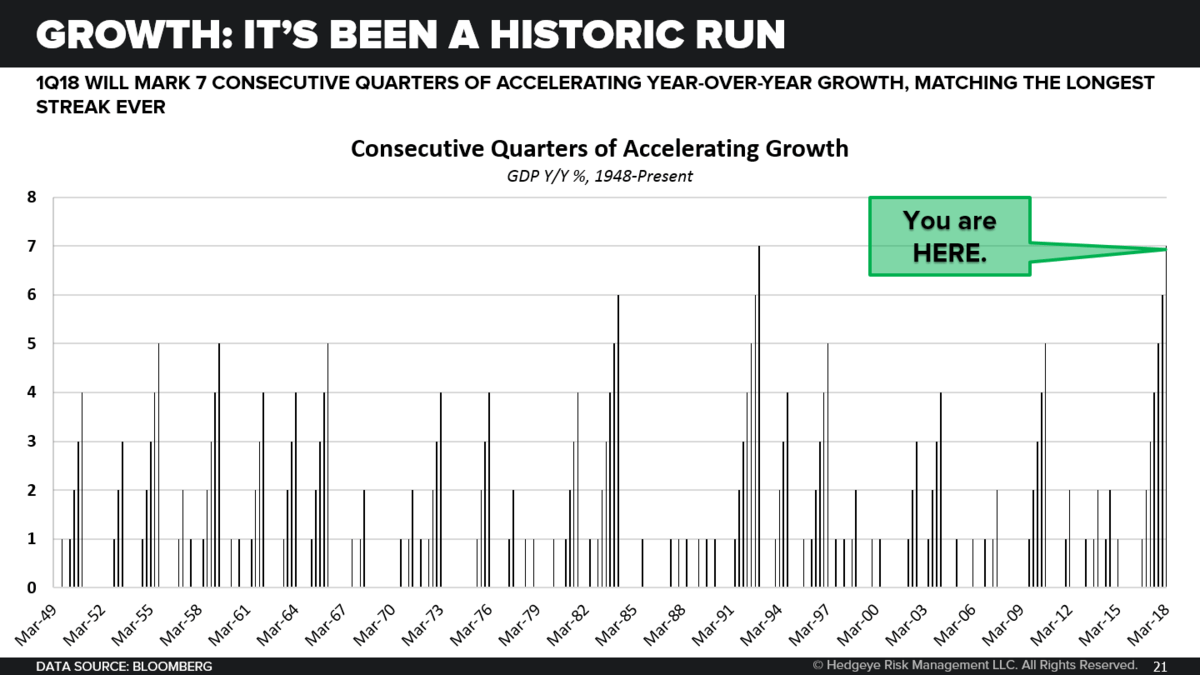

- Our goal isn’t to nail every print; it’s to identify the most probable path of growth and inflation over the intermediate term. Right now that means sticking with our dour U.S. growth outlook (in RoC terms) and below-consensus inflation forecasts for 2H18.

The big picture

Edward Gibbon was an 18th century English writer, historian and member of British Parliament (Whig Party). He is most remembered for his seminal work, The History of the Decline and Fall of the Roman Empire, which became the go-to textbook on the subject and contained a rather controversial criticism of organized religion.

Are you comfortable criticizing the Old Wall, its legacy research providers and its myriad of click-bait media outlets? From what I can tell, there is an increasing number of investors who are. It’s early April and Keith and I have already had half as many introductory meetings with prospective clients as we did for all of 2017. If we keep this pace up, we have a legitimate shot of doubling that figure by year-end.

Thank God for MiFID II and the level playing field it’s providing for an innovative firm like ours, at the margins. Are general industry price deflation and shrinking commission pools good for our business? Absolutely not. I suspect they won’t be for anyone trying to generate alpha on the buyside with increasingly limited resources either. All that being said, however, we are uniquely positioned to take increasing share of whatever is left. We’re all overpaid anyway...

Macro grind

When we first started at this experiment to build a research shop that was free from the conflicts of interest associated with banking, trading and asset management, we used to get criticized for our unorthodox and relatively simple forecasting techniques. A decade and a myriad of books praising Bayesian Inference (e.g. Thinking, Fast and Slow, Superforecasting and Misbehaving) later, not so much.

I honestly don’t know if I would feel as comfortable modeling economies the way we do if I started at this now. There’s something about the bliss of youthful ignorance that allows you to resist conforming to industry standards – e.g. Kevin Kaiser’s calls on LINE, KMI and CHK – or even those standards taught to us in econ classes at Yale and Princeton, respectively.

You build confidence in unorthodox approaches in this industry by being right. Nailing the 2008-09 downturn, the 2009-10 recovery, the 2011 stagflation, the 2011-13 deflation off those highs, the 2012 slowdown, the 2013 recovery, the 2014-16 deflation, the 2015-16 slowdown and the 2017 recovery helped us build confidence in our process(es), at the margins.

Do we nail everything? Of course not! I can immediately recall three costly mistakes we made throughout:

- Turning bearish (on the market) too early in late-2010;

- Staying bearish throughout 2012; and

- Staying bearish well into 2H16.

Perhaps it’s the way us football players are coached that causes me to over-analyze our “bad plays”. Fortuitously, and much like my playing career (I wasn’t beaten for a single sack as a 4-year starter at offensive tackle), we don’t have too too many of those to dwell on…

Moving along, if we’re right two-thirds of the time with respect to our quarterly investment themes, we’d consider that an acceptable success rate. Moreover, that ratio synchs up well with the directional accuracy embedded in our comparative base effects model which suggests roughly 65-70% of the time the sign of the marginal rate of change of the two-year average growth or inflation rate in the comparative base period is the inverse of the sign of the marginal rate of change in the forecast period.

That’s an admittedly verbose way of saying that growth and inflation have an investably high propensity to accelerate/decelerate against easier/tougher compares.

Our goal isn’t to nail every print (although we’ve been pretty good at that lately); it’s to identify the most probable path of growth and inflation over the intermediate term according to all the information we have at the current juncture – including changes in base effects. This is the Bayesian prior from which we adjust our estimates in accordance with information received from Bayes factors such as the indicators in our predictive tracking algorithms for growth and inflation, as well as financial market signals.

In conjunction with the bounce [to lower-highs] in U.S. equities, we’ve been getting a lot of questions about what’s driving our dour U.S. growth outlook (in RoC terms) for 2H18 and our response is as simple as the unorthodox forecasting processes underpinning it:

- Steepening base effects;

- Key high-frequency soft data – which led on the way up – is rolling over on a trending basis; and

- The corporate profit outlook is more challenging than consensus believes due to rising wage pressures and traversing peak rates of contribution to sales and EPS growth from a falling U.S. dollar. Recall that corporate profit growth leads hiring and capex.

On the bounce [to near the top end of the risk range] in bond yields, we’ve also gotten a lot of questions this week about what’s driving our below-consensus inflation forecasts in 2H18. In short:

- [Again] steepening base effects;

- A rollover in commodity-oriented inflationary pressures that suggest reported inflation should peak in JUN; and

- A likely reversal in the U.S. dollar.

Does that mean you need to de-risk your exposure to U.S. equity and credit beta at every price? Absolutely not. Nor does it mean you need to back the truck up on Treasury bonds here either. It’s important that we don’t overlook the sequence of growth and inflation between now and then – most notably our forecasted accelerations in headline GDP and CPI here in Q2. The sequence matters a helluva lot more than bin values when it comes to explaining financial market returns.

All told, we think investors should use the next few months of trading to prepare their portfolios to fade an uber-hawkish Fed, > 3% on the 10Y and a potential reflationary bias in the market sometime this summer. Of course that view could change with more information. We reserve the right to remain Bayesian in our unorthodox approach.

Our levels

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.71-2.86%

SPX 2573-2687

VIX 17.38-24.60

USD 88.78-90.25

Oil (WTI) 61.76-67.69

Copper 2.95-3.16

Keep your head on a swivel,

DD

Darius Dale

Managing Director